Original | Odaily Planet Daily (@OdailyChina)

Author | Ethan(@ethanzhang_web3)

RWA Sector Market Performance

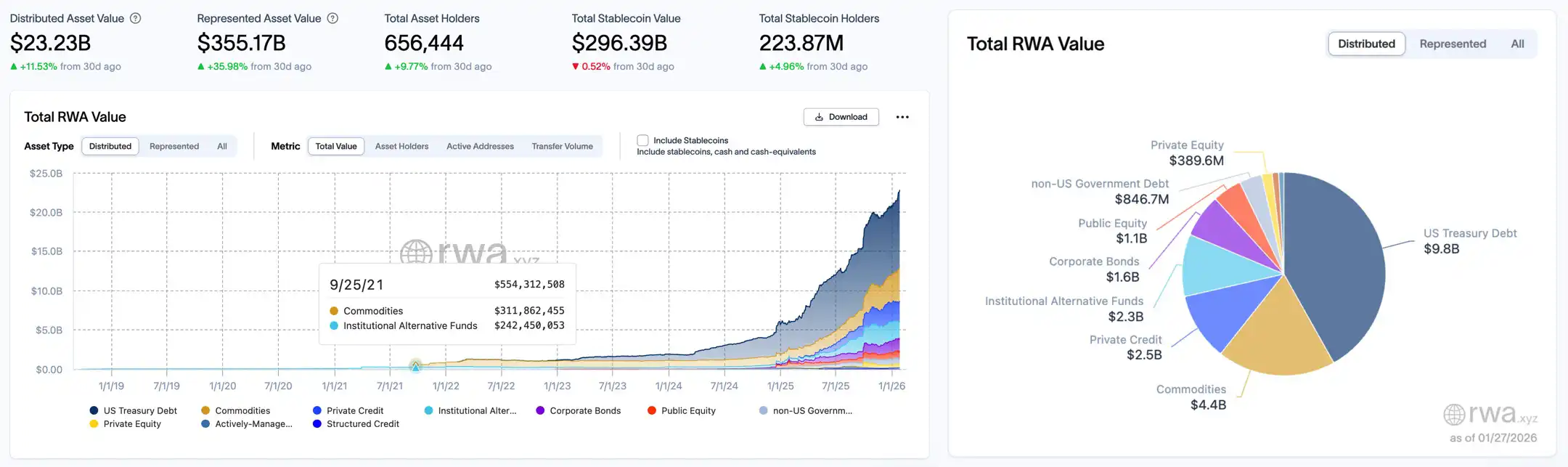

According to the rwa.xyz data panel, as of January 27, 2026, the total on-chain value of RWA (Distributed Asset Value) continued to rise steadily, growing from $216.6 billion on January 20 to $232.3 billion, a weekly increase of $7.6 billion, a growth rate of 3.51%. The size of the broad RWA market also saw a significant rebound, rising from $3.5008 trillion to $3.5508 trillion, an increase of $5 billion, a growth rate of 1.43%. The total number of asset holders increased from 637,807 to 656,444, a net increase of 18,637 people in a single week, an increase of 2.92%. Meanwhile, the stablecoin market maintained relatively stable growth, with the number of holders increasing from 223.34 million to 223.87 million, an increase of 0.23%; the stablecoin market capitalization rose slightly from $2.9964 trillion to $2.99964 trillion, an increase of 0.1%.

In terms of asset structure, the dominant US Treasury on-chain total value remained unchanged at $9.1 billion. Commodity assets continued to perform strongly, growing from $4 billion to $4.2 billion, an increase of 5%. The non-US government debt sector also continued to grow, rising from $8.319 billion to $8.491 billion, an increase of 2.07%. Public equity performance remained strong, increasing from $8.631 billion to $8.754 billion, an increase of 1.43%. Private equity increased slightly from $425.5 million to $429.3 million, maintaining growth. The private credit sector also remained stable, rising slightly from $2.5 billion to $2.55 billion. Institutional alternative funds saw a decline, decreasing from $2.3 billion to $2.2 billion.

Trend Analysis (Compared to Last Week)

This week, the RWA market continued to show a healthy expansion trend, with a stable growth rate in the total value of on-chain assets and a relatively balanced allocation trend in the market structure. Capital flows gradually tilted towards medium-to-high-risk asset classes, especially in commodities, non-US government debt, and equity assets, showing the market's preference for medium-risk assets. The slight increase in private credit and private equity indicates that investors continue to pay attention to the stability of such assets. The steady growth in stablecoin market capitalization and user base has also laid the foundation for subsequent capital flows, further promoting the market's reservoir effect, which is basically consistent with last week's situation.

