Author: Tanay Ved, Coin Metrics

Compiled by: Luffy, Foresight News

TL;DR

- As blockchains scale and transaction costs decrease, the differentiation among public chains is shifting from cost competition to specialized, scenario-based division of labor.

- In March, the 20 millionth Bitcoin was mined. The ecosystem of wrapped tokens and ZK Rollups continues to grow, gradually unlocking Bitcoin's programmability and asset utility.

- Ethereum is consolidating its position as the hub for on-chain liquidity and settlement. L1 fees hit record lows, while L2s are evolving from scaling solutions into specialized execution layers.

- Solana is advancing its vision of an 'Internet Capital Market,' with increasing payment adoption and maturing on-chain trading infrastructure. The Alpenglow upgrade aims to achieve sub-second finality.

As network block space continues to expand, on-chain transaction costs have significantly decreased. Ethereum mainnet fees dropped notably after recent upgrades, Solana's fees remain under a few cents, and L2 networks offer similarly low-cost execution environments. In this context of compressed costs, the differentiation of block space increasingly depends on ecosystem liquidity, throughput, and scenario specialization, rather than mere marginal cost advantages.

This article explores how major public chains are evolving around their respective positions: Bitcoin is expanding its programmability and asset utility; Ethereum is consolidating its role as the liquidity and settlement center for stablecoins, real-world assets (RWA), and DeFi; and Solana is focusing on high-frequency payments and trading scenarios.

