Author: BlockBeats

Undoubtedly, the current main narrative within the Base ecosystem remains AI. To be more precise, it's "VVV."

Before introducing the tokens related to the "VVV" concept, let's first understand what "VVV" actually is.

What is the "VVV" Concept?

$VVV is the token of Venice, which is a privacy-first and censorship-resistant generative AI platform on the Base ecosystem, led by Erik Voorhees.

Erik is a seasoned OG in the crypto space since 2011, having played a pivotal role in early Bitcoin adoption. After the Mt.Gox collapse, he founded ShapeShift, one of the first platforms to emphasize non-custodial and privacy-first trading. His expertise in decentralized finance and user sovereignty makes him a strong advocate for permissionless AI.

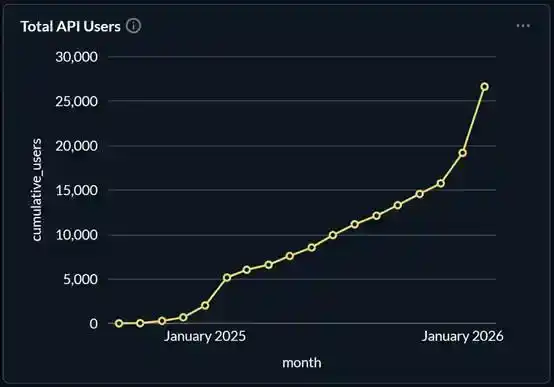

According to the Venice API user statistics chart disclosed by Erik Voorhees in March, Venice's API user count grew from near zero to 15,000 throughout 2025.

However, the corresponding price performance of $VVV has been lukewarm, with occasional rebounds reaching only about a $200 million market cap at most. It once fell below a $45 million market cap, far from its all-time high of nearly $1 billion when it first launched.

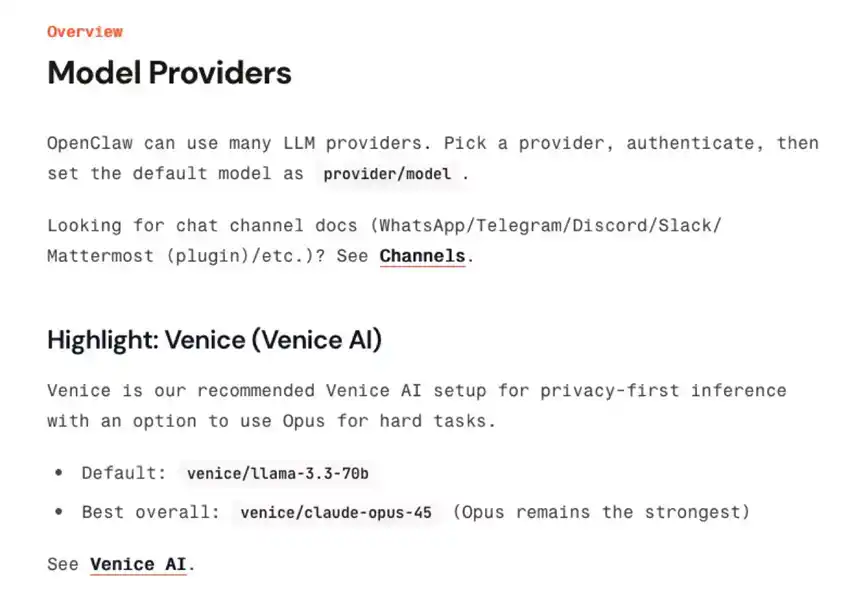

It's also noticeable that entering 2026, Venice's API user count experienced rapid growth. This has to be credited to the explosion of OpenClaw. Due to its privacy-focused positioning, Venice was prominently recommended in the model provider section of OpenClaw's official documentation.

Although this prominent recommendation was later removed, 2026 has been a year of rapid growth for Venice. According to data disclosed by Erik Voorhees, by March this year, Venice's total user count exceeded 2 million, paid subscription users reached 55,000, monthly revenue hit $835,000, with a monthly growth rate of 15%.

Corresponding to this is the continuous rise of $VVV. Since entering 2026, $VVV has increased by over 9 times.

$VVV/$DIEM

Earlier, we covered Venice's growth in exposure and user numbers this year, which are the macro-narrative reasons for its rise. But as a crypto AI project with a token, its price increase is also closely tied to the token's mechanisms.

