Abstract

Based on the article "Truth, Bubbles, and Illusions: A Look Back at the 2025 Crypto Report Card," here is a summary of its main points:

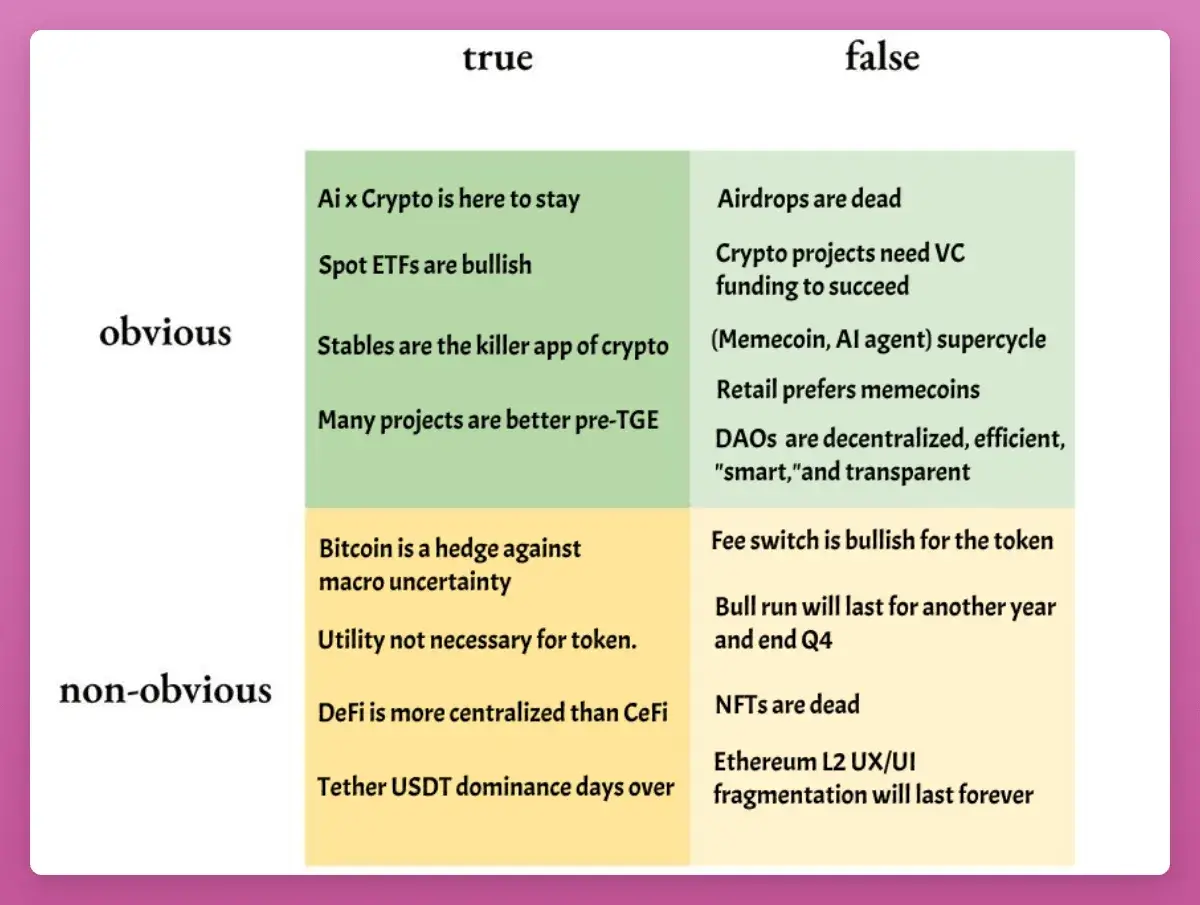

The author reflects on their 2025 predictions for the crypto market. They admit to being wrong about Bitcoin's peak in Q4, as the cycle held, and wrong about a memecoin or AI agent supercycle, as retail investors favored traditional assets like gold and AI stocks instead. The AI x Crypto narrative saw mixed results with project development but poor token performance, and NFTs were declared "dead."

Key insights from 2025 include:

1. **Bitcoin ETFs acted as a floor, not a ceiling:** Massive selling by long-term holders created a $95B supply overhang, causing BTC to underperform. However, its correlation with traditional risk assets fell, which is bullish long-term.

