Written by: Castle Labs, OAK Research, Hazeflow

Compiled by: AididiaoJP, Foresight News

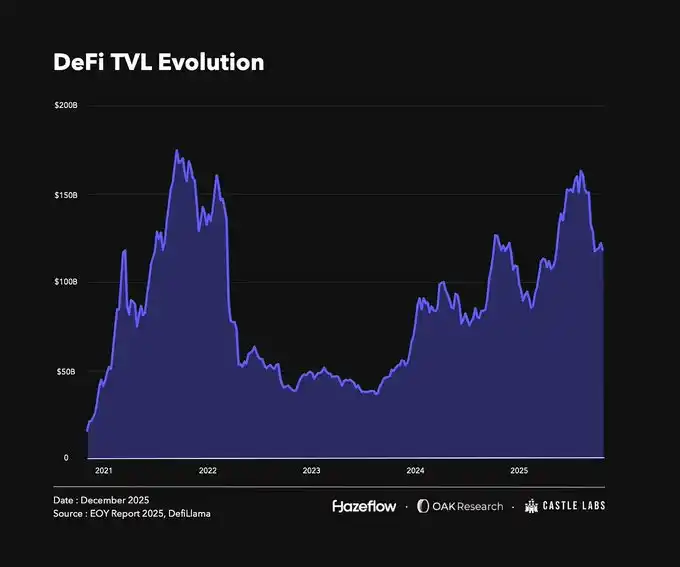

Looking back, DeFi has gone through various stages of glory, troughs, and turmoil. It has now firmly established itself, with key metrics showing a continuous growth trend of "higher highs and higher lows." It is important to note that many changes in TVL (Total Value Locked) are closely related to asset prices, as the assets locked in DeFi are mostly volatile coins, and their price movements directly affect key data.

As of the time of writing, the TVL level is still higher than at the beginning of the year. Although the difference is not significant, a peak was reached in October this year when the prices of major crypto assets hit new all-time highs. The subsequent "October Liquidation Event" led to $19 billion in asset liquidations, causing some protocols to implode and resulting in a drop of about 28% in total TVL, with related token prices also falling.

However, this part of the report is not just about implosions and cascading liquidations; it aims to provide a comprehensive review of the overall development, growth, and transformation of the DeFi space this year.

The 2025 DeFi Landscape

This year, several protocols and sectors have stood out in the market, becoming the focus of attention. We cannot list all the success stories but will select a few representative cases for analysis.

Successful Protocols

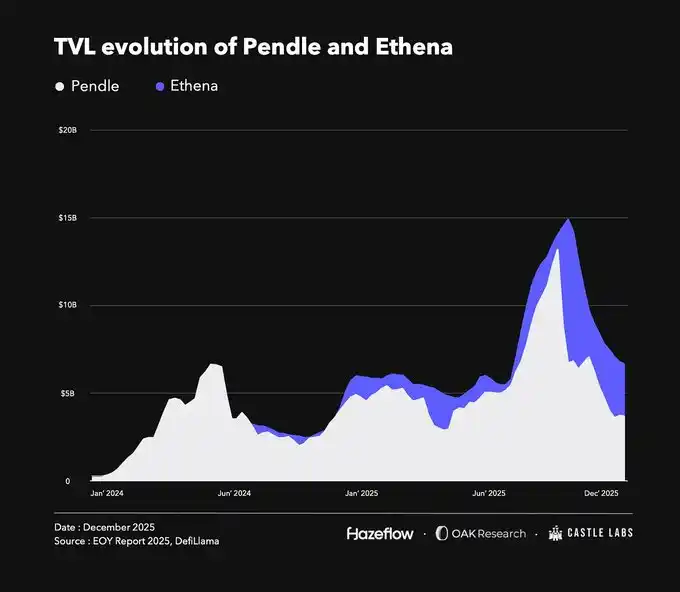

2025 was the "Year of Yield," and in this sector, @pendle_fi was undoubtedly the leader. This protocol splits yield-bearing assets into principal (PT tokens) and yield (YT tokens). The yield portion can be traded independently, while the principal can be redeemed at maturity. This innovative design, coupled with collaborations with protocols like @ethena_labs and @aave, drove its TVL growth.