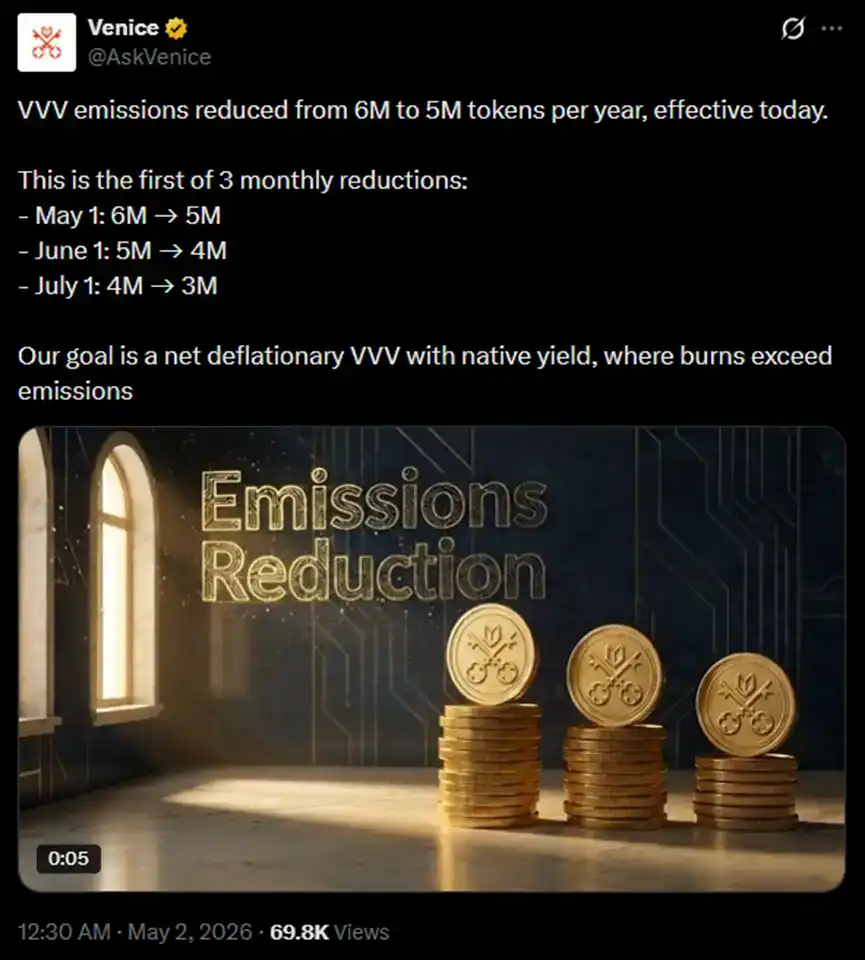

This year, the annual emission of $VVV has undergone multiple reductions and adjustments, dropping from 8 million tokens per year to 5 million. By July 1st, the annual emission will be further reduced to 3 million tokens. The official stated goal is to achieve net deflation for $VVV, ensuring the burn rate exceeds the emission rate to guarantee $VVV's native yield.

$VVV's initial total supply was 100 million tokens. The current total token supply is approximately 79.9 million, with 42.22% (about 33.73 million) of the current supply already burned.

The burn of $VVV is linked to Venice's subscription revenue. At the end of April, Venice allocated more subscription revenue towards token buybacks. For each new Pro plan subscription ($18), $2 will be allocated to buy back and burn $VVV. The Pro+ plan ($68) and Max plan ($200) correspond to $5 and $10 for buyback and burn, respectively.

The current circulating token count is approximately 46 million tokens. Additionally, about 8.85 million tokens remain locked, and around 32.47 million tokens are staked.

The token utility of $VVV is quite interesting. Compared to the awkward situation faced by past crypto projects where "token rights are useless compared to equity," $VVV offers a very compelling solution.

