NFT 专案「Milady Maker」因马斯克发梗图,交易量、地板价皆大幅上涨,相关代币「LADYS」也受益上涨,而先前早期进场PEPE 却被列为黑名单的交易员,他的地址这次也买了「LADYS」,又再次被团队黑单。

马斯克发Milady 梗图,NFT 地板价创新高

马斯克在5 月10 日晚间接近12 点时推文发布NFT 专案「Milady Maker」的图片。

NFTGO数据显示,这导致Milady 交易量暴涨1,805%,24 小时交易量超过8,000 ETH,成交量也上升1,185%。

24 小时涨幅48.22%。

pic.twitter.com/4s6HwnCY74

— Elon Musk (@elonmusk) May 10, 2023

Milady 是Remilia Collective 早在2021 年推出的NFT 专案,由艺术家Charlotte Fang所设计。

Milady 价格一直踌躇不前,2022 年5 月曾短暂突破1 ETH后便无起色,但今年1 月起再次站上1 ETH,在马斯克发文前日,价格也来到将近4 ETH。

而在马斯克助攻下,Milady 截稿前地板价约5.33 ETH。

甚至远高于许多NFT 蓝筹专案。

迷因代币Milady (LADYS) 涨超20 倍

迷因币LADYS 也因为马斯克推文而受益,自发文起截至目前涨幅2,269%,凌晨四点时涨幅甚至超过5,000%。

不过LADYS 这波上涨引发许多争议,包括争议风投DWF Labs 的早期进场、LADYS 获利地址又被合约部署者锁定,似乎满满的内幕。

(详述DWF Labs 争议行为:半年多笔千万美元等级投资,谜样机构DWF Labs回应仍遭质疑)

LADYS|15分线

迷样机构DWF Labs 5/9 进场LADYS

链上分析师@EmberCN指出DWF Labs 在5 月9 日即花费13.5 ETH (约2.5 万美元) 买进LADYS,当时还浮亏5,000 美元。

根据DWF Labs地址,这家机构在今天还不断加仓LADYS (再投入40 ETH),也买进了Milady #8277,截稿前持有的LADYS 价值已来到193 万美元。

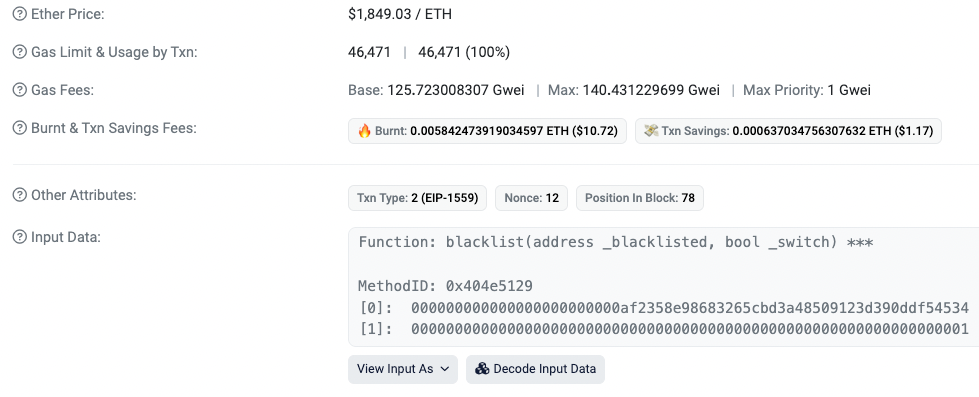

继PEPE 之后,同位早期进场者又被LADYS 黑单

此前报导,一地址在PEPE 上架Uniswap 不久后随即以0.013 ETH购入2.5 兆枚PEPE (目前价值400 万美元),但8 分钟后就遭到合约部署者将地址列为黑名单。

(社群对此事的臆测: 800万美元PEPE地址遭开发者列入黑名单,代币将永久锁定)