It should be noted that Pendle's TVL is currently not at its all-time high and is even lower than at the beginning of the year, with the peak occurring around mid-September. This is mainly due to the launch of its Plasma chain, which incentivized users to migrate assets from other platforms, causing a temporary decline in locked value. However, the protocol's fundamentals remain solid, and Pendle has solidified its position as a core yield distribution platform.

Pendle is also expanding its yield services through the Boros protocol. Boros aims to hedge or leverage funding rate risk by going long or short on Yield Units (YU). A YU represents the yield generated by 1 unit of collateral from issuance to maturity. For example, 1 YU-ETH equals the yield generated by 1 ETH of nominal value until maturity, similar in logic to YT tokens on Pendle.

@ethena_labs was another highlight this year. Ethena offers a synthetic dollar stablecoin, USDe, which is a yield-bearing asset that generates returns through basis trading. USDe is backed by volatile assets like BTC, ETH, and LSTs. To maintain delta neutrality, Ethena hedges its spot holdings and simultaneously opens perpetual short positions as margin. Although the position is delta-neutral, it earns yield from the funding rates paid by longs to shorts in perpetual contracts.

Similar to Pendle, Ethena also experienced a TVL decline in the second half of the year. The main drop occurred after the October liquidation event, when TVL was at its peak. The reason was a brief depeg of USDe on @binance, which led to the liquidation of positions based on USDe and had a cascading effect on locked value. In reality, USDe itself did not depeg, and its reserve assets remained safe. The depeg on Binance was primarily due to oracle configuration and insufficient liquidity in that trading pair. On other platforms like Aave, where the USDe/USDT price used a hard-coded feed, related positions were unaffected.

Ethena's moat is strong and scalable. Recently, they have focused on a "Stablecoin-as-a-Service" model, issuing customized stablecoins for specific use cases, and have launched native stablecoins in collaboration with @megaeth, @JupiterExchange, @SuiNetwork, and others. This helps capture value that would otherwise flow outside the ecosystem (e.g., to Tether, Circle) back to the protocol and the chain. Tether and Circle earn billions of dollars in annual revenue from their stablecoin businesses, but this revenue does not flow back to the underlying chains and protocols that use their stablecoins.

Additionally, Ethena is expanding the utility of its token, recently launching @hyenatrade, a USDe-margined perpetual合约 DEX built on the Hyperliquid HIP-3 standard. Its unique feature is that traders can use USDe as margin and earn substantial APY, while using other stablecoins as margin does not yield any returns.

By expanding its core business and enriching its application scenarios, Ethena is poised to further increase its market share in the stablecoin market in the coming years.

Among the successful protocols, @HyperliquidX ranked at the top in various metrics this year. After the successful launch of its token, it has become one of the best on-chain venues for trading perpetual contracts. The protocol generated substantial revenue and fees, all of which were used for token buybacks, driving significant growth in its market capitalization. Hyperliquid aims to build comprehensive financial infrastructure and is steadily advancing through the HIP-3 upgrade and the launch of HyperEVM.

Successful Sectors

It can be said that successful protocols often come from outperforming sectors. The two big winning sectors this year were perpetual contracts and stablecoins, both of which have found solid product-market fit with sustained strong demand.