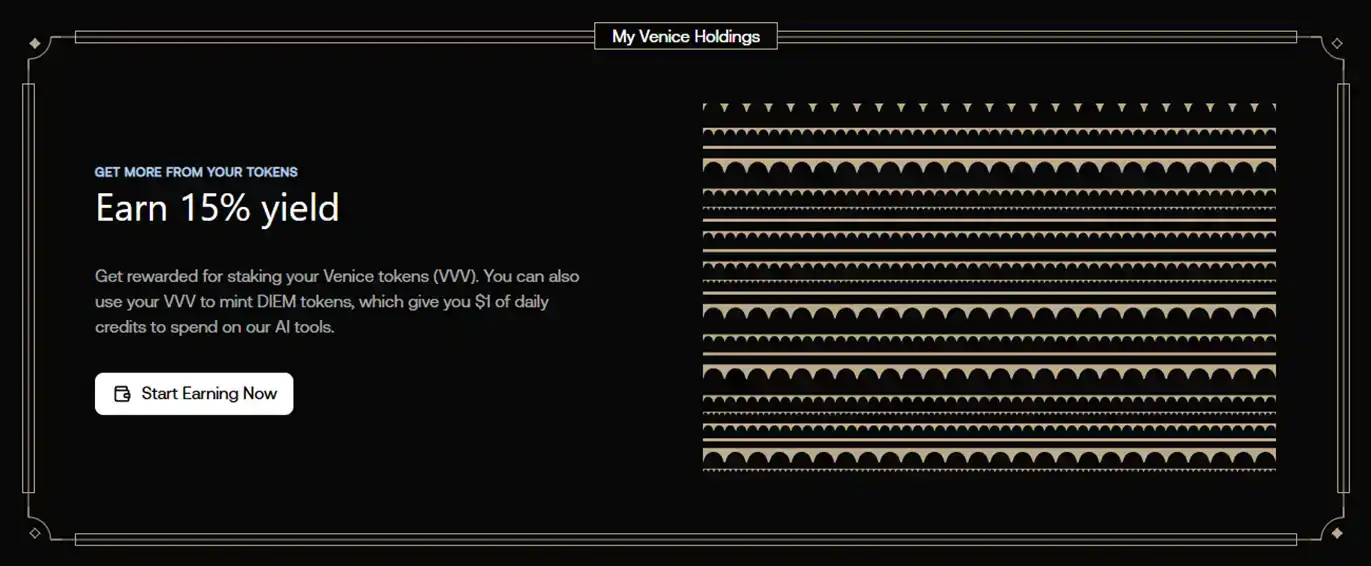

On the foundation of continuously controlling token supply, staking $VVV not only earns more $VVV (receiving more rewards from emission cuts) but also grants the right to mint $DIEM using the staked token $sVVV.

$DIEM can either be traded or staked. Staking 1 $DIEM corresponds to $1 worth of Venice API credit per day.

This credit refreshes daily; what's used today is replenished tomorrow, and it's permanent. What can you do with $1 of Venice API credit? Quite a lot, according to Venice itself:

Stake 1 $DIEM, and get free daily processing of the above with Venice.

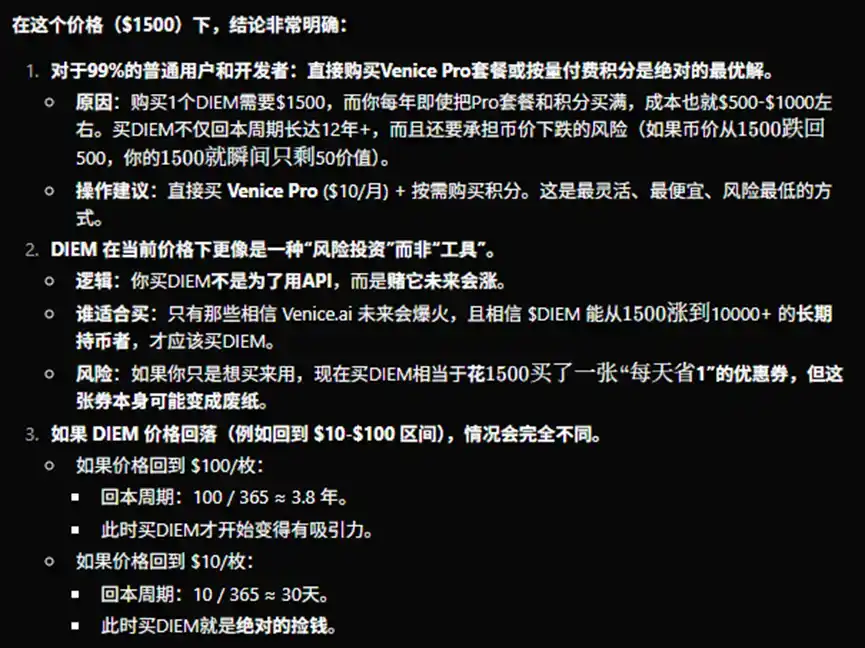

However, one must consider that the current price of one $DIEM has skyrocketed to around $1,500. To mint one $DIEM requires approximately 756 $sVVV, costing about $12,800. Is it worth it? Venice's own calculation looks like this:

Overall, the $VVV/$DIEM economic structure, combined with Venice's regulatory mechanisms, gives $VVV a genuine "tech stock" flavor while retaining unique crypto characteristics:

- Supply-side emission reduction prevents excessive dilution of token value (and also protects the $VVV dividends for stakers from dilution).

- Subscription revenue is used for token buybacks.