Bitcoin

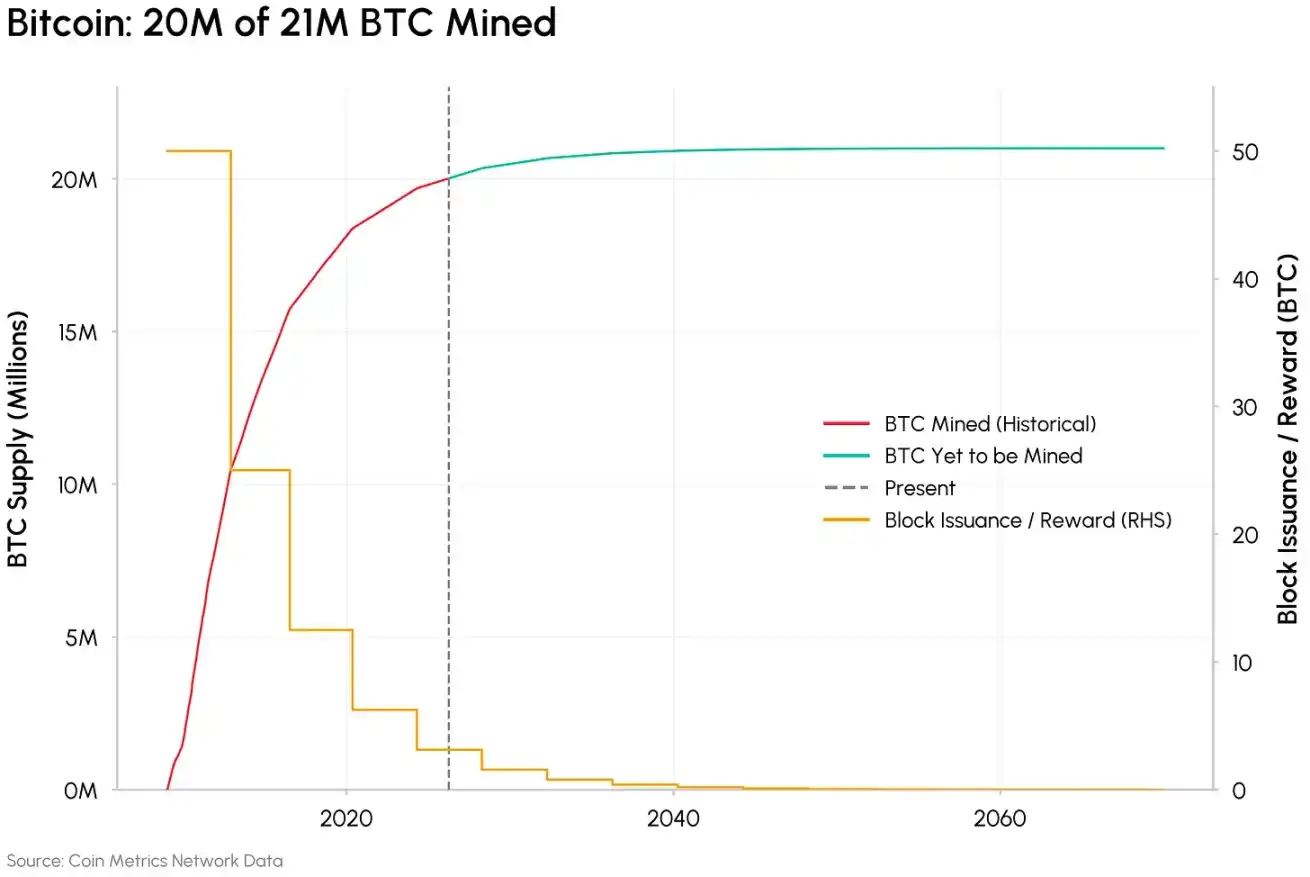

In March 2026, the 20 millionth Bitcoin was mined, meaning only 1 million BTC remain to be issued. Over 95% of Bitcoin's total supply is already in circulation. After the halving in April 2024, the block reward dropped to 3.125 BTC, and the issuance rate continues to decline as programmed.

Bitcoin mining speed, Data source: Coin Metrics

As block rewards decrease, the importance of transaction fees in miner revenue continues to grow. Excluding periods of sharp spikes, transaction fees account for less than 1% of total miner income. Since all Bitcoin fees go to miners, a core long-term issue for its security model is whether naturally occurring fee demand can sustainably fill the gap left by declining block rewards.