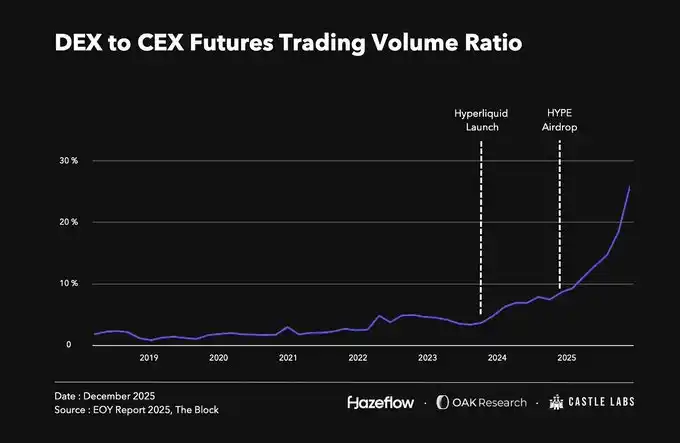

Perpetual trading has long been a major component of the crypto market, with daily trading volumes in the tens of billions of dollars. But before this year, the vast majority of this volume occurred on centralized exchanges. This landscape began to change with Hyperliquid's large airdrop at the end of 2024, reigniting interest in on-chain perpetual contracts and intensifying competition. To date, the proportion of DEX perpetual trading volume relative to CEX has reached a record high of about 18%. Currently, protocols like @Lighter_xyz, @Aster_DEX, @extendedapp, @pacifica_fi, and many others are entering this sector, competing for a share of the growing on-chain perpetual trading pie.

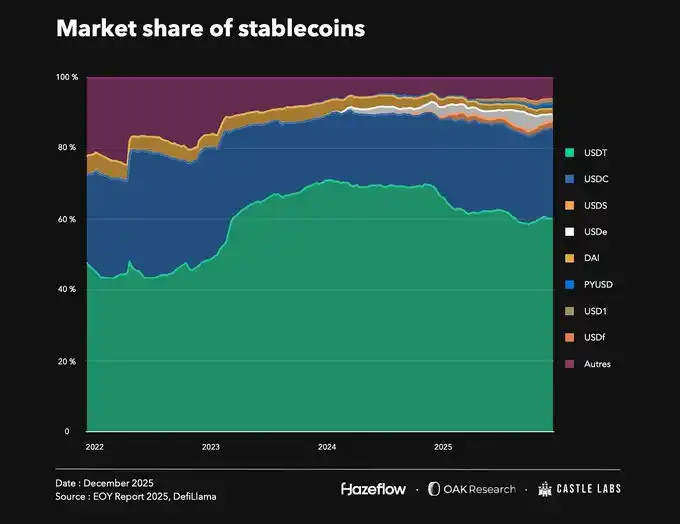

Another successful sector is stablecoins, whose total market capitalization has continued to climb. The current stablecoin market cap is approximately $309 billion, an increase of over 50% compared to the $200 billion at the start of the year. For years, the demand for stablecoins has only grown, and the presence of over 300 issuers indicates increasingly fierce competition.

Despite the numerous issuers, the market is still dominated by @Tether_to (USDT) and @circle (USDC), which together hold an 85% market share, followed by protocols like Ethena (USDe) and @SkyEcosystem (USDS). With first-mover advantages and deep on-chain integrations, Tether and Circle maintain their dominance despite the constant influx of new players.

This dominance also leads to a problem: a significant amount of value flows from native ecosystems to external entities. In the past 30 days, Tether and Circle, due to their widespread use across various chains and protocols, generated approximately $700 million and $240 million in revenue, respectively. To address this value leakage, Ethena introduced the "Stablecoin-as-a-Service" model to help blockchains retain the value created within their ecosystems. However, challenging Tether and Circle remains very difficult, as they are deeply embedded in the infrastructure of the entire crypto ecosystem.

The October Liquidation Event

The October Liquidation Event (also known as the "Crypto Stress Test") occurred on October 10th, leading to the liquidation of over $19 billion in assets. The immediate trigger was Trump's announcement of imposing 100% tariffs on China in response to China's restrictions on rare earth exports and expanded export controls. A few weeks later, an internal JPMorgan memo leaked, suggesting that Strategy might be removed from the MSCI index, further exacerbating market panic.