- Staked $VVV can be used to mint $DIEM, allowing the token to serve a practical function within the product through $DIEM.

- However, this practical utility comes at a cost; $VVV used to mint $DIEM only receives 80% of the dividends ($VVV staking rewards).

- Enables on-chain DeFi operations, such as staking $VVV to obtain $DIEM, then selling $DIEM to buy more $VVV. There are even community projects like @cheaptokensAI that allow users to profit without selling $DIEM, by reselling the daily credit granted by $DIEM.

$POD

Since entering May, $POD has surged over 12 times at its peak, with its market cap rising from about $7.8 million to briefly surpass $100 million.

$POD is the token for Dolphin's distributed AI inference and training network. In simple terms, it involves "mining" with idle GPUs, providing computing power to those needing AI computation services, and earning $POD rewards.

However, the reason for $POD's speculative frenzy isn't the network itself, but another aspect of Dolphin's business—AI models. Venice's current default model, Venice Uncensored 1.2, is jointly developed by Dolphin and Venice and evolved from Dolphin Mistral 24B Venice Edition.

Therefore, although $POD is solely the token for Dolphin's distributed AI network, at this stage, it is being treated as the only investment vehicle for Dolphin and is being heavily speculated upon.

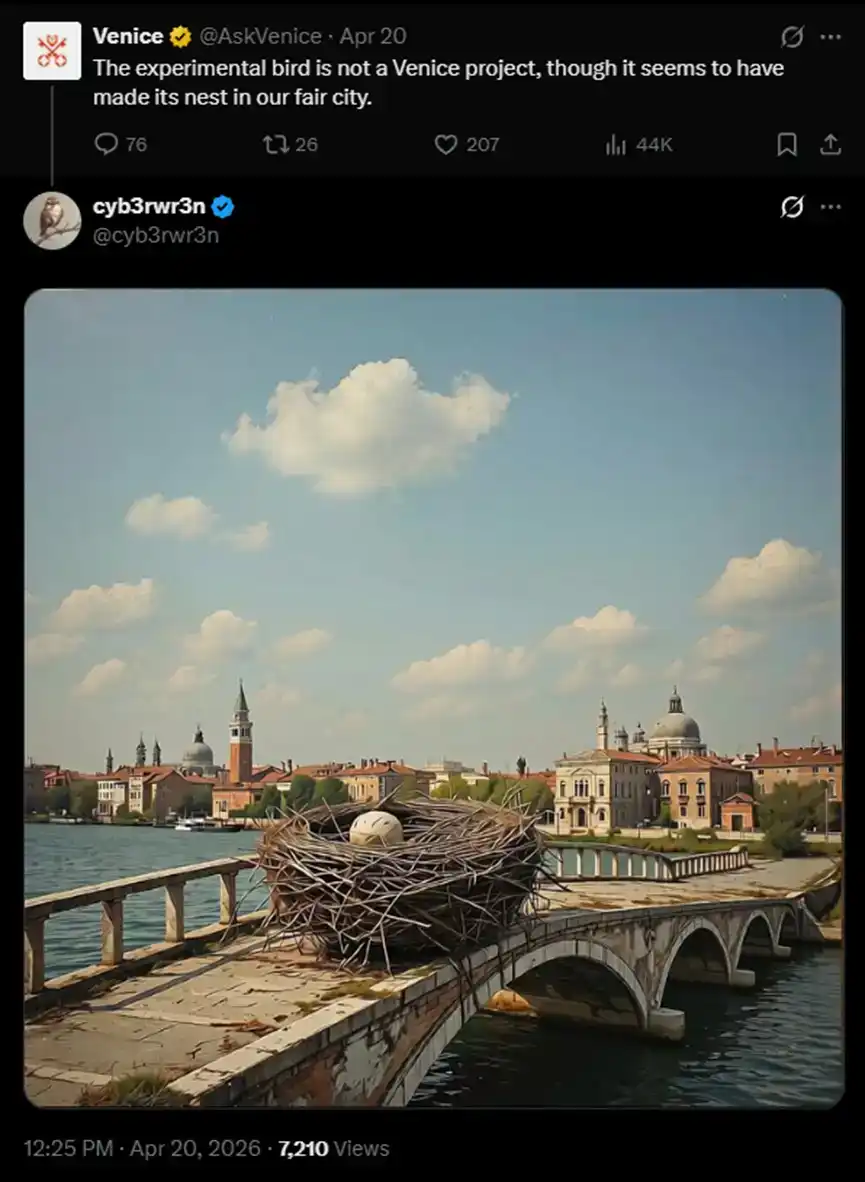

$cyb3rwr3n

This project claims to be building a USDC-based auction market for Venice usage credits. However, it is seen as part of the "VVV" related concepts largely because some players, after analyzing correlations between on-chain behavior and tweets, believe this project is highly associated with Venice founder Erik Voorhees.

