原文来源:钮轱辘瑶

如果市场情绪发生变化,ADA 可能上涨至 0.67 美元,AVAX 可能上涨至 50.35 美元,MATIC 可能上涨至 1.06 美元。

根据 IntoTheBlock 的说法,Cardano [ADA]与Avalanche [AVAX]和Polygon [MATIC]的相关性比任何其他顶级加密货币都更强。

截至发稿时,ADA 与 AVAX 之间的相关性为0.99。对于 MATIC,60 天相关系数为 0.98。相关系数值范围从 -1 到 +1,前者表示存在显著差异。

另一方面,接近 +1 的读数表明方向性运动强劲,Cardano 和其他两种货币就是这种情况。截至本文撰写时,ADA 的价格为 0.45 美元,年初至今 (YTD) 下跌了 26.40%。

深水三人组

AVAX 的价格为 36.94 美元,同期下跌 11.73%。最后,MATIC 的价格为 0.71 美元,下跌 29.21%。

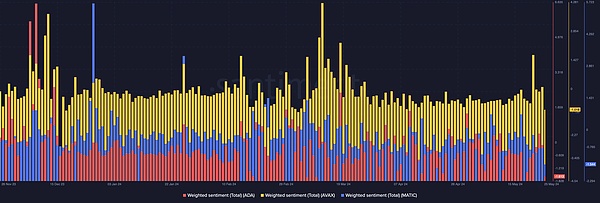

为了确定 Cardano 是否会继续与 AVAX 和 MATIC 保持一致,AMBCrypto 研究了围绕这些项目的情绪。

看一下 Santiment 提供的加权情绪指标,ADA 的读数为 -1.613。就 AVAX 而言,读数为 -1.018,而 MATIC 的读数为 -1.544。

加权情绪显示独特的社交量,以对资产的评论来衡量。如果该指标为正,则意味着市场参与者看涨,对相关资产的需求可能会增加。

然而,由于这三者的读数均为负值,这表明对潜力的信心不足。 鉴于这种趋势,ADA、AVAX 和 MATIC 的价格有可能再次下跌。

与此同时,这种高度负面的情绪可能预示着在出现大幅上涨之前需要一段较长的积累期。

代币可能很快就会回到牛市阶段

但为了证实这一点,我们需要分析市场价值与实际价值 (MVRV) 的比率。该指标可判断加密货币是否被低估。

MVRV 比率越高,持有者的利润就越多,他们愿意出售的资产就越多。另一方面,该指标的下降表明更多持有者正在陷入未实现的损失。

在这种情况下,大多数人会决定持有。截至发稿时,Cardano 的 30 天 MVRV 比率为 -5.313%。这意味着,如果过去 30 天内积累的每个 ADA 持有者都出售,他们就会产生未实现损失。

在 MATIC 的案例中,该指标为 1.608%。但 AMBCrypto 注意到的一件事是,该比率下降了。因此,人们可以假设在牛市背景下代币被低估了。

无论现实与否,以下是AVAX 以 ADA 计算的市值

如果价格开始回升,ADA 可能会回升至 0.67 美元。如果 AVAX 也是如此,该代币可能会升至 50.35 美元。

此外,MATIC 的反弹可能使价格朝 1.06 美元的方向发展。

目前我们6个分析师一起投研出来的一些百倍潜力的币,和短期暴涨项目,可以关注我进社区了解,目前都是免费的