2. **Airdrops are not dead:** Nearly $4.5B was airdropped in 2025 (e.g., Story Protocol, Berachain). The game has shifted towards requiring more focused, high-conviction farming due to points fatigue and better Sybil detection.

3. **Fee switches set a price floor, not an engine for growth:** Token buybacks from fees establish a bottom price but don't guarantee appreciation, as seen with UNI's price action. The market treats everything as a trade.

4. **Stablecoins gained traction for payments, but "proxy trading" was difficult:** Stablecoins like USDT saw real-world adoption for payments. However, investing in related equities (e.g., Circle's IPO) proved challenging, as gains we...

Author: Ignas

Compilation: Plain Talk Blockchain

Original Title: Crypto Truth and Lies: A Review of the 2025 Report Card

A year ago, I wrote "Truth and Lies of the 2025 Crypto Market".

At that time, everyone was sharing higher Bitcoin price targets. I wanted to find a different framework to discover where the public might be wrong and to position myself differently. The goal was simple: to seek out ideas that already existed but were overlooked, disliked, or misunderstood.

Before sharing the 2026 edition, here is a clear review of what truly mattered in 2025. What we got right, what we got wrong, and what we should learn from it. If you don't examine your own thinking, you're not investing, you're guessing.

Quick Summary

-

"BTC Peaked in Q4": Most people expected this, but it seemed too good to be true. Turns out they were right, and I was wrong (and paid the price). Unless BTC skyrockets from here and breaks the 4-year cycle pattern, I'll concede this one.

-

"Retail Prefers Memecoins": The truth is, retail doesn't prefer crypto at all. They bought gold, silver, AI stocks, and anything that wasn't cryptocurrency. The supercycle for memecoins or AI Agents also did not materialize.

-

"AI x Crypto Remains Strong": Mixed results. Projects continued to deliver, the x402 standard evolved, and funding continued. But tokens failed to sustain any rallies.

-

"NFTs Are Dead": Yes.

These are easy to review in hindsight. The real insights lie in the following five larger themes.