Market Keywords: Market Expansion, Capital Risk Appetite, Capital Diversion

Key Event Review

Tokenized Gold and Tokenized Silver Sectors Both Reach New Highs in Market Capitalization

According to Coingecko data, as gold prices continue to rise, the total market capitalization of the tokenized gold sector has exceeded $5.27 billion, currently reaching $5,275,490,349, with a 24-hour increase of 1%; the tokenized silver sector market capitalization has exceeded $400 million, currently reaching $439,598,206, with a 24-hour increase of 4.5%, both reaching new highs.

US Enters a Period of Clear Crypto Asset Regulation; Market Structure Bill, If Passed, May Enhance Industry Predictability and Benefit Retail Investors

US crypto asset regulation is further accelerating. The proposed crypto market structure bill, if ultimately passed, will clarify the regulatory authority of federal agencies over digital assets, making cryptocurrencies easier to manage, track, and trade, potentially attracting more investors and increasing token value. It is reported that crypto platforms like Coinbase and Kraken intend to follow a registration system, while stablecoin issuers like Circle and Tether will need to comply with bank-like regulatory requirements to protect retail investors' asset safety. Subsequent procedures include: approval by two Senate committees, a full Senate vote, return to the House for final signing, and finally signature by Trump. Overall, most crypto investors will not be affected in the short term, but in the long run, the bill is expected to provide a safer, more predictable trading environment while making compliance operations of crypto platforms more transparent.

Paul Chan: Hong Kong Expected to Issue Stablecoin Licenses Later This Year

Financial Secretary Paul Chan stated at the World Economic Forum Annual Meeting that Hong Kong is taking a proactive and prudent approach to developing digital assets, promoting market development under the principle of "same activity, same risk, same regulation." Since 2023, Hong Kong has licensed 11 virtual asset trading platforms and is expected to issue stablecoin licenses later this year. Additionally, the SAR government has issued three batches of tokenized green bonds totaling approximately $2.1 billion and launched a regulatory sandbox to encourage application innovation.

South Korea Considering Allowing Domestic Institutions to Issue Virtual Assets; Stablecoins Remain Controversial

Lee Chang-yong, speaking at the Asian Financial Forum in Hong Kong, stated that given market pressure, South Korean authorities have allowed domestic residents to invest in virtual assets issued overseas. Financial regulatory authorities are considering establishing a new registration system to allow domestic institutions to issue virtual assets.

Lee Chang-yong pointed out that if a KRW-denominated stablecoin is launched, its main use might be concentrated in cross-border transactions, while tokenized deposits are more suitable for domestic payment scenarios. However, he emphasized that there is still significant controversy surrounding stablecoins. The core concern is whether KRW stablecoins could be used to evade capital flow management, especially when combined with USD stablecoins.

He further stated that USD stablecoins have a wide range of applications and low access barriers, with related transaction costs significantly lower than using USD directly. When exchange rate fluctuations cause changes in market expectations, funds may quickly flow into USD stablecoins, causing large-scale capital transfers; at the same time, the participation of many non-bank institutions in stablecoin issuance significantly increases regulatory difficulty.

Furthermore, Lee Chang-yong pointed out that South Korea itself has a highly developed fast payment system, so retail CBDC offers limited advantages. Currently, the central bank is advancing tokenized deposits and wholesale CBDC through multiple pilot programs to maintain the existing two-tier financial system.

Thailand SEC Releases Three-Year Strategic Plan, Will Launch Crypto ETF Regulatory Framework

The Thailand Securities and Exchange Commission (SEC) released a three-year strategic plan for 2026-2028, focusing on formulating a crypto ETF regulatory framework and promoting asset tokenization. Thailand SEC Secretary-General Pornanong Budsaratragoon stated that the plan aims to develop digital assets as a formal investment category and improve the competitiveness of the local market.

According to the plan, the Thailand SEC is expected to issue crypto ETF regulatory guidelines early this year and explore issuance in the form of trusts. Meanwhile, the Thailand Futures Exchange (TFEX) is researching the launch of crypto futures trading. In terms of security regulation, the Thailand SEC intercepted 47,692 crypto money mule accounts used for fraud in 2025 and handled over 12,000 investor inquiries. Currently, the Thai digital asset market is valued at approximately $3.19 billion, with a daily trading volume of $95 million. Additionally, the Thai government has approved an exemption from capital gains tax on crypto traded through authorized service providers during the period 2025 to 2029.

