5 月 26 日,数字资产交易平台 JuCoin 正式推出首期 USDT 定息理财产品,为广大用户提供安全、灵活且高回报的数字资产增值服务。本次产品上线,不仅是 JuCoin 理财业务的正式起航,更是其金融服务战略升级的重要里程碑,致力于满足用户在数字时代日益增长的财富管理需求。

产品亮点

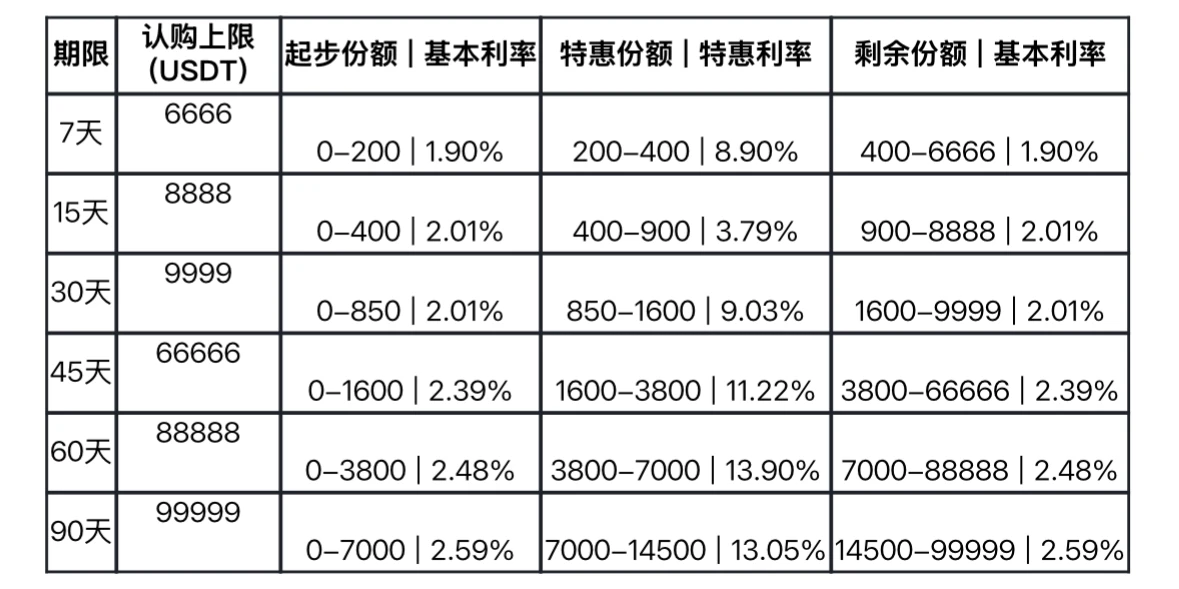

JuCoin 理财首批 USDT 定息产品正式上线,产品覆盖 6 种不同期限,从 7 天到 90 天。

产品亮点

6 种期限随心选: 7 天/15 天/30 天/45 天/60 天/90 天

阶梯利率更划算:买对额度,享受更高特惠利率

本金保障 + 专业风控:资金更安心,收益更稳健

收益计算超简单

JuCoin 采用"阶梯利率"计算方式:

1. 每个产品都设有"起步份额"和"特惠份额"

2. 起步份额内:享受基础利率

3. 超过起步份额:特惠份额部分享受更高利率

4. 超过特惠份额:超出部分回归基础利率

举个例子

Jason 购买了 45 天产品,投入 4000 USDT:

• 前 1600 USDT:享受 2.39% 基本年化利率

• 中间 2200 USDT(3800-1600):享受 11.22% 特惠年化利率

• 最后 200 USDT:回归 2.39% 基本年化利率

• 实际综合年化≈ 7.25%

( 1600* 2.39% + 2200* 11.22% + 200* 2.39% )/4000 ≈ 7.25%

温馨提示:

• 不同产品设有不同认购上限

• 收益按日计算,到期自动发放

• 详情请查看产品页面说明

社区激励计划

JuCoin 团队一直相信社区的力量,倾听用户的声音。

这次是 JuCoin 理财产品的首次亮相,超高利息理财产品之外,还为所有参与宣传和邀请的朋友准备了丰厚奖励金池。KOL、社群领袖、普通用户都可以轻松参与。

活动玩法要素 :

人人都可以邀请赚钱

分享邀请码,邀请新朋友来 JuCoin 注册并购买理财产品,有机会赚现金奖励。

满足条件就奖励现金

只要被邀请用户认购了一定额度的理财产品,并保持账户存额≥ 2000 USDT 状态 45 天以上,就算“成功邀请”。邀请者将获得与“成功邀请”存款总额挂钩的现金奖励。账户存额=用户账户中的闲置 USDT+购买的理财产品份额

(奖励计算细则即将公布,敬请关注官方公告和 AMA 直播)

老用户也有奖励

如果已有用户购买了 2000 USDT 以上份额的 45 天/60 天/90 天理财产品,也会给其邀请人发放奖金。

即使未满足条件,也能拿返佣

就算朋友暂时没有达标,用户依然可以享有 JuCoin 基础邀请返佣政策,未来朋友在平台的交易行为,用户最高可以拿 30% 返佣分成。

未来展望

JuCoin 这次推出的基于 USDT 的 7 至 90 天短期系列定息理财产品仅仅是开始。

此次活动不仅为用户提供优质的理财选择,也标志着 JuCoin 在数字资产财富管理领域迈出的关键一步。在活动期间 JuCoin 将密切关注用户的使用行为和反馈,深入了解社区的真实需求,并积极采纳建议,作为未来产品设计与功能优化的重要参考。

当前活动不设固定截止时间,现有的理财产品与特惠利率将在较长一段时间内持续开放。若用户暂时错过了心仪产品的额度,也无需担心:当相关产品到期后,额度将自动释放并重新开放认购。

随着产品研发的持续推进,JuCoin 未来计划推出更多满足用户多样化需求的理财方向和功能特性,包括但不限于:

• 多币种理财: 支持 USDC 等其他主流稳定币的理财产品

• 流动性改良:具备灵活赎回或可交易转让机制的理财工具

• 无门槛收益:无需锁仓认购,即可享受收益的活期账户

• 专业级理财工具:涵盖 RWA 资产、市场波动率、双币对冲策略、FoF 等的结构化理财产品

结语

JuCoin将持续以用户为核心,构建稳健、高效且创新的数字资产理财生态。在当前牛市背景下,JuCoin 平台正通过理财宝的稳健收益策略,并结合其在 CeDeFi 等创新领域的持续布局,为用户提供全面且高效的数字资产管理方案。