Author: BitalkNews

On the morning of April 20, 2026, the stock price of New Huo Group suddenly surged, rising more than 11% during the session.

What triggered this market movement was a piece of news that simultaneously ignited the financial and crypto circles: Fu Peng, former chief economist of Northeast Securities, officially joined New Huo Group as chief economist.

The news was first disclosed by Tencent News' "First Line," and New Huo Group subsequently confirmed it. Fu Peng himself also stated to the media: "It is mainly about combining FICC and C businesses."

Among them, FICC refers to fixed income, foreign exchange, and commodities, while C refers to cryptocurrency. His main work after joining will be to incorporate digital assets into the global asset allocation framework, providing macro research and asset allocation support for New Huo's institutional clients.

This is the first time he has reappeared in the public eye with an official position nearly a year after leaving Northeast Securities. For him, this is not just a change of employer but more like a restart of his career narrative.

The first half reached the pinnacle in the traditional financial system but was interrupted by controversy and illness; the second half is chosen in Hong Kong, in the crypto track, at the intersection where traditional finance and digital assets are slowly merging.

The Path of an Atypical Chief

In 2004, Fu Peng joined Lehman Brothers and later served as the head of global macro hedge strategy design at Solomon International Investment Group, responsible for currency, commodity, and major asset linkage analysis, for nearly four years.

He returned to China at the end of 2008 and worked at institutions such as Shandong High-Tech Investment, CIFCO, Galaxy Futures, Galaxy Securities, and Essence Securities.

In February 2020, he joined Northeast Securities as chief economist. His approach in this role differed from most of his peers: he made self-media his main battlefield.

He often used analogies and metaphors to explain economic logic, with a performance-style flair. His Weibo account, "Fu Peng's Financial World," has accumulated over 4 million followers, while his Douyin (TikTok) followers have reached 1.485 million. On Xiaohongshu and Bilibili, he has 355,000 and 773,000 followers, respectively.

In 2024, he published "Witnessing the Countercurrent," using a three-layer framework of "politics/distribution—macro—assets" to explain changes in global asset logic after 2016.

This approach gave him high recognition in the financial circle, making him an analyst who could present complex macro logic in an accessible way to ordinary investors.

The Consequences of a Speech

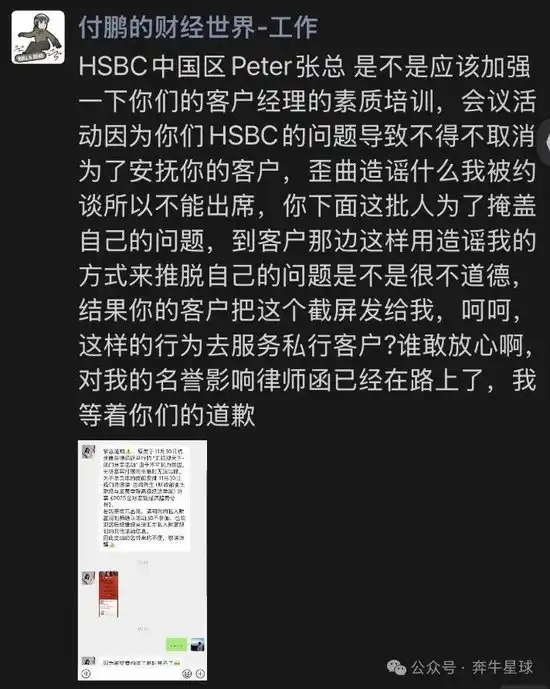

In late November 2024, Fu Peng was invited to give a year-end speech at an internal HSBC Private Wealth Planning event in Shanghai. The content covered China's declining demand, shrinking middle-class income,加剧的消费分化, and his judgment that current stimulus policies could not replicate the effects of the 2008 measures.

The recording and transcript were widely circulated online, removed from multiple platforms, and his WeChat and short video accounts were banned for nearly half a year.

Rumors emerged that he was canceled due to regulatory talks. Fu Peng publicly responded, directly criticizing HSBC, sharing chat records, and stating, "A lawyer's letter is already on the way, waiting for your apology."

Northeast Securities also stated: There has been no recent regulatory discussion. HSBC responded that it was "looking into the relevant situation." After that, the matter quietly faded from public discussion, with no further progress, eventually ending without resolution.

