Editor's Note: While the U.S. stock market continues to hit record highs, consumer confidence has plunged to low levels. These two seemingly contradictory data sets are presenting a classic structural divide in the U.S. economy.

This article does not attempt to explain whether the stock market is detached from fundamentals, but rather explores what the narrative of 'the U.S. consumer remains strong' is actually built upon, at a time when asset price appreciation and a sense of decline for ordinary households are happening simultaneously. The author points out that consumer confidence surveys themselves may have sampling bias, but the more critical issue is that the U.S. economy is becoming increasingly 'K-shaped': those who hold stocks, real estate, and financial assets continue to benefit from rising asset prices; those without investment assets are being left further behind under the pressure of inflation, and rising food and energy costs.

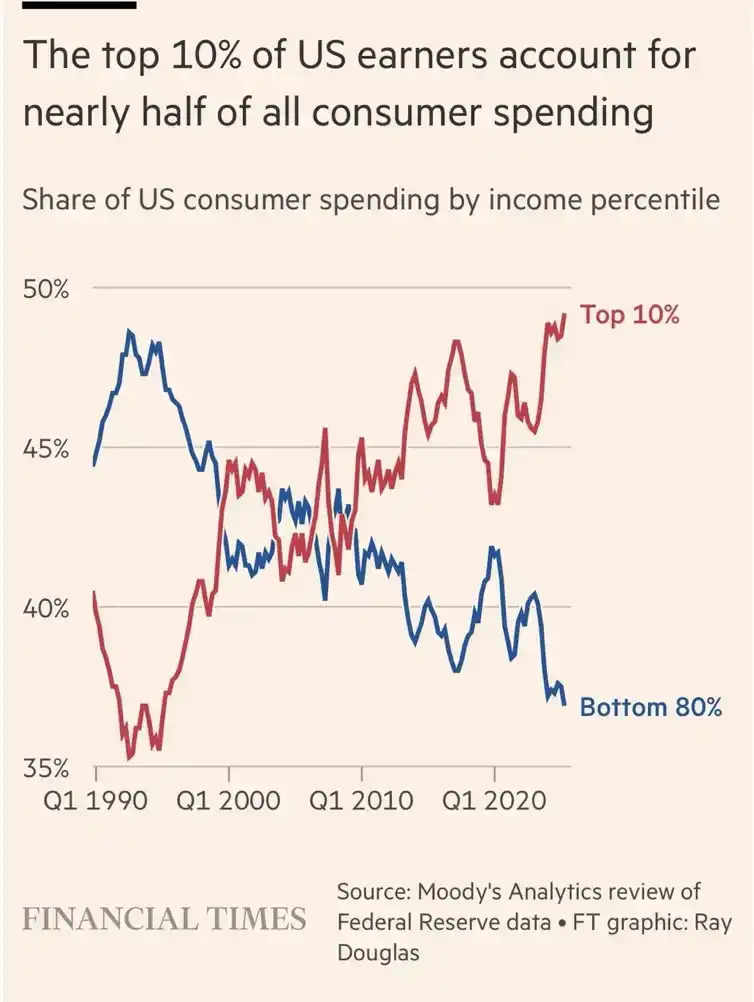

This also explains why aggregate consumption data still appears robust. The top 10% of U.S. consumers now contribute to nearly half of all consumer spending. The continued spending of asset holders, high-income earners, and affluent retirees masks the reality that most households are weakening. In other words, the U.S. economy is not without resilience, but this resilience is increasingly concentrated among a minority.

For investors, low consumer confidence might be a contrarian indicator; but for ordinary people without assets, a rising stock market does not necessarily mean an improved life. The real issue is that the same mechanisms driving asset prices higher may also continue to increase pressure on the asset-less group. This is the sharpest contradiction in the current U.S. economy: the more prosperous the market, the more pronounced the division may become.

The following is the original text:

To the Investors:

One of the most perplexing charts in financial markets is perhaps the one that overlays consumer confidence with the performance of the U.S. stock market. Over the past period, U.S. stocks have been hitting new all-time highs almost daily, yet consumer confidence has been consistently sliding, falling to some of the lowest levels on record.

How can both these things be true at the same time?

First, the quality of the University of Michigan Consumer Sentiment Survey has declined noticeably. Historically, respondents to the survey were roughly 50% Republican and 50% Democrat, but over the last three years this has changed. As the survey methodology has shifted online, the sample composition has also shifted: today's respondents are approximately two-thirds Democrat and one-third Republican.

Given that Democrats currently hold a significantly more pessimistic view of the economy, this over-sampling of one political bloc amplifies negative sentiment in the survey results more than it used to.

That said, I do personally believe a significant portion of Americans hold negative views about the economy and their own financial situations. They are bearing the brunt of currency debasement and the pressures of high inflation from the past few years. Grocery and gasoline bills keep adding up, while wage increases haven't kept pace with rising prices.