American Bankers Association Plans to Lobby to Block Interest-Bearing Stablecoins

The American Bankers Association has listed "preventing stablecoins from generating yield" as its top lobbying goal for 2026. The association believes that interest-bearing stablecoins will become an alternative to bank deposits, potentially leading to the outflow of trillions of dollars from the traditional banking system, thereby weakening banks' lending capacity and endangering their core role in the financial system.

In response, Circle CEO Jeremy Allaire refuted this at the Davos Forum, calling the concern that stablecoin yields would affect bank deposits "completely absurd," and pointed out that yields can enhance user stickiness, and stablecoins will become a necessary payment system for AI agents to conduct large-scale transactions in the future. Opponents believe that this move aims to protect bank interests, limits fintech innovation, and puts the US at a disadvantage in competition with China's digital yuan. Opinion: NYSE Tokenization Plan More Like "Concept Packaging," Lacking Key Details

Fortune magazine analyst Omid Malekan published an article stating that the New York Stock Exchange's large-scale tokenization plan is nothing more than an empty promise wrapped in innovation. The 24/7 trading and instant settlement emphasized by the NYSE are not unique to blockchain; existing centralized systems can also achieve this technically. The real阻力 comes from the interest structure of existing intermediary systems and business partners. It also did not disclose which blockchains and stablecoins the plan supports, nor the programming languages, virtual machines, and token standards. Considering that the NYSE's grand plan is "subject to regulatory approval," this lack of detail is puzzling. The core advantage of public chains is not database efficiency, but permissionless global access and a financial architecture similar to bearer assets, which fundamentally conflicts with the market structure of "only qualified brokers allowed" that the NYSE explicitly retains.

US Senators Submit Multiple Amendments to Crypto Market Structure Bill, Including Banning President and Others from Trading Digital Assets

Before next week's hearing, debate, and vote on the crypto market structure bill by the Senate Agriculture Committee, Democratic senators submitted multiple amendments to the bill.

One amendment aims to add the "Digital Asset Ethics Act" to the bill. This amendment would prohibit "covered persons" such as the President, Vice President, and members of Congress from engaging in certain financial transactions involving digital assets. Bloomberg estimated that Trump has profited approximately $1.4 billion from his cryptocurrency investments, including investments from DeFi and stablecoin project World Liberty Financial. The Trump family also holds a 20% stake in mining company American Bitcoin.

Other amendments include aims to prevent "digital asset kiosks" from conducting fake transactions; and requiring the effective date of future cryptocurrency bills to be delayed until at least four Commodity Futures Trading Commission (CFTC) commissioners are appointed. Since the CFTC currently has only one commissioner, and the maximum number of commissioners is five, this issue has been a point of contention among some legislators.

Stablecoins Transferred Over $35 Trillion Last Year, But Only 1% Were Real-World Payments

A new report from consulting firm McKinsey and blockchain data company Artemis Analytics shows that stablecoins transferred over $35 trillion on the blockchain last year, but only about 1% of that was real-world payments. Analysis estimates that only $380 billion of the activity reflected actual payments, such as payments to suppliers, remittances, or payroll. This accounts for about 0.02% of global payment volume, while McKinsey estimates global payment volume exceeds $2000 trillion annually.

Tether Gold Accounts for Over Half of Gold Stablecoin Market Share; Gold Reserves Reached 520,089.350 Ounces in Q4 Last Year

Tether officially announced that Tether Gold accounts for over half of the entire gold stablecoin market share. The company's key metrics for the end of Q4 2025:

Total Physical Gold Reserves: 520,089.350 ounces (fine troy ounces)

Total XAU₮ Tokens in Circulation: 520,089.300000 XAUT

Gold Backing: 1:1, each XAUT token is backed by one fine troy ounce of physical gold.

Total Market Cap: $2,246,458,120

Tokens Sold: 409,217.640000 XAUT

Number of Tokens Available for Sale: 110,871.660000 XAUT

Capital One Plans to Acquire Fintech Company Brex for $5.15 Billion; Brex Previously Planned to Launch Stablecoin Payment Function

Technology-based financial services company Capital One agreed to acquire fintech company Brex for cash + stock (50% each), valuing the transaction at $5.15 billion, and will merge it into its commercial banking and payments business. The transaction is expected to be completed in mid-2026, and Franceschi will continue to be responsible for Brex after its merger into Capital One's commercial banking and payments business.

