Written by: Charlie Wells, Paulina Cachero

Compiled by: Chopper, Foresight News

Those trading apps that became famous for commission-free trades, fractional shares, and meme stocks, touting 'financial democratization,' are now going elite.

Robinhood, eToro, Revolut, and Public.com, once labeled as platforms for 'young people trading from their parents' basements,' are now offering investors airport lounge access, dinners, and F1 viewing perks. They are launching premium credit cards with annual fees of $695, providing exclusive concierge services for clients with million-dollar account balances, and venturing into complex tax planning, wealth management, and even trust accounts to compete with traditional legacy institutions.

A few months ago, when 29-year-old David Easterwood used his hefty 17-gram Robinhood Gold Card to buy a cowboy hat, the store clerk told him, 'You must be rich.'

And he is. The Phoenix-based retail trader registered for Robinhood as soon as he came of age in 2019, making his first trade in a few shares of Ford, followed by stocks like McDonald's. He said his account 'exploded' in 2023. According to an account screenshot he provided to Bloomberg News, he had made over $885,000 in profits since September of that year.

Beyond owning the Robinhood credit card, Easterwood also has access to Robinhood's concierge service, available only to users with assets exceeding $1 million or those with high platform activity.

'Whether I have a hundred bucks or a hundred million in my account,' he said, 'I'm staying with Robinhood.'

David Easterwood used his Robinhood Gold Card to buy this cowboy hat

As their user base ages and accumulates wealth, this is precisely the atmosphere these trading platforms are trying to create. During the pandemic, platforms like Robinhood built a young, anti-establishment, anti-Wall Street image with their low costs, 'financial democratization,' and appeal to retail investors.

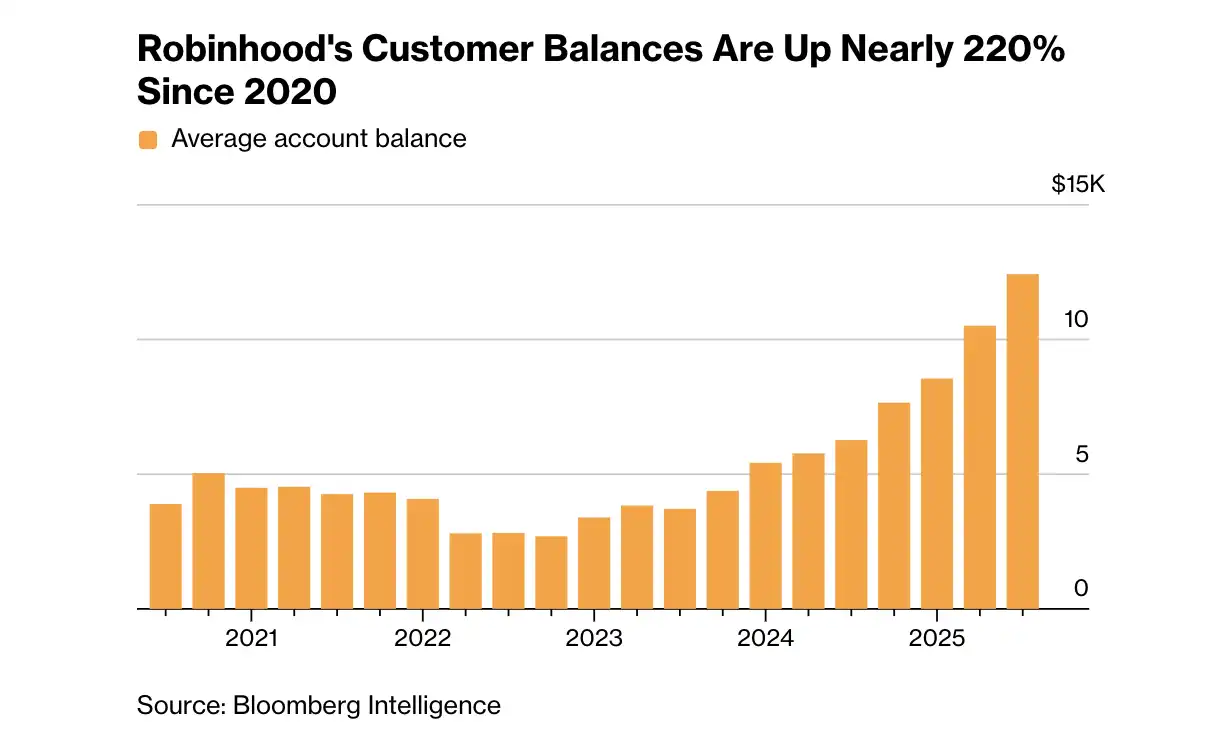

The median age of Robinhood users has risen from 31 five years ago to 36 today. The company now has over 300,000 clients with assets exceeding $100,000, an increase of more than 250% since 2022.

Public stated that its invite-only concierge service for users with assets over $500,000 or high trading activity continues to grow. eToro's membership club program offers similar high-end perks, with membership surpassing 720,000 by the end of last year, up from 579,000 a year earlier.

The evolution of these brokerage apps' products reflects both how former startups are catching up with their maturing users and the K-shaped divergence forming in many developed economies: those with limited funds get basic services, while those holding substantial assets, even if their wealth started with meme stocks, are fiercely competed for by financial institutions and enjoy various preferential treatments.