1. Spot ETFs Are the Floor, Not the Ceiling

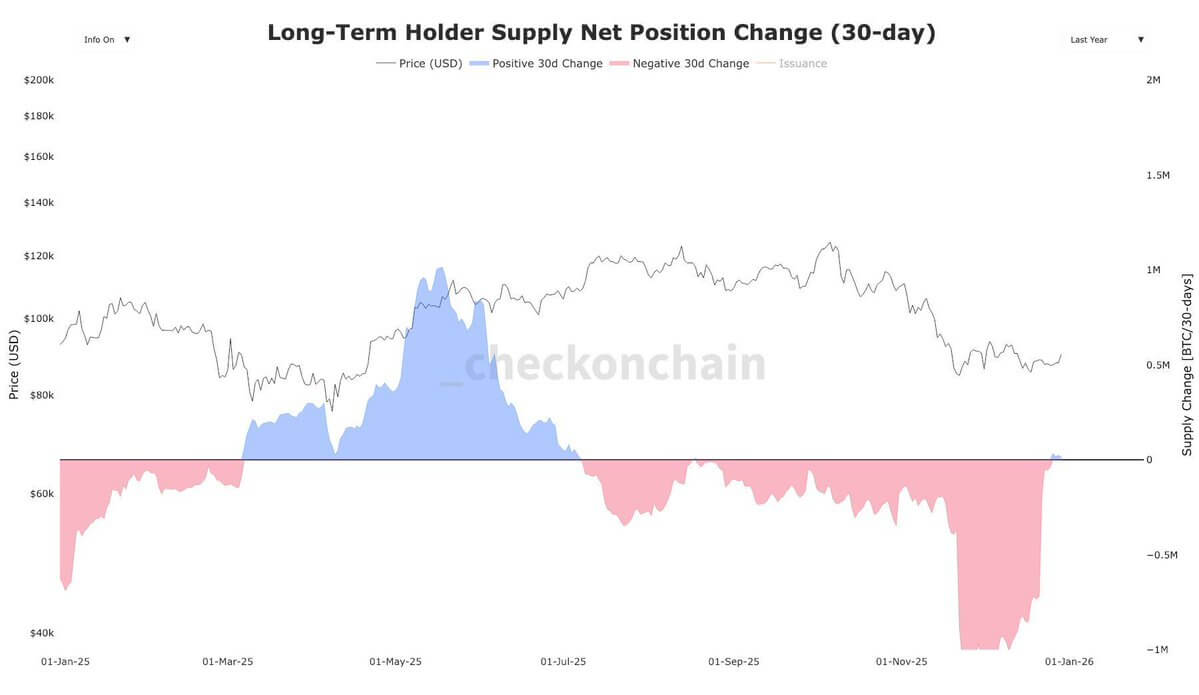

Since March 2024, long-term Bitcoin holders (OGs) have sold approximately 1.4 million BTC, worth about $121.17 billion.

Imagine the bloodbath in the crypto market without ETFs: Despite the decline in price, BTC ETF inflows remained positive ($26.9 billion).

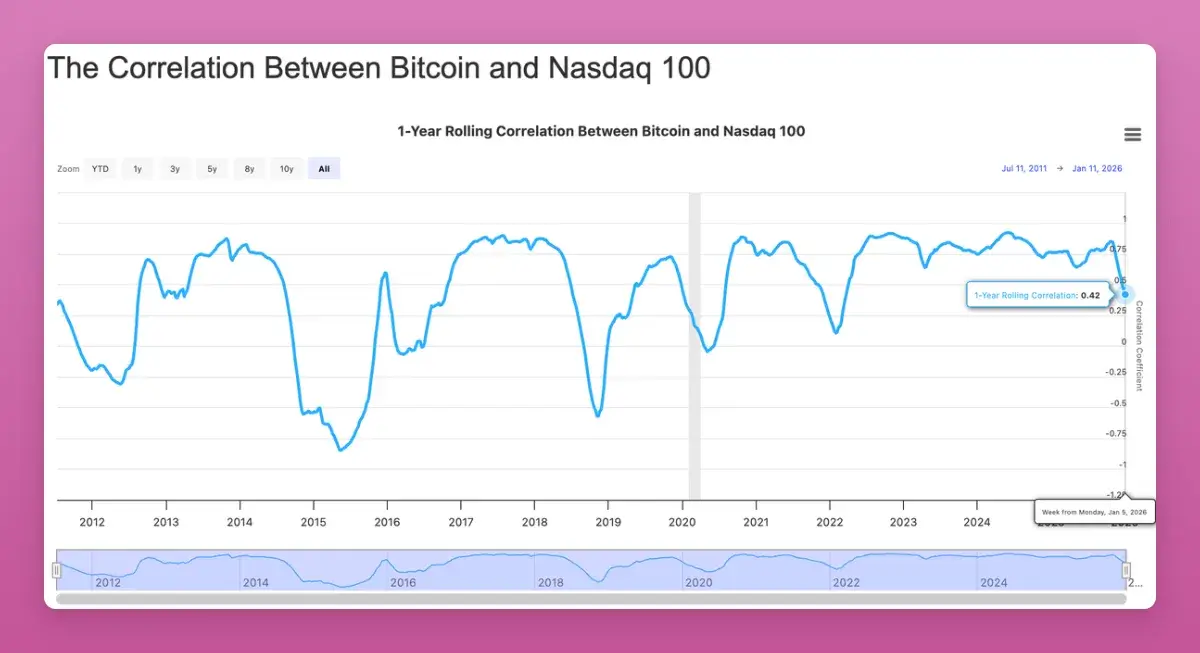

The gap of about $95 billion is precisely why BTC underperformed almost all macro assets. There's nothing wrong with BTC itself; you don't even need to dig deep into unemployment or manufacturing data to explain it—it's just the "great rotation" by whales and "4-year cycle believers".

More importantly, Bitcoin's correlation with traditional risk assets like the Nasdaq fell to its lowest since 2022 (-0.42). While everyone hoped for an upward breakout in correlation, in the long run, this is bullish as an uncorrelated portfolio asset sought by institutions.

There are signs the supply shock is over. Therefore, I dare to predict a BTC price of $174,000 for 2026 (equivalent to 10% of gold's market cap).