Brex previously announced plans to launch a native stablecoin instant payment function.

CPIC IMHK Co-Establishes $500 Million RWA Tokenization Fund

China Taiping Insurance Investment Management (Hong Kong) Co., Ltd. (CPIC IMHK) announced the establishment of a real-world asset (RWA) tokenization fund with Hivemind Capital. The initial target for this fund platform is set at $500 million, with the specific amount depending on market conditions, institutional and other non-retail qualified investor demand, and relevant regulatory approvals. The two companies are jointly committed to combining on-chain investment infrastructure with established asset management practices to provide transparent, compliant, and institutionalized tokenized investment products. Blockchain Infrastructure Company Zerohash in Talks to Raise $250 Million at a $1.5 Billion Valuation

Blockchain infrastructure company Zerohash is in talks to raise $250 million at a valuation of $1.5 billion. However, Zerohash has not yet responded to requests for comment on the matter. As discussions are ongoing, the amount may change. Zerohash raised $104 million in a Series D-2 round led by Interactive Brokers last October, valuing the company at $1 billion. The company, founded in 2017, provides APIs and embeddable developer tools that enable financial institutions and fintech companies to deliver cryptocurrencies, stablecoins, and tokenized products.

Davos "Tokenization" Debate: Technological Dividends Expected, Sovereignty and Regulation More Difficult

While AI almost "dominated" the entire World Economic Forum 2026 Annual Meeting, virtual currency, once extremely popular in Davos, returned to the spotlight. Representatives from traditional banks, regulatory agencies, and crypto leaders engaged in a sharp, in-depth debate on whether tokenization is on the eve of an explosion, how digital currencies are reshaping sovereign boundaries, and the foundation of trust in the financial system:

1. Coinbase CEO Brian Armstrong pointed out that tokenization solves the efficiency problem of the financial system, enabling real-time settlement and reducing fees, but its core strength lies in the "democratization of investment access."

2. Euroclear CEO Valérie Urbain sees tokenization as an "evolution of financial markets and securities" that could allow issuers to shorten issuance cycles, reduce issuance costs, and also help the market "reach a wider range of investors," playing a role in "financial inclusion."

3. Banque de France Governor François Villeroy de Galhau believes that increasing investment opportunities must be synchronized with the improvement of financial literacy, otherwise tokenization could turn into a disaster.

4. Standard Chartered Bank Group CEO Bill Winters bluntly stated that while achieving tokenization for the vast majority of transactions by 2028 might be slightly optimistic, the direction that "the vast majority of assets will eventually be settled digitally" is irreversible.

5. Ripple CEO Brad Garlinghouse quoted former Fed Chairman Ben Bernanke, saying that governments will not give up control of the money supply. Ripple's current strategy leans more towards building bridges between traditional finance and decentralized finance rather than challenging sovereignty itself.

"1011 Insider Whale" Agent: US Stock Tokenization May Become the Only Realistic Path for US Debt Resolution and Benefit ETH and RWA

"1011 Insider Whale" agent Garrett Jin posted on platform X, stating that against the backdrop of de-dollarization, extending the debt cycle to help the US solve its debt problem seems unrealistic. Tokenizing US stocks to drive stablecoin demand is the main feasible path for the US to refinance its growing debt. BlackRock's push for RWA illustrates this, against the backdrop of accumulating US debt. Since 2025, rumors of the so-called "Mar-a-Lago Agreement" have circulated, but the agreement was never formally signed or implemented. Its core idea was to alleviate the $36 trillion US federal debt burden. The reality is that US debt continues to rise, and de-dollarization has not slowed. Countries like Sweden, Denmark, and India are reducing their holdings of US Treasury bonds. If the US wants to repay old debt with new debt, the only realistic path is to issue more stablecoins, bringing new global capital into US Treasury bonds. To achieve large-scale operations, the solution is RWA, i.e., putting US stocks on-chain. Tokenizing $68 trillion worth of US stocks would significantly increase stablecoin demand, indirectly absorbing debt pressure. This is why BlackRock, closely linked to the US power center, is actively promoting RWA and on-chain stock trading. In this context, ETH will become the settlement layer for the global capital market due to practical needs. 2026 will be the "Year of RWA".