Making Bitcoin Programmable and Assetized

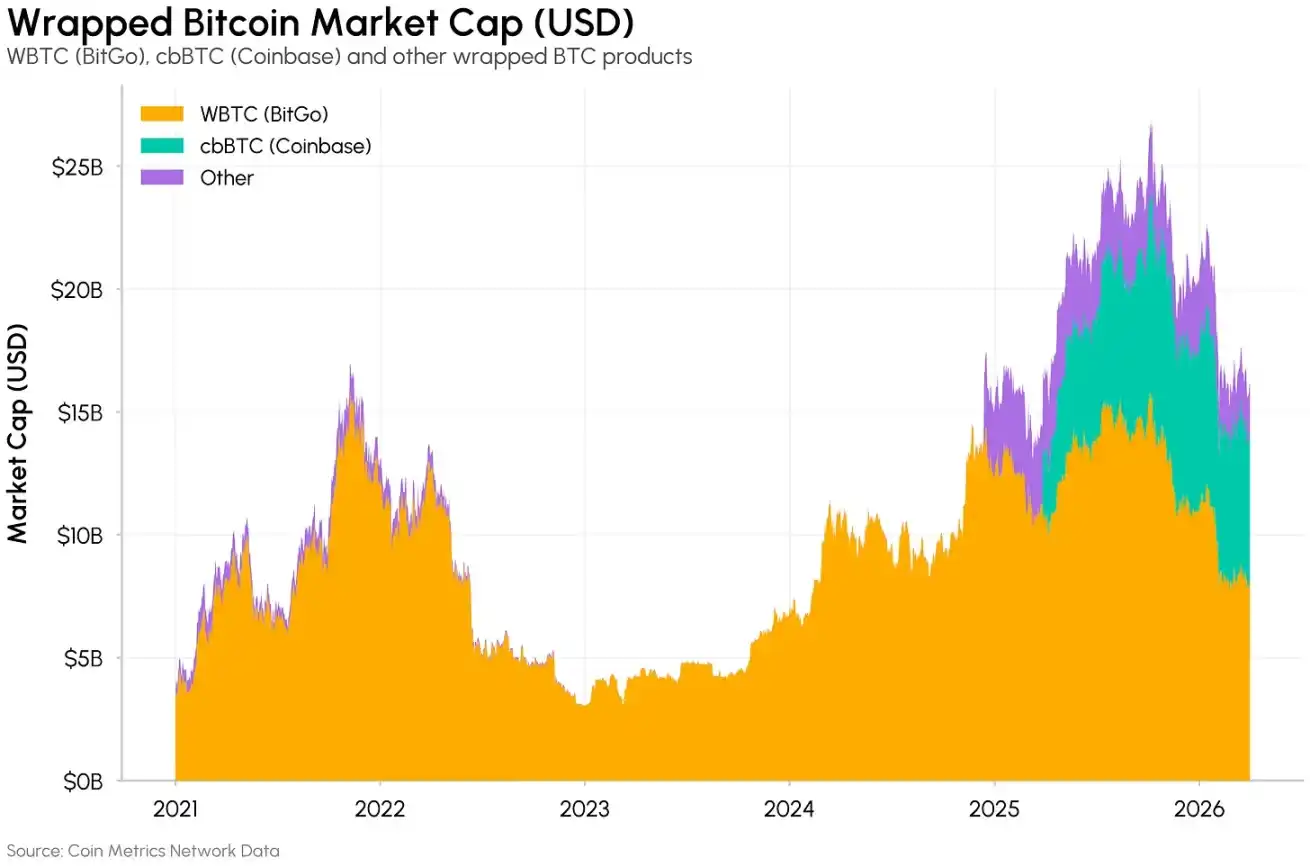

Despite a market cap of approximately $1.3 trillion, about 60% of BTC has not moved in a year; around 2.4 million BTC (11% of the supply) is held on centralized exchanges, and another ~243,000 BTC circulates as wrapped tokens on other public chains.

Most Bitcoin capital remains idle, and the vast majority of related activity and fee generation occurs off the main chain.

Bitcoin's functional role is evolving along two main lines: expanding base-layer programmability and enhancing BTC's asset utility. Sidechains, L2s like Lightning Network, wrapped Bitcoin, and liquid staking protocols are enriching Bitcoin's practicality, but they also introduce varying degrees of trust assumptions, ranging from fully custodial to smart contract-based.

Market cap of wrapped Bitcoin, Source: Coin Metrics

In the direction of minimal trust, Citrea stands out as a ZK Rollup that settles directly on Bitcoin L1. It uses the BitVM framework to verify programs within Bitcoin's existing script system, enabling EVM-compatible applications, with security guaranteed by Bitcoin's proof-of-work. Unlike sidechains, it settles directly on Bitcoin via zero-knowledge proofs, with withdrawals relying on non-custodial bridges.

Simultaneously, the use of BTC as collateral continues to grow. The total value of wrapped Bitcoin across various chains exceeds $15 billion, and the lending market for Coinbase's cbBTC on Morpho has surpassed $1 billion. Liquid staking protocols like Babylon further expand this scenario, allowing BTC to provide economic security for external proof-of-stake networks. These developments are gradually unlocking the assetization potential of long-idle capital.

Ethereum

Ethereum remains the global center for on-chain liquidity and settlement. It holds about 62% of the total stablecoin market cap, boasts the deepest DeFi liquidity of any public chain, and is also a key platform for circulating tokenized real-world assets (RWA), including money market funds, tokenized treasuries, and stocks.

Recent upgrades have further strengthened Ethereum's底层 (base layer) position as the core of economic activity. PeerDAS, larger blob space, and the increased Gas limit from the Pectra and Fusaka upgrades have pushed L1 fees to multi-year lows, expanding the range of activities that can be settled directly on the mainnet.