2. Airdrops Clearly "Did Not" Disappear

The crypto community (CT) once again claimed airdrops were dead. But in 2025, we saw nearly $4.5 billion in large airdrop distributions:

-

Story Protocol (IP): ~$1.4B

-

Berachain (BERA): ~$1.17B

-

Jupiter (JUP): ~$7.91M

-

Animecoin (ANIME): ~$7.11M

The changes are: points fatigue, stronger Sybil detection, and lower valuations. You also need to "claim and sell" to maximize returns.

2026 will be a big year for airdrops, with heavyweights like Polymarket, Metamask, Base(?) preparing to launch tokens. This is not the year to stop clicking buttons, but to stop betting blindly. Airdrop "farming" requires concentrated effort on high-conviction bets.

3. Fee Switches Are Not Price Appreciation Engines, They Are the Floor

My prediction was: Fee switches won't automatically drive token prices up. Most protocols don't generate enough revenue to support their massive market caps.

"The fee switch doesn't affect how high the token can go; it sets a 'floor price'."

Look at the projects ranked by "Holder Revenue" on DeFillama: Except for $HYPE, all high revenue-share tokens outperformed ETH (though ETH is now the benchmark everyone challenges).

The surprise was $UNI. Uniswap finally flipped the switch and even burned $100 million worth of tokens. UNI initially surged 75% but then gave back all its gains.

Three revelations:

Token buybacks set a price floor, not a ceiling.

Everything this cycle is a trade (refer to UNI's pump and dump).

Buybacks are only one side of the story; sell pressure (unlocks) must be considered, as most tokens are still low float.

4. Stablecoins Capture Mindshare, But "Proxy Trading" Is Hard to Monetize

Stablecoins are going mainstream. When I rented a motorbike in Bali, the owner even asked for payment in USDT on TRON.

Although USDT's dominance fell from 67% to 60%, its market cap is still growing. Citibank predicts the stablecoin market cap could reach $1.9 to $4 trillion by 2030.

In 2025, the narrative shifted from "trading" to "payment infrastructure". However, trading the stablecoin narrative wasn't easy: Circle's IPO gave back all its gains after an initial surge, and other proxy assets also underperformed.

One truth of 2025: Everything is just a trade.

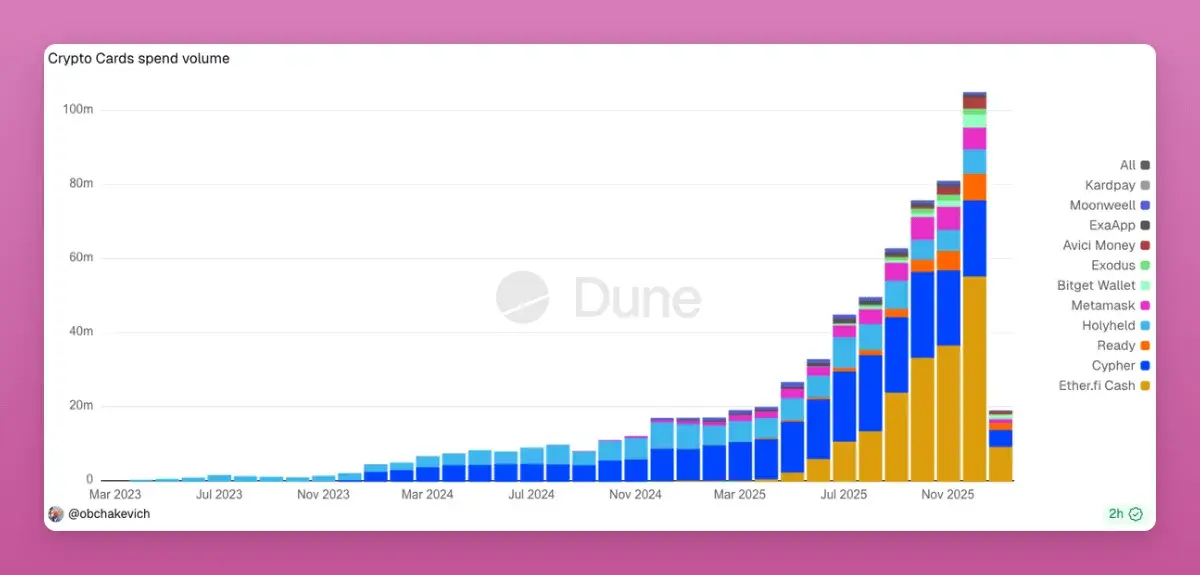

Currently, crypto payment cards are exploding due to their convenience in bypassing strict bank AML requirements. Every card swipe is a transaction on-chain. If direct peer-to-peer payments bypassing Visa/Mastercard emerge in 2026, that would be a 1000x opportunity.

