Рыночная капитализация Toncoin (TON) снижается, и позиция токена в топ-10 криптовалют находится под угрозой. Он рискует вылететь из этого рейтинга

Флагманская монета «Телеграма»Toncoin (TON) уступила свою позицию в рейтинге рыночной капитализации токену Tron (TRX). Это произошло после недавней коррекции цены на фоне ареста основателя «Телеграма» Павла Дурова.

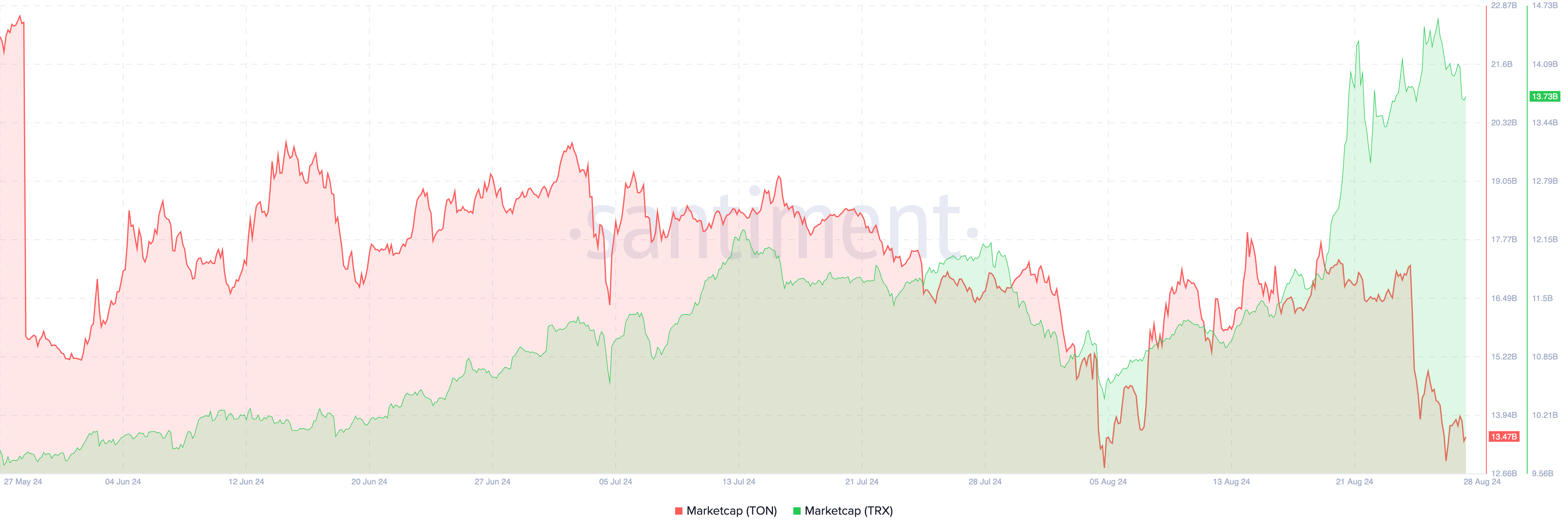

Флагман «Телеграма» спасовал перед Tron

До событий воскресенья рыночная капитализация TON составляла $17,20 млрд. Тем временем рыночная капитализация Tron превысила $14 млрд после того, как монета обогнала Cardano. Теперь же рыночная капитализация Toncoin упала до $13,47 млрд, сократившись на $4 млрд за последние три дня. Падение цены TON напрямую способствовало этому снижению.

Между тем Tron (TRX) находится в более выгодном положении. За последние 30 дней цена TON упала на 18%, а стоимость TRX увеличилась на ту же величину. Позитивная динамика TRX в основном связана с запуском площадки для создания мемкоинов SunPump, представленной основателем блокчейна Джастином Саном.

Проект Toncoin тоже активно развивался до недавнего времени, привлекая к себе большое внимание. Однако продолжающиеся продажи и нерешенная ситуация с Дуровым предполагают, что цена и рыночная капитализация токена могут упасть еще больше.

Читайте подробнее: Что такое TON. Обзор проекта и криптовалюты Toncoin

Показатель чистого потока средств в сегменте крупных держателей (Large Holders Inflow) уменьшился на 95% за последние семь дней. Крупные держатели — это адреса, на которых хранится более 1% оборотного предложения актива. Чистый поток измеряет разницу между количеством монет, купленных этими крупными держателями (приток) и проданных ими (отток) за определенный период.

Когда показатель резко вырастает, это бычий сигнал. Он указывает на то, что киты накапливают актив. И наоборот, снижение означает усиление оттока средств с адресов крупных игроков. Это чревато потенциальным давлением продаж и снижением цены. В случае с TON снижение показателя свидетельствует о том, что крупные инвесторы остаются осторожными и не покупают токены по текущей цене.

Если ситуация не изменится, монете может быть сложно компенсировать недавние потери. В итоге она рискует лишиться и 10-го места в рейтинге самых капитализированных криптовалют, уступив его Cardano (ADA).

Читайте также: Как арест Павла Дурова повлиял на курс и перспективы Toncoin (TON)

Прогноз TON: готовимся к новому снижению

На дневном графике цена TON остается под значительным давлением. Например, вчера монета пыталась достичь $6, но на момент написания упала до $5,32 — вероятно, из-за сегодняшнего общего снижения рынка.

Кроме того, индекс относительной силы (RSI) для TON снизился, отражая текущий медвежий импульс. Для Toncoin это может означать возможное дальнейшее снижение цены.

Тем временем уровень Фибоначчи 38,2% недавно стал зоной сопротивления для TON. Это может затруднить формирование повышающихся максимумов. Чтобы получить шанс на рост, токен должен преодолеть этот уровень.

Если цены на рынке продолжат падать, TON может опуститься ниже $5, возможно, до $4,85. Однако в случае роста числа транзакций с Toncoin покупательское давление может потенциально поднять цену до $5,67.