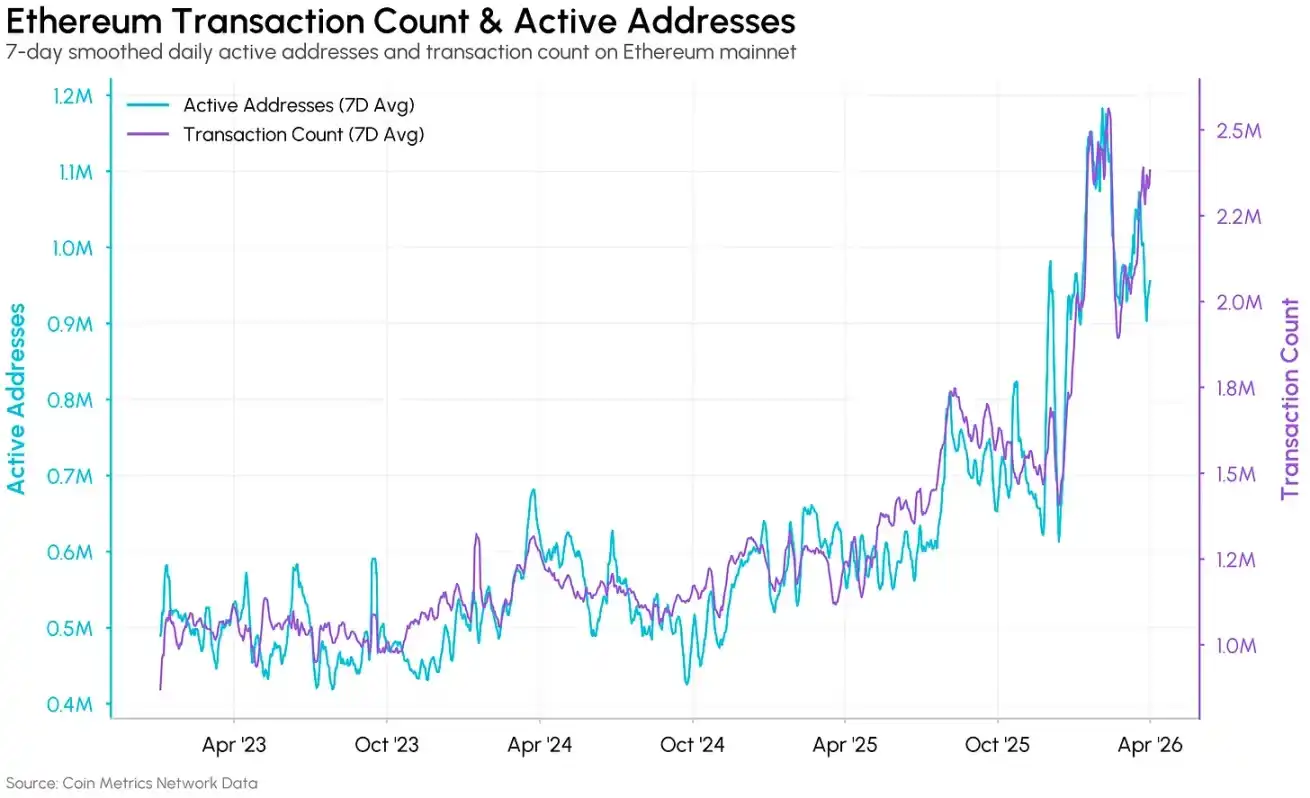

Ethereum transaction volume and active address count, Data source: Coin Metrics

Daily active addresses and transaction volume on Ethereum mainnet have nearly doubled year-over-year, exceeding 1 million and 2.4 million respectively. However, as we previously noted, part of this growth comes from address poisoning attacks and low-value economic activity addresses (transaction value less than $1), which sometimes constitute a very high proportion of daily active addresses.

The Evolving Relationship Between L1 and L2

With L1 transaction costs significantly reduced, the role of Ethereum L2 networks is being redefined. L2s were initially designed as core scaling solutions for Ethereum, reducing costs by offloading the execution layer. This positioning is now changing.