CZ: Bullish on Tokenization, Payments, and AI in the Future Directions

CZ spoke at the World Economic Forum in Davos at the "New Era of Finance" panel discussion, stating, "The overall scale of trading platforms is also higher than last year. The crypto industry already has two mature industries: trading platforms and stablecoins. I am optimistic about three new directions in the future:

First, tokenization is a very important direction. By tokenizing some assets, governments can actually solve financial problems more efficiently, improve the operational efficiency of the financial system, and thereby promote the development of related industries and trading markets.

Second is payments. We have also tried crypto payments in the past, but frankly, not many people actually used them. But now a trend is emerging: traditional payment methods are integrating with crypto technology. For example, users use Visa, Mastercard and other cards to complete payments, funds are deducted from the account, merchants receive fiat currency, and stablecoins and blockchain are used for settlement and bridging in the background. This model is gradually being implemented and will definitely develop in the future.

The third direction is artificial intelligence (AI). He believes that the "native currency" of AI Agents should naturally be cryptocurrency, and blockchain is currently the most suitable native technology interface for AI Agents to use. Today's AI is not yet a true Agent; they cannot buy you plane tickets, book restaurants, or directly complete payments; but once AI truly has the ability to act and transact, cryptocurrency will become its most natural, most native payment and settlement method.

Hot Project Dynamics

Ondo Finance (ONDO)

One-Sentence Introduction:

Ondo Finance is a decentralized finance protocol focused on structured financial products and the tokenization of real-world assets. Its goal is to provide users with fixed-income products, such as tokenized US Treasury bonds or other financial instruments, through blockchain technology. Ondo Finance allows users to invest in low-risk, high-liquidity assets while maintaining decentralized transparency and security. Its token ONDO is used for protocol governance and incentive mechanisms. The platform also supports cross-chain operations to expand its application scope in the DeFi ecosystem.

Latest Developments:

On January 21, Ondo Finance announced that over 200 tokenized US stocks and ETFs are now live on the Solana mainnet, bringing a complete traditional finance (TradFi) investment portfolio into the crypto space. Over 200 assets are available for Solana users to trade, including: stocks across various sectors, ETFs, market indices and sector funds, gold, silver, oil and strategic metals, treasury and corporate bonds, leveraged and inverse ETFs, etc.

On January 24, according to official data, Ondo Finance's Total Value Locked (TVL) has exceeded $2.5 billion, making it a leading global tokenized US Treasury and stock platform. Ondo's TVL in the tokenized US Treasury sector is approximately $2 billion; the USDY product has exceeded $1 billion TVL, supporting global investors across 9 chains; the flagship institutional fund OUSG TVL exceeds $770 million, covering funds from top asset management companies like Fidelity, BlackRock, and Franklin Templeton; tokenized stock TVL exceeds $500 million, accounting for about 50% of the market share. Since its launch in September 2025, cumulative trading volume has exceeded $7 billion, covering 200+ stocks.

MSX(STONKS)

One-Sentence Introduction:

MSX is a community-driven DeFi platform focused on tokenizing US stocks and other RWAs for on-chain trading. Through a partnership with Fidelity, the platform achieves 1:1 physical custody and token issuance. Users can use stablecoins like USDC, USDT, USD1 to mint stock tokens like AAPL.M, MSFT.M, and trade 24/7 on the Base blockchain. All trading, minting, and redemption processes are executed by smart contracts, ensuring transparency, security, and auditability. MyStonks is committed to bridging the gap between TradFi and DeFi, providing users with a high-liquidity, low-barrier entry to on-chain US stock investment, building the "Nasdaq of the Crypto World".

Previous Developments:

On January 13, Maiton MSX announced that starting immediately, it would change the RWA spot trading fee collection model. After the adjustment, this section changed from the original "two-way fee" to a "one-sided fee." The specific implementation standard is that the buy direction maintains a 0.3% handling fee, and the sell direction handling fee is reduced to 0. This means that when users complete a full trading cycle of "buy + sell," the comprehensive transaction cost will be substantially reduced by 50%. This fee policy is now effective across the entire MSX platform, covering all listed RWA spot trading pairs.

Previously, Maiton MSX published a 2025 review article "Anchoring the Era Window, Co-building a New On-Chain US Stock Ecosystem," reviewing the phased achievements of the year.

Related Links

《RWA Weekly Report Series》

《What is ESE? Why is it Key to the RWA Track?》

《Listed Company U Power Issues RWA on PicWe Platform, Promoting Dynamic Energy Assets into the On-Chain Era》