Bitcoin Ordinals, the non-fungible tokens minted on the world’s most valuable blockchain, have been the talk of the industry since they emerged virtually overnight earlier this year and quickly rose to prominence. Now they're providing serious competition to other networks, and changing trading behavior.

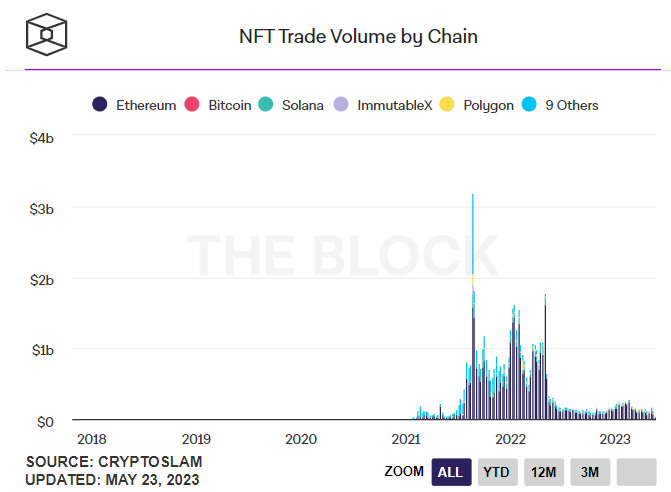

While Ethereum, long the dominant blockchain for NFTs, still ranks number one in terms of trading volume and is unlikely to lose that lead any time soon, Bitcoin has been maintaining a firm grip on second place for more than three weeks.

Besides frustrating rival chains like Solana and Polygon that have been consistently ranking second and third for several months, Bitcoin’s ascendance in the NFT space could have the knock-on effect of spurring a decline in wash trading which can sometimes distort markets.

“Wash trading” generally refers to artificial trading that, rather than representing genuine supply and demand, inflates trading volumes as parties trade between their own wallets. It's harder to do on the Bitcoin network when it comes to NFT trading.

“You can’t really create tokens and advance smart contracts on Bitcoin, thus making token incentives for trading near impossible and wash trading less likely,” said The Block Director of Research Steven Zheng.

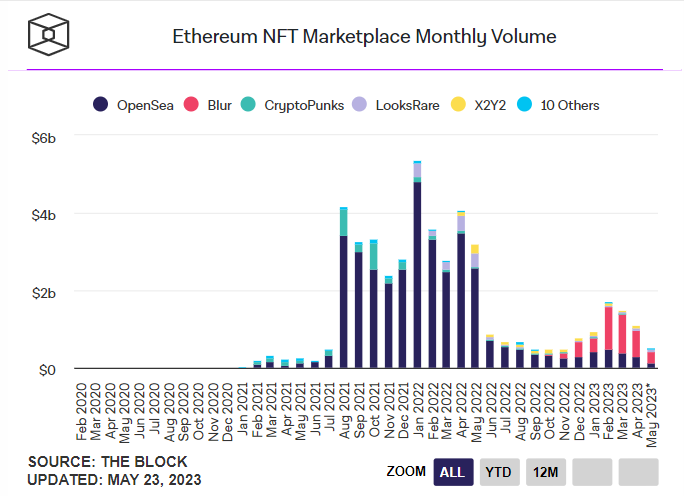

Before exchanges like LooksRare and Blur launched ambitious token-incentive programs designed to steal traders away from top NFT marketplace OpenSea, wash trading was minimal, according to Zheng. Most recently, Blur began awarding tokens to traders based on the total value of the trading they conducted on the marketplace.

Zheng illustrated the power of Blur’s incentives by providing the example of someone trading $1 million worth of NFTs on Blur in the hope of securing more than $1 million worth of BLUR tokens.

“This incentive mechanism doesn’t exist on Bitcoin," he said. "At least not yet.”

Can Bitcoin Ordinals help restore legitimacy to NFT markets?

At the end of last year, an online sleuth known as @hildobby_ on Twitter posted a Dune analytics dashboard which posited that more than $30 billion of transaction volume, and roughly 44% of all NFT trading, was in fact nothing more than wash trading. At its peak, according to the same dashboard, wash trading accounted for about 80% of the total volume of NFT trades.

Blur’s program, like LooksRare’s before it, led to many traders selling high-valued NFTs from collections like Bored Ape Yacht Club and CryptoPunks in order to collect tokens. During its February peak, Blur’s token hit a price of $1.24 on more than $600 million in trading amid a flurry of transactions on the NFT marketplace.

While trading can cause the NFT market to appear more robust than it actually is — weekly trading is still down more than more than 90% since the height of 2021's bull run — many argue it casts a pall over the industry for various reasons.

“Wash trading distorts the NFT market, creating an illusion of demand and value,” web3 advocate @kouk_web3 said in a Twitter thread from March. “It hurts trust, makes real investors vulnerable to losses, and can even lead to regulatory crackdowns.”

In a report published in 2022, leading blockchain analytics firm Chainanalysis agreed.

“NFT wash trading exists in a murky legal area," it said. "While wash trading is prohibited in conventional securities and futures, wash trading involving NFTs has yet to be the subject of an enforcement action. However, that could change as regulators shift focus and apply existing anti-fraud authorities to new NFT markets.”