This caused all asset prices to fall. BTC and ETH fell 23% and 33% from their highs, respectively. The total crypto market capitalization shrank from around $4.24 trillion on October 10th to $3.16 trillion at the time of writing, a drop of 25%.

On platforms like Binance, Ethena's yield-bearing stablecoin USDe depegged due to the use of the exchange's spot price (which had poor liquidity), leading to unfair liquidations of user positions. The exchange ultimately compensated affected users over $280 million, involving assets like BNSOL and WBETH.

DeFi lending protocols performed robustly during this event, executing liquidations as expected with minimal bad debt. Protocols like @Aave, @Morpho, @0xFluid, @eulerfinance collectively liquidated over $260 million in assets with very low bad debt rates.

While blue-chip DeFi and CeFi withstood the test, many other protocols and leveraged strategies on lending and perpetual platforms (especially recursive lending) suffered heavy losses.

In lending protocols, recursive lending strategies allow users to obtain leverage. This strategy has gained attention recently with the popularity of yield-bearing assets, as it can be profitable when the asset yield exceeds the borrowing rate. However, during periods of high market volatility, even slight depegging can put immense pressure on leveraged positions. When prices plummeted on October 10th, many users were unable to close their positions in time and were ultimately liquidated.

Although leverage caused many losses, cases like Stream Finance were particularly prominent, serving as a warning that blindly chasing excessively high yields is not wise. We will analyze this in detail in the next section.

Are Stablecoins Really Stable? The Stream Finance Incident

In the fourth quarter of this year, several stablecoins with flawed mechanisms collapsed. They might have lasted longer, but the October liquidation event liquidated some over-leveraged stable assets. The largest and most impactful among them were xUSD (Stream Finance) and deUSD (Elixir), which were interconnected and ultimately collapsed together.

Taking Stream Finance as an example, they were essentially selling an over-leveraged, under-collateralized "stablecoin" called xUSD. When users deposited collateral, the protocol would mint xUSD, convert the user's deposit into Elixir's high-yield stablecoin deUSD, and then deposit it into lending protocols like Euler and Morpho.

Through collateralized loans, they were not simply recursing but minting more xUSD, inflating its supply to over 7 times the actual collateral, with only $1.9 million in verifiable USDC collateral supporting $14.5 million in xUSD.

Additionally, the protocol had some off-chain risk exposures unknown to users. During the liquidation event on October 10th, its major off-chain positions were also liquidated, causing the protocol to collapse with losses of $93 million, after which they disabled withdrawals. The withdrawal halt triggered panic among xUSD holders, who sold the asset on illiquid secondary markets, causing the token to depeg rapidly. Subsequently, Elixir's deUSD also depegged quickly, but the protocol managed to process redemptions for most users.

All vaults and managers exposed to these stablecoins in lending protocols like Euler and Morpho suffered losses. Even some protocols generated bad debt because they used fixed-price oracles that hardcoded the price of these assets at $1 even when they had actually depegged. There is no perfect solution for pricing such assets; protocols could use proof-of-reserve oracles, but the collateral for stablecoins like xUSD is often over-leveraged or opaque. Ultimately, users participating in such high-APY trades must understand that this is a high-risk investment and must conduct careful research.

Back to Basics: Revenue is King

Revenue is the foundation of any business. If a protocol can make money and has a good mechanism to return value to token holders, everyone benefits. Of course, reality is often more complex, and token holders often end up on the losing side. Before discussing value accrual, let's look at the main sources of revenue in the crypto industry.