Second, people who own stocks feel good about the market rising; but people with no investment assets just feel left further behind as stock prices climb. Thankfully, about 60% of Americans own stocks directly or indirectly, so a decent chunk of the population does benefit from appreciating assets.

But 40% of Americans are not benefiting. These are typically people who do not appear on national television shows, do not post their views on X or Substack, and may not necessarily articulate the financial pain they are experiencing in the language familiar to economists or investors.

This is why the gap between stock market performance and consumer confidence is widening.

One could argue that consumers are saying one thing but their spending behavior shows another. There is some truth to this, as U.S. consumer spending is indeed still growing. But the detail is this: today, the top 10% of U.S. consumers now account for 50% of the nation's consumer spending.

As my friend SightBringer wrote:

"The U.S. consumption economy is increasingly a demand engine driven by luxury goods and high-income earners, wrapped in a fragile mass-market shell. The cruelty of that chart is that it shows the consumption base being hollowed out. The top 10% now support nearly half of all consumer spending, while the share of the bottom 80% is declining.

This means that, looking at aggregate data, the U.S. consumer appears to be holding strong, but most households are actually weakening. Overall consumption is holding up because asset holders, high-income earners, and affluent retirees are still spending."

If you dig into the data, you'll see a 'K-shaped economy' emerging more and more clearly in consumer spending. This makes the situation complex and confusing, but it makes sense when linked to the slump in consumer confidence.

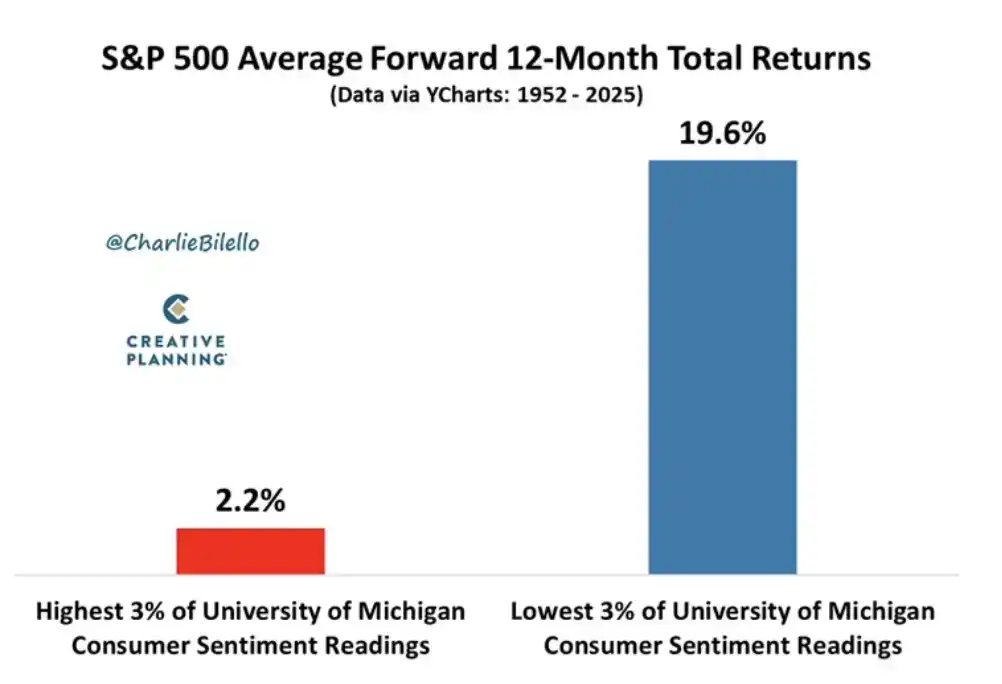

However, I also bring some good news for investors. Peter Mallouk, CEO of Creative Planning, points out that extremely low consumer sentiment readings tend to be a "very good contrary indicator." He says: "The worse people feel about the future, the better the stock market tends to perform afterwards."

When the University of Michigan Consumer Sentiment Index has fallen into the lowest 3% of all its historical readings, the S&P 500 has delivered an average 12-month return of 19.6%. Given the stark divergence already present between the stock market and consumer confidence, this should offer investors some solace. But the continued strength of the U.S. economy may not truly help the bottom 40% of Americans—they own no investment assets and are still absorbing the impact of higher consumer prices.

This is the most profound binary split of our times.

The rich get richer, while everyone else falls further behind. The very forces driving asset prices higher are also punishing those who most need breathing room. If you want to know what the Federal Reserve, the Treasury, or Washington will ultimately decide, you need only look at which category the people making those decisions belong to.

The wealthy and powerful are navigating the situation with the tools at their disposal. They will try to show empathy. They will look at as much data as possible. I truly believe these people want to do the right thing and help as many people as possible.

The problem is they cannot serve two masters. So, wealthy asset holders will continue to win, and everyone else will continue to sink. All you can do is make sure you're on the right side. Because time is running out, asset prices are still moving higher, and inflation is claiming more victims.

Have a great day. We'll talk again soon.