Public.com hosted a small dinner in New York in 2025, inviting members and content creators to discuss product updates and upcoming launches

'The core of our strategy is to ensure that users who build wealth on the platform don't leave,' said Deepak Rao, Vice President and General Manager of Robinhood Money. These companies don't want the clients they've painstakingly nurtured to流失 to large Wall Street wealth management institutions like Goldman Sachs, JPMorgan Chase, or Citigroup.

Abigail Sussman, a professor of marketing at the University of Chicago Booth School of Business, said this transformation is difficult, especially as brokerage apps pivot to a premium positioning that contradicts their initial brand image of 'democratizing finance.'

'It's much easier for a brand to go from high-end to mass market,' Sussman said. While a high-end fashion brand moving downmarket might dilute the brand, it already has established prestige; it's much harder for a fast-fashion retailer to move upmarket. 'Going the other way, building that high-end image and status is much more difficult.'

Nevertheless, these platforms are pushing forward with full force.

The invitation to Robinhood's launch event for its platinum card and other premium services read: 'Experience our new offerings from a first-class perspective, empowering every generation to achieve their financial goals.' The event was held at the TWA Hotel at New York's JFK Airport, unveiling a credit card with a $695 annual fee made of 99.9% pure platinum, as well as custodial and trust accounts for children.

Robinhood CEO Vlad Tenev launched the Robinhood Platinum Credit Card in New York in March

London-based fintech Revolut is aggressively moving into private banking and plans to launch more products targeting high-balance users. The company is also hiring multilingual private bankers to serve high-net-worth individuals, cross-sell products, and provide financial advice.

Public's COO, Stephen Sikes, said better data, content, and AI tools are making people more comfortable managing tens of millions of dollars on their own. The company has hired concierge specialists to communicate with high-value clients, build relationships, and optimize their experience.

Meanwhile, eToro CEO Yoni Assia said the platform's premium membership program is due for an upgrade. Currently, Diamond members, the highest tier for those with assets over $250,000, receive access to select sporting event tickets, airport lounge access, and a Visa card that offers stock rebates on spending.

'Ultimately, I want eToro to be your family office,' Assia said.

eToro CEO Yoni Assia

These emerging platforms face fierce competition from legacy Wall Street institutions that have served the wealthy for centuries. They retain generational clients through one-on-one dedicated services, access to private investments, and estate planning. At the same time, traditional banks, sitting on trillions in client assets, are also optimizing their own apps, eroding the core advantage of digital-only platforms. In this industry, great experience and marketing are far less important than trust.

And trust has been a long-standing issue for these digital brokerages. Robinhood faced major setbacks after its user base exploded during the pandemic. In 2021, the Financial Industry Regulatory Authority fined it $70 million for reasons including misleading customers and lack of internal controls, among others. Robinhood neither admitted nor denied the allegations but said it had made numerous improvements. In 2024, eToro agreed to pay $1.5 million to settle charges from the U.S. Securities and Exchange Commission that it operated as an unregistered broker-dealer and clearing agency.

The benefits of Robinhood's new platinum card are very similar to popular products from American Express and JPMorgan Chase: 5% cash back on dining, $250 in DoorDash credits annually, 10% back on hotels and rental cars, free Robinhood Gold membership, and a $250 annual credit for autonomous ride-hailing.

Ted Rossman, a senior industry analyst at Bankrate who focuses on credit cards, said this premium card doesn't surpass its competitors.

'To be honest, this card isn't as good as the Amex Platinum or the Chase Sapphire,' Rossman said. For example, the DoorDash credits have many restrictions and are far less valuable than they appear.

But Nick Ewen, Senior Editorial Director at The Points Guy, pointed out that the Robinhood card offers a different kind of value: 'Other points don't appreciate, but Robinhood's design is for you to invest long-term for growth.'

This is also why 32-year-old Polish investor John Ostrowski sticks with his eToro card. He opts for a 4% rebate in Mercedes-Benz stock, values its dividends, and says the card brings a new sense of identity.

'It's a social talking point,' he said. 'My dad uses an Amex, I use an eToro card.'

An eToro members-only event held in Dubai

However, even with the high-end光环, novelty isn't enough for some users. Some services intended to increase loyalty have backfired.

'They assigned me a CPA to help with taxes,' said 42-year-old Jason Sabshon from New York, who qualifies for Robinhood's concierge service. The platform's logic is that proper tax planning can enhance investment returns, and handling taxes within the investment process can reduce the burden at tax time. But Sabshon wasn't convinced: 'They said the person was from a company I'd never heard of. I wasn't very comfortable with that.'

Kai Schukowski, a 39-year-old man from Dubai, has accounts with multiple brokerages but says none treat their top clients as well as eToro. A few months ago, he was invited to a high-end event hosted by the platform at the Belcanto restaurant atop the Dubai Opera House, gathering top traders and executives, with an露天 reception offering views of the world's tallest building, the Burj Khalifa.

What impressed him was that the event was upscale and stylish, and there were genuinely wealthy people present. He said, 'They weren't just influencers or people trying to get famous; they were real, wealthy people.'