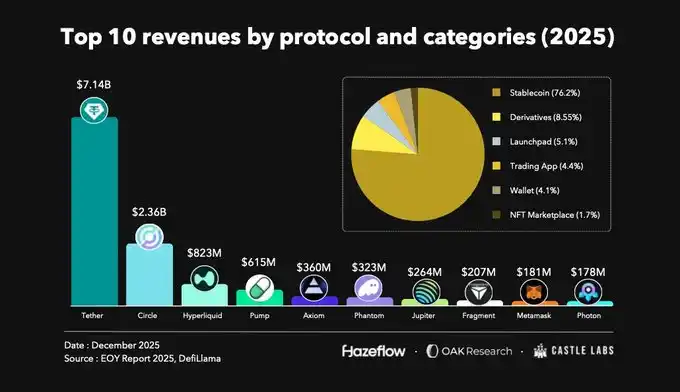

Looking at the top 10 revenue-generating protocols over the past year, stablecoin issuers contributed about 76% of the revenue, followed by derivatives, launchpads, trading applications, etc.

Stablecoins have consistently been the most profitable business in crypto because they are widely used, form the backbone of DeFi, and are the main channel for funds entering and exiting the ecosystem. Secondly, derivatives and launchpads also contributed a significant share of revenue.

Over the past year, Tether and Circle combined generated $9.8 billion in revenue and continue to maintain a similar scale. Following them are Hyperliquid and Jupiter in the derivatives sector, with combined revenue of approximately $1.1 billion.

Beyond these mature sectors, protocols like Pumpdotfun also have sustainable revenue streams. It is worth noting that some of the listed protocols launched just last year, making them relatively new, reflecting the market's willingness to try emerging alternatives. At the same time, incentives are crucial for a protocol's initial performance and user attraction, and unique features may lead to user retention.

Before this, one of the largest DeFi protocols, Uniswap, could not directly link its token to protocol revenue due to regulatory constraints on the token. The proposal burned 100 million UNI tokens from the treasury, equivalent to the amount that should have been burned if protocol fees had been enabled from the beginning. Simultaneously, it formally enabled protocol fees and will use these fees to continuously burn UNI tokens, while ceasing to charge fees for its front-end interface, wallet, and API.

This means that the protocol's growth will be more directly tied to the value of the governance token. An increasing number of projects are focusing on this value alignment, attempting to direct more value to token holders.

Buybacks Become a Mainstream Strategy

In the past, the performance of crypto tokens largely depended on marketing efforts, and users typically paid little attention to the protocol's economic model. This might have benefited short-term speculators, but it was unsustainable in the long run, and many token holders ultimately couldn't exit. Today, the protocol's economic model and actual revenue have become the core measures of value, no longer relying solely on market hype.

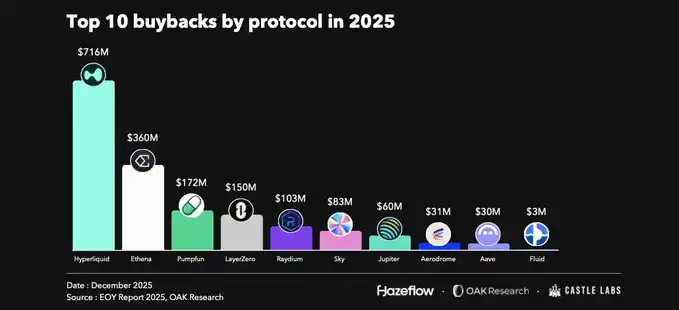

A significant driver of this change was the launch of the HYPE token and its value accrual mechanism. The protocol injects 99% of its revenue into a support fund used to buy back HYPE tokens on the market, reigniting interest in the perpetual contracts sector—Hyperliquid set an extremely high standard for this. These buybacks provided strong price support for the HYPE token, promoting its value growth.

Not only Hyperliquid but also blue-chip DeFi protocols like Aave, Maple, and Fluid have launched buyback programs. Buybacks are a good way to share revenue with token holders, but they require the protocol to have a sustainable revenue source. Therefore, buybacks are more suitable for mature protocols; for new protocols, the early focus should be on growth itself.

Since launching its buyback program in April, Aave has cumulatively used approximately $33 million for buybacks.

Similarly, Fluid has completed about $3 million in buybacks since October, directly returning its revenue to token holders.