5. DeFi Is More Centralized Than CeFi

This is a bold claim: DeFi's business and TVL concentration is higher than that of traditional finance (CeFi).

Aave commands over 60% of the lending market share (compared to JPMorgan's 12% in the US).

L2 protocols are mostly multi-billion dollar unregulated Multisigs.

Chainlink controls almost all value oracles in DeFi.

In 2025, the conflict between "centralized equity holders" and "token holders/DAO" became apparent. Who truly owns the protocol, IP rights, and revenue streams? The internal dispute at Aave showed that token holders have fewer rights than we thought.

If the "Labs" ultimately win, many DAO tokens will become uninvestable. 2026 will be a crucial year for aligning the interests of equity and token holders.

Summary

2025 proved one thing: Everything is a trade. Exit windows are extremely short. No token has long-term conviction.

As a result, 2025 marked the death of HODL culture, DeFi turned into Onchain Finance, and with improving regulation, DAOs are shedding their "pseudo-decentralized" disguise.

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush

Original link:https://www.bitpush.news/articles/7601755

Related Questions

QWhat was the author's main prediction about Bitcoin's price cycle in 2025, and were they correct?

AThe author predicted that Bitcoin would peak in Q4 of 2025, but they were wrong. The market followed the expected four-year cycle, and the author admitted to paying the price for this incorrect prediction.

QAccording to the article, what was the state of the NFT market in 2025?

AThe article states that NFTs were dead in 2025, confirming the author's previous prediction.

QHow did the performance of tokens with fee switches (like UNI) compare to the author's expectations?

AThe author predicted that fee switches would not automatically drive token prices up but would instead set a price floor. This was confirmed when UNI initially surged 75% after its fee switch was activated but then gave back all its gains, showing that buybacks set a price bottom, not a ceiling.

QWhat significant shift occurred in the stablecoin narrative in 2025?

AThe narrative for stablecoins shifted from 'trading' to 'payment infrastructure' in 2025, as their use for real-world payments grew, exemplified by instances like a Balinese motorbike rental requesting payment in USDT on the TRON network.

QWhy does the author argue that DeFi is more centralized than CeFi?

AThe author argues that DeFi is more centralized due to extreme market concentration: Aave holds over 60% of the lending market share (compared to JPMorgan's 12% in the U.S.), L2 protocols are run by multi-sigs, and Chainlink dominates the oracle market for DeFi.

Related Reads

In Conversation with Ray Dalio: We Are Currently in an AI Bubble, with 1% of My Portfolio in Bitcoin

Ray Dalio, founder of Bridgewater Associates, warns in an interview that the current AI boom shows classic bubble characteristics, which could lead to significant economic downturns as seen in past cycles like 1929 or 2000. He explains that speculative enthusiasm, fueled by debt and overvaluation, often precedes a crash when rising rates or taxation force asset sales, causing widespread losses and recession.

Dalio also outlines his "Big Cycle" theory, describing an approximate 80-year pattern where widening wealth gaps, massive government deficits, and shifting geopolitical power (like China's rise) create internal conflict and global instability. He emphasizes that we are in a late-cycle, transitional phase where traditional powers like the US and UK face decline.

For personal wealth protection, Dalio advises diversification beyond cash into assets like stocks, bonds, real estate, and particularly gold, which he prefers over Bitcoin. While he holds about 1% of his portfolio in Bitcoin as a non-printable hard asset, he views gold as more secure from technological or governmental threats.

Regarding AI's impact, Dalio believes it will disproportionately benefit capital owners, worsening inequality by replacing both physical and cognitive labor. He suggests that human intuition and emotional intelligence, combined with AI, will be key for future workers.