The Venice official Twitter account has clarified these speculations, stating that cyb3rwr3n is not an official Venice project.

When this news broke last month, it caused about a 50% price drop, but a few days ago, the token hit a new all-time high. The official clarification hasn't completely erased market associations. According to some community discussions, Erik Voorhees was the first follower of the cyb3rwr3n official Twitter account, and Venice team members like co-founder @TeanaTaylor, CTO @jesseproudman, and product lead @willyogo also follow the account. They argue that even if Venice has no formal link, the supportive sentiment conveyed by such interactions is still a significant bullish signal.

This is also currently one of the cheaper tokens among "VVV" related concepts, with only a $4 million market cap. But being cheap comes with reasons—its product hasn't launched yet, and it currently functions more like a meme coin.

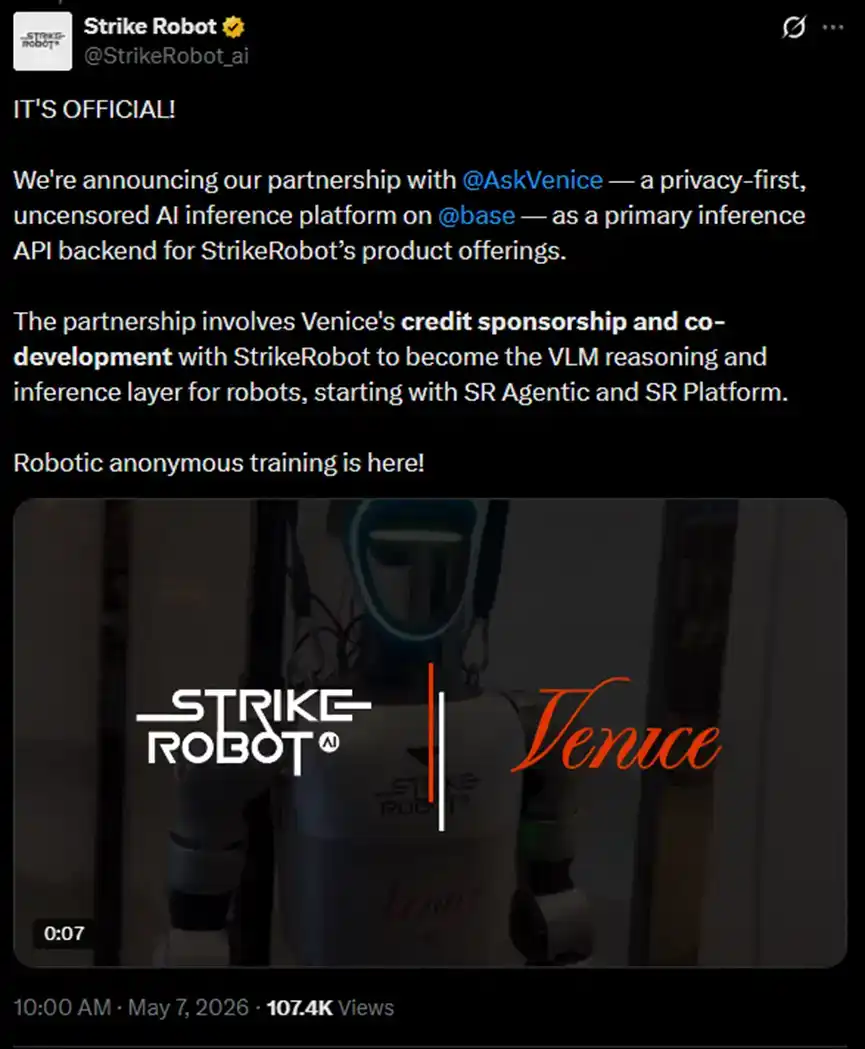

$SR

STRIKEROBOT.AI is a full-stack embodied intelligence platform building a humanoid robot framework for physical AI Business Process Outsourcing (BPO), focusing on safety in hazardous environments (nuclear plants, high-voltage facilities, radiation zones, etc.).

They have a robot training and simulation platform called SR Platform, and $SR is the token for this platform. The project's connection to Venice is the announcement on May 7th about jointly developing a VLM inference layer for robots with Venice and receiving funding sponsorship from Venice.

Since entering May, $SR has risen approximately 4 times, with a current market cap of around $9 million.