According to a recent Ethereum Foundation blog post, the core mission of L2s has shifted to providing differentiated functions, customized capabilities, and specialized execution environments, with scaling becoming a secondary function.

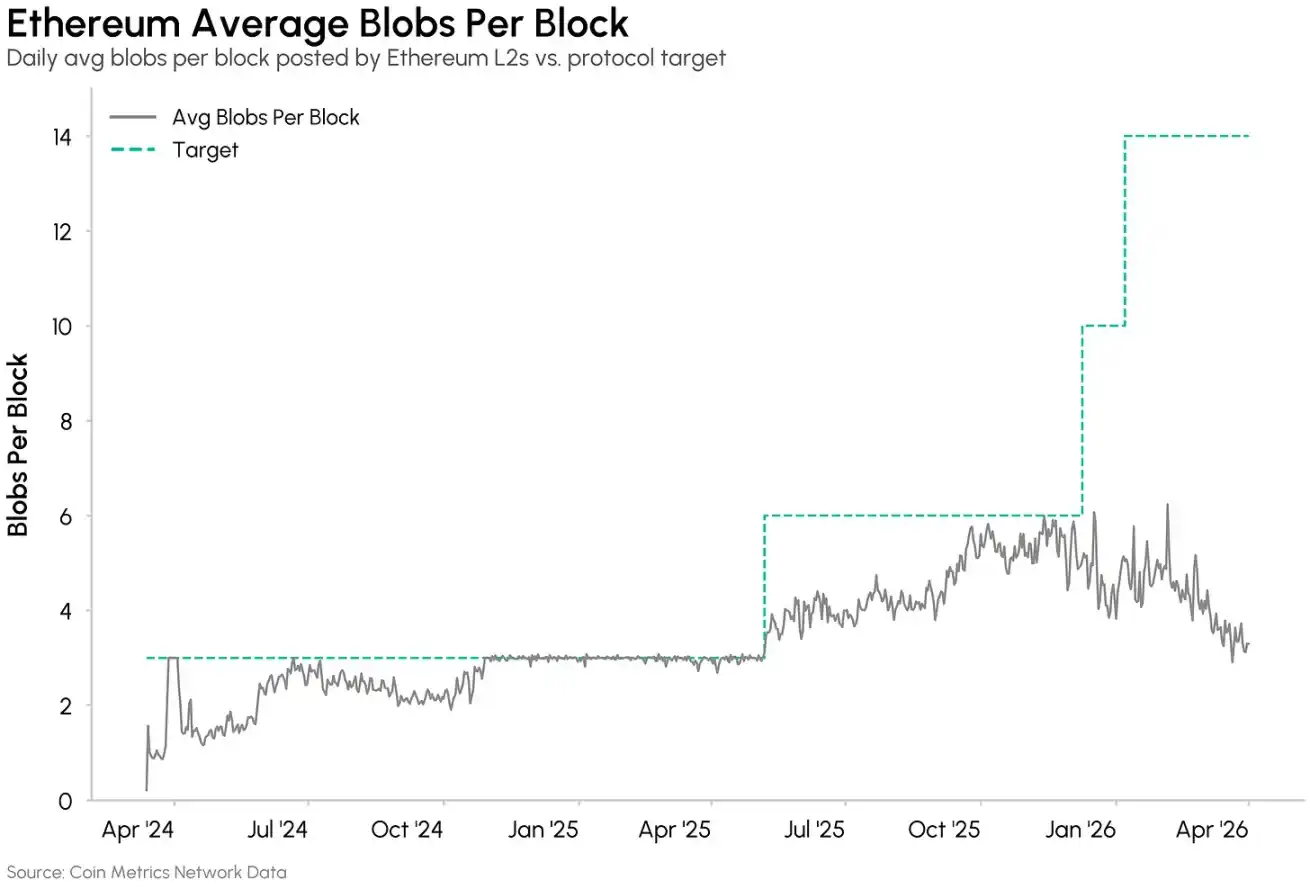

L2 usage of blob space for submitting transaction data to Ethereum is below 30%, with an average of about 3 blobs per block post-scaling. Blob usage is concentrated on a few L2s, and related fees constitute a negligible portion of total transaction fees. The pace of L1 scaling has now surpassed L2 settlement demand, making Ethereum settlement costs no longer a barrier for most L2s.