On taxation, Dalio argues that wealth taxes are impractical and risk triggering asset sell-offs, reducing productive investment. He points to the UK as a cautionary example of debt, low productivity, and political strife.

Geopolitically, Dalio foresees a more regionalized world, with the US showing weakness in prolonged conflicts like with Iran, akin to past imperial declines. The ideal outcome, he suggests, is coexisting powerful blocs (e.g., Americas, China-Asia Pacific) without major war.

marsbit2h ago

marsbit2h ago

Daily 7.2 Trillion KRW: Foreign Capital's Record Net Buying on Friday! Wall Street Says Headwinds for Korean Stock Fund Flows Have Subsided

South Korean stock market sees a dramatic shift in fund flows. On July 31, foreign investors made a record net purchase of approximately KRW 7.2 trillion in KOSPI stocks, marking a fundamental reversal from the persistent large-scale net outflows seen in previous months. This contributed to a significant narrowing of foreign net selling in July to KRW 9.8 trillion, down sharply from KRW 48.4 trillion in June and KRW 44.5 trillion in May.

Simultaneously, domestic institutional pressure eased. South Korean pension funds and asset managers turned to a net buying position in July, purchasing KRW 1.0 trillion worth of KOSPI shares, contrasting with net sales in May and June.

Market volatility is expected to be dampened by new financial regulations. Effective July 31, the Financial Services Commission tightened access for retail investors to single-stock leveraged ETFs by raising the minimum cash deposit requirement. Trading volumes for these products subsequently dropped to about 50% of their monthly average.

Citigroup Research maintains its year-end KOSPI target of 10,000 points. The firm cites several supportive factors: the substantial easing of headwinds from capital outflows, a robust fundamental outlook for the semiconductor sector, historically low market valuations, strong economic fundamentals, and the potential for policy support from financial authorities if needed.

marsbit2h ago

marsbit2h ago

How to Make Yourself Irreplaceable by AI Forever

This article argues that the primary threat from AI is not job replacement, but remaining trapped in "wage slavery"—financial dependence on employers. The path to becoming irreplaceable is not resisting AI, but becoming an "unemployable" individual who builds their own meaningful enterprise. The author identifies five key elements for this: Agency (acting without permission), Taste (judging what's worthwhile), Persuasion, Persistence, and Iteration.

The solution is to stop being a "pawn" in someone else's game. To start, you must fundamentally change your identity and environment, then engage in rapid, real-world trial and error. While both coding and creating media (content) are powerful, content is more crucial. AI can generate assets, but true value lies in subjective, human-driven content that builds trust and narrative.

The actionable advice is to carve out 15 minutes to answer foundational questions: 1) Uncover your "raw material"—what you know deeply or solve effortlessly. 2) Define your contrarian perspective—what common beliefs you think are wrong. The intersection of these answers is your direction. Finally, you must launch by publishing your first core idea immediately, using the feedback to iterate and develop the skills needed for a self-directed life and career.

marsbit4h ago

marsbit4h ago

Thanks to Dice Rolls, Bitcoin Keys Are Stored Offline, But Not Everyone Will Do It

The article discusses using dice rolls to generate secure Bitcoin wallet seeds, providing entropy independent of potentially flawed hardware random number generators. It explains that each fair dice roll offers about 2.585 bits of entropy, with around 50 rolls needed for a standard 12-word seed phrase and 99+ recommended for higher security. This method gained attention after a vulnerability was revealed in some Coldcard hardware wallets, where a faulty firmware RNG (dating back to 2021) compromised generated keys. The analysis notes that while a dice-generated main seed was safe from this specific flaw, other Coldcard functions (like creating paper wallets, backup keys, or passwords) could still be vulnerable if they used the defective RNG. The piece argues that while dice-based entropy is technically robust, the manual process is error-prone, tedious, and unrealistic for most new users, who might make mistakes in recording or inputting rolls. It concludes that while manual entropy generation should remain an option for advanced users, the long-term goal is to develop reliable, user-friendly hardware and software that securely generates randomness without requiring specialized knowledge. Coldcard users are advised to check their firmware version and replace any secondary secrets (like paper wallet keys) created with vulnerable devices, while also considering multi-signature setups with devices from different manufacturers for added security.

cryptonews.ru7h ago

cryptonews.ru7h ago