During the account ban, Fu Peng's channels for public expression were significantly reduced.

On April 30, 2025, he officially resigned from Northeast Securities, explaining externally: He had just undergone two major surgeries and needed to rest for more than half a year.

Predictive Ability and Boundaries

Among Fu Peng's fan base, there are many stories about his accurate predictions, covering the 2008 financial crisis, the recovery of the Japanese stock market, and the turning point of China's real estate cycle. Since 2016, he has consistently emphasized de-globalization and changes in interest rate trends, with parts of his framework later validated to some extent.

However, his prediction record is not consistent. There have been clear deviations in short-term exchange rates and specific policy windows, with some judgments criticized as overly pessimistic or significantly inaccurate due to policy interventions. He himself admits that macro research focuses on structural variables, not next quarter's data. This is both a methodological explanation and a preventive clarification for short-term inaccuracies.

What he provides is a framework for interpreting the world, not a stable, reproducible prediction tool. Describing him as a prophet who gets everything right is a misinterpretation.

One of his major advantages is his ability to express complex macro logic in an accessible manner while maintaining relatively independent judgment. This allows his influence to reach a broader audience, and this characteristic is precisely what New Huo Group needs most.

Why Choose New Huo

Theoretically, Fu Peng had more than one option for his comeback. Traditional securities firms would welcome him back, and the role of chief economist is familiar to him, but he chose New Huo.

The space in traditional finance is narrowing. For someone who spoke so bluntly in the HSBC speech, returning to the system would mean something he likely understands better than anyone.

His skill set was never limited to traditional assets; FICC has always been his forte. After institutionalization, the connection between crypto assets and macro logic has become increasingly evident. Interest rate cycles, dollar liquidity, geopolitical risk premiums—these variables affect both traditional and digital assets.

There is also a more practical factor: a comeback requires a suitable stage.

New Huo Group is licensed in Hong Kong, listed on the Hong Kong stock exchange, and operates within a compliance framework. At the same time, its size and stage provide enough flexibility to allow a strong-minded individual to build a new research system. This is a completely different situation from playing a fixed role in a mature large institution.

Why New Huo Needs Him

New Huo Group currently positions itself as a digital asset management institution for high-net-worth clients. It holds Hong Kong SFC Type 1, 4, and 9 licenses and a TCSP trust license, making it one of the较早实现全牌照虚拟资产管理的机构 in Hong Kong.

In 2025, Weng Xiaoqi became CEO, launched the Bitfire Premium service, acquired a majority stake in the Japanese licensed exchange BitTrade, exited the retail market, and focused on family offices, listed companies, and institutional clients. At the end of March 2026, the company was renamed New Huo Group Holdings Limited, with the English name Bitfire Group.

Financially, total revenue for the 2025 fiscal year was HKD 8.661 billion, a year-on-year increase of over 450%, but growth was mainly driven by low-margin crypto OTC trading volume. The company整体依然亏损. Management has designated 2026 as the year for profitability, with significant pressure.

The compliance framework is in place, and growth numbers are impressive, but what New Huo truly lacks at this stage is not流量, but trust.

The clients it serves—family office partners, financial executives of listed companies, private investors with substantial wealth—do not lack information or data. What they lack is a narrative framework that can make them comfortable with digital assets and a professional image from the traditional financial world.

Weng Xiaoqi stated this logic quite bluntly: "Fu Peng's profound global macro research capabilities and precise market liquidity insights will become the company's top strategic brain... helping clients accurately grasp certainty in the era of 'FICC+C.'"

Fu Peng's background in international investment banking and hedge funds, his independent public persona, and his million-level influence constitute a recognizable professional signal for traditional wealthy individuals evaluating whether to allocate more funds to digital assets.

This is a transaction where both sides get what they need.

A Beginning Without a Conclusion

On one side is a person who emerged from the traditional financial system, experienced highs, controversies, and a forced interruption, now seeking a space to continue expressing and contributing. On the other side is a company striving to transition from a trading platform to an institutional service provider, attempting to establish a language more easily understood by traditional capital.

Can the appeal of macro narratives translate into real institutional capital inflows? How long can Fu Peng's independent style last within the framework of a listed company?

Will the trust of traditional wealthy clients in digital assets ultimately be built on framework认同, or will it still require further regulatory developments? These questions will take time to answer.