Average number of blobs per block on Ethereum, Data source: Coin Metrics

The L2s achieving sustained growth are those with unique value propositions: Base leverages Coinbase's distribution advantages, Arbitrum stands on its deep DeFi liquidity. A new generation of specialized chains like MegaETH, Lighter, Robinhood Chain, and Ink target specific scenarios, offering new business models and distribution channels.

The Ethereum roadmap, through native rollups and other interoperability and minimal-trust architectures, further promotes deep integration between L1 and L2, consolidating its position as the core of ecosystem liquidity and settlement.

Glamsterdam and Other Upgrades

The Glamsterdam upgrade, scheduled for the first half of 2026, will continue this trend. By increasing the Gas limit to 200 million and introducing parallel transaction execution, this upgrade aims to significantly increase L1 throughput while reducing fees for complex smart contract interactions. Additionally, the Proposer-Builder Separation mechanism (ePBS) integrates block building into the protocol, reducing MEV centralization and improving transaction ordering transparency. These changes are designed to make Ethereum L1 a more competitive execution environment, maintaining its status as a trusted platform for high-value settlement and DeFi.

Solana

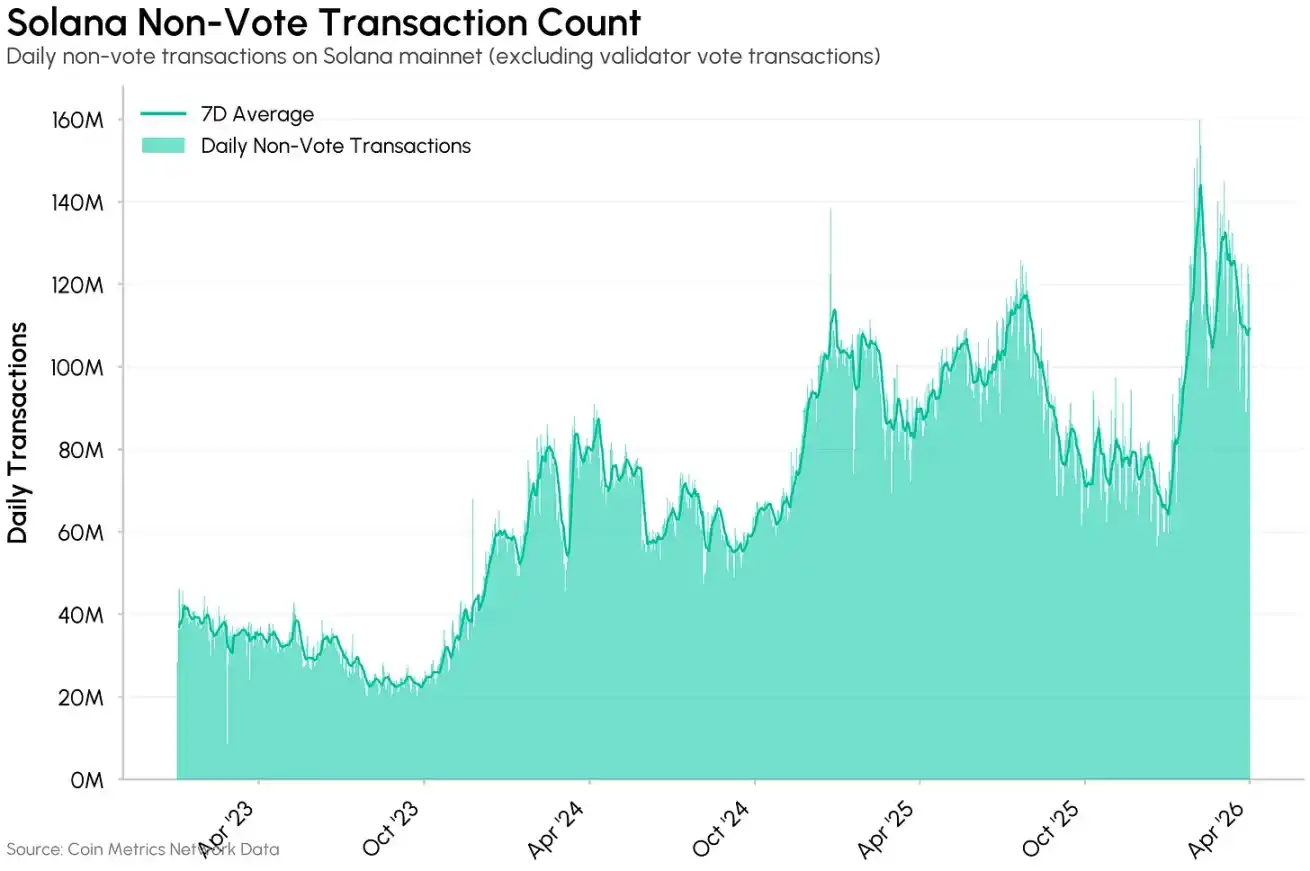

Solana is shedding its early label as a 'retail and meme coin chain' and moving towards its vision of an Internet Capital Market. With transaction fees under 1 cent and block times below 400 milliseconds, it is a natural fit for high-frequency applications like payments, micropayments, and high-frequency trading. This characteristic attracts a range of professional applications requiring large-scale, low-latency execution.

Since late 2024, non-vote transactions on Solana have nearly doubled, exceeding 120 million daily on average.

Number of non-vote transactions on the Solana network, Data source: Coin Metrics

Payments and High-Frequency Micropayments

Solana's low-cost environment makes it a top public chain for payments and peer-to-peer value transfer. Daily USDC transfers under $1000 are stable at around 3 million, with the median transaction amount consistently below $100.

