Author: FintechFrank

Compiled by: Deep Tide TechFlow

Deep Tide Guide: This article captures an ongoing structural shift: Trump's habit of making market-moving statements after the market closes, which coincides with the rise of 24/7 trading infrastructure. The S&P 500 proxy product on Hyperliquid experienced three significant fluctuations triggered by Trump's tweets over the same weekend. This is not a coincidence but a preview of a new normal.

Full Text Below:

Trump calls himself the "Crypto President," but in many ways, he is also the "Perpetual Contracts President."

It is well-known that Trump doesn't sleep, and he doesn't hesitate to make statements that can shake the market outside of traditional trading hours. This is a peculiar yet fitting backdrop: the market is evolving toward 24/7 trading, and we happen to have a president who can best be described as "spontaneous and sometimes chaotic."

This dynamic was fully demonstrated over the weekend.

Just days after S&P Global announced it would authorize trading of the S&P 500 on Hyperliquid, Trump stated on Friday afternoon after the market closed that the U.S. is "very close to achieving our goals." The S&P 500 proxy product on Hyperliquid immediately rose.

Then, on Saturday at 7:44 PM Eastern Time, Trump escalated his threats, warning that he would strike Iran's power facilities if the Strait of Hormuz was not reopened. The reaction was instantaneous: the S&P 500 on Hyperliquid immediately fell.

But it didn't end there. On Monday morning, Trump claimed that the U.S. and Iran had held talks on a "comprehensive and thorough resolution of hostilities." S&P 500 futures surged by over 3.5%. Iran later denied Trump's statement.

Trump's presidency may not be driving the arrival of 24/7 markets, but it has made it impossible to ignore the issue.

It remains unclear which perpetual contract product will dominate or whether perpetual contracts will become the primary structure for 24/7 markets. Futures have historically been far less familiar to U.S. retail investors than options, and whether traditional brokerages can successfully promote these products to their customer base remains an open question. I am skeptical. What works in crypto markets may not seamlessly translate to traditional finance users.

Nevertheless, growth is undeniable.

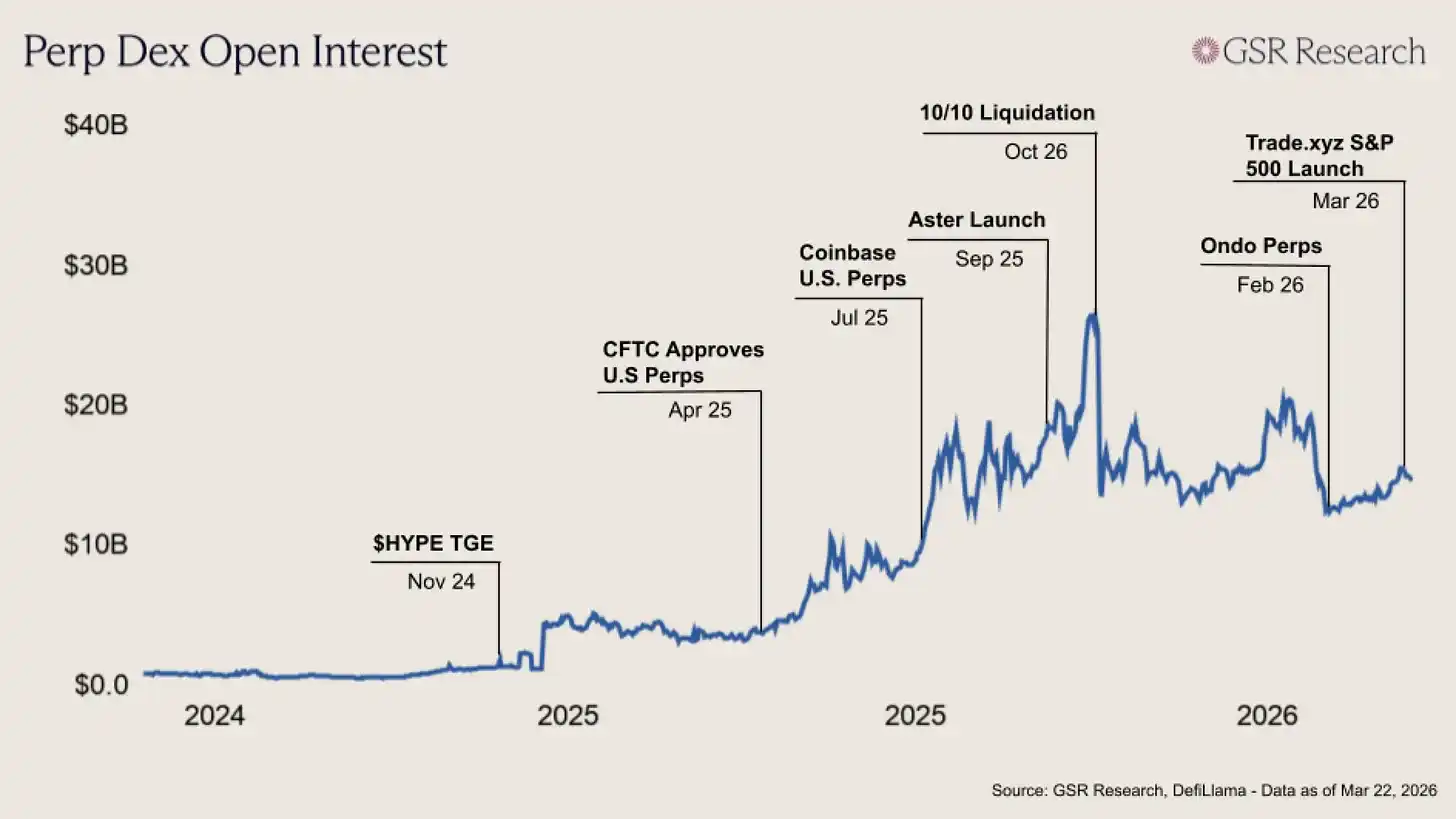

The open interest on perpetual contract DEX platforms has surged significantly. In January 2026, the trading volume of perpetual contract DEXs reached $739 billion, accounting for 10.2% of the total crypto perpetual contract trading volume on decentralized platforms—compared to just 2.0% two years ago.

As Carlos Guzman and Slater Santer of GSR Research show in the chart, news flow in both centralized and decentralized perpetual contract markets has accelerated since the HYPE TGE:

This morning, there was further momentum within the GSR ecosystem:

Katana acquired the early decentralized exchange IDEX and launched Katana Perps, a platform designed to unify spot and derivatives trading on-chain. This is the first major move by CEO Matthew Fisher since taking office, reflecting a pursuit of controlling more of the trading stack and capturing greater economic value.

This move also highlights a broader shift: the environment for perpetual contracts is becoming increasingly favorable. Here’s how Katana put it:

"This move coincides with U.S. regulators sending clear signals allowing crypto perpetual contracts, marking a potential inflection point for on-chain derivatives. At the same time, trading activity continues to migrate toward 24/7 markets, with price discovery increasingly happening in real-time rather than during fixed trading hours. As global markets adapt to new realities, macro risks no longer wait for trading hours, reinforcing the importance of a continuous 24/7 trading environment."