神奇的是,此地址0x…54534 也早在3 天前就以0.1 ETH 买进了1,053,249 LADYS。

而他又再次被LADYS 的合约部署者黑单,目前持有价值429 万美元的PEPE、959 万美元的LADYS。

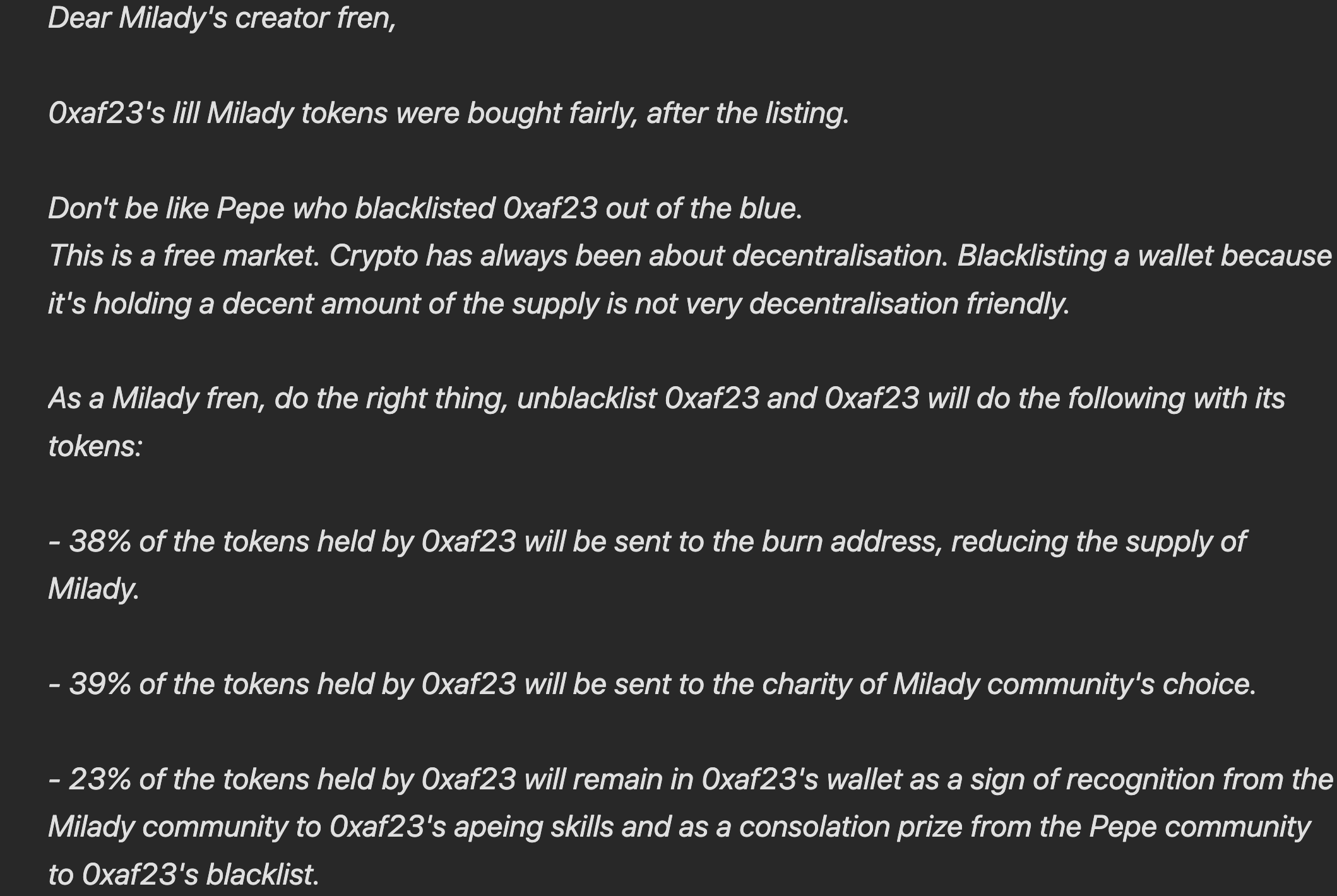

黑名单喊话LADYS:留23% 给我,其它捐掉

地址0x…54534 于链上留言向LADYS 团队表示,自己的代币是在上架后公开购买的,呼吁别像PEPE 团队将其黑单,这样做相当中心化。

若将其解除黑单,0x…54534 表示会将失而复得的代币执行以下操作:

38% LADYS 近行销毁,减少供应量。

39% 由Milady 社群自行选择慈善机构进行捐赠。

23% 留在原地址,作为Milady 社群对0x…54534「Ape in」技术的认可,也能当作无故被PEPE 黑名单的安慰补偿。

LADYS 团队也回覆表示:

对于黑名单一事我们已经有了结论,针对你的钱包也与PEPE 商讨中,后续能在Blockscan chat 讨论吗?

截稿前,双方尚未有更进一步讨论。

黑单者链上留言