An emerging development is the x402 protocol, an open HTTP payment protocol launched by Coinbase that allows any API or digital service to charge stablecoin fees per request. Despite competition from chains like Base and Stripe's Tempo, Solana captures a significant share of x402 transactions, becoming an early adoption layer for agent micropayments.

Trading Infrastructure

Solana's high throughput also attracts professional on-chain trading infrastructure. Proprietary AMMs (propAMMs) developed by professional market makers use private off-chain pricing models, resembling dark pools more than public DEXs. Unlike AMMs like Uniswap, which are susceptible to front-running and arbitrage, propAMMs update prices off-chain and settle on Solana, offering MEV resistance.

Alpenglow and Other Upgrades

Upcoming infrastructure upgrades will further strengthen Solana's advantages. Alpenglow replaces the original consensus with the lightweight vote aggregation protocol Votor, aiming to reduce block finality time from about 12 seconds to 100–150 milliseconds. The block assembly market developed by Jito allows trading applications to control transaction ordering themselves, supporting features like cancellation priority, thus improving execution fairness.

Conclusion

As block space expands and costs compress, the core of competition in the public chain industry is shifting from cost to specialized division of labor. Major public chains leverage their architectural strengths to meet diverse scenario needs; dedicated chains like Hyperliquid, Canton, Arc, and Tempo are optimized around application requirements, making clear trade-offs in permissioning, compliance, and execution design. A key question for the future is how the industry landscape will evolve when on-chain demand truly scales massively.

The entire on-chain infrastructure still faces common risks. A Google Quantum AI paper on March 31st suggested that the number of physical qubits required to break the elliptic curve cryptography underlying major blockchains like Bitcoin and Ethereum could be below 500,000, only 1/20th of the previous estimate of 20 million. Early solutions like Bitcoin's BIP-360 and Ethereum's post-quantum roadmap are beginning to take shape. A deeper challenge lies in coordinating community consensus and voluntary adoption within decentralized networks, a process that may be slower and less predictable than in centralized institutions.