Editor's Note: Supply bottlenecks in AI infrastructure are spreading from GPUs, memory, data centers, and power systems to even more fundamental hardware components. Goldman Sachs and Morgan Stanley have now turned their attention to MLCCs — the multilayer ceramic capacitors long regarded as ordinary passive components.

In AI servers, MLCCs are responsible for stabilizing current and filtering noise, serving as critical components to ensure high-speed chip operation. As Nvidia's new-generation rack architecture increases MLCC usage per rack, their value is rising rapidly. Goldman Sachs expects the AI server MLCC market to grow more than fourfold between 2025 and 2030, while industry capacity is increasing at an annual rate of just over 10%. This supply-demand mismatch is becoming the core variable driving the current market cycle.

More importantly, the price cycle has already begun. Japanese leaders Murata and Taiyo Yuden have initiated price hikes, and Japanese export data are also beginning to validate demand strength. For capital markets, the MLCC logic is not complex: demand comes from AI servers and high-end automobiles, supply expansion is constrained, and price increases can significantly amplify profit elasticity.

From chips to capacitors, pricing power within the AI supply chain is shifting to more segmented and hidden links. Whether MLCCs will become the "next memory chip" still depends on whether AI server demand continues to materialize. However, it is certain that this once-overlooked fundamental component has now reached the starting point of a new cycle of simultaneous volume and price growth.

Original Article:

Supply bottlenecks in the artificial intelligence (AI) arms race are sequentially igniting opportunities across various hardware sectors. After data centers, energy infrastructure, and memory chips became focal points for capital, Wall Street giants Goldman Sachs and Morgan Stanley simultaneously pointed in their latest reports to a long-underestimated fundamental component: multilayer ceramic capacitors (MLCCs). Both institutions expect MLCCs to become the next key battleground for "volume and price growth," and this AI-driven growth cycle could be the largest in history.

Goldman Sachs analyst Daiki Takayama noted in the report that the AI server MLCC market is expected to surge from approximately ¥215 billion (about $1.4 billion) in FY2025 to about ¥920 billion (about $5.8 billion) in FY2030, an increase of over fourfold, representing a compound annual growth rate (CAGR) of 34%. Goldman Sachs stated bluntly that the current AI-driven MLCC cycle "will be the largest and longest-lasting in history, and we believe it is still in its early stages."

MLCC: The 'Invisible Heart' Keeping AI Servers Running

An MLCC (Multi-layer Ceramic Capacitor) can be understood as an extremely miniaturized, ultra-fast-response charge/discharge unit. Unlike ordinary batteries that store large amounts of energy and release it slowly, MLCCs store very little energy but can complete charging and discharging within milliseconds or even shorter timeframes. Their core function is to smooth power fluctuations and filter noise: absorbing instantaneous voltage spikes or rapidly replenishing current during voltage dips, thereby providing stable current to sensitive chips and blocking electrical interference that could disrupt digital signals.

The operating characteristics of AI servers make MLCCs indispensable. When an AI model performs massive calculations, the processor's power consumption can spike dramatically within microseconds and then drop rapidly to near zero after the computation ends. The power supply system itself struggles to respond promptly to such drastic fluctuations. MLCCs are typically placed directly near AI chips, releasing energy instantaneously when power peaks occur to prevent server crashes. As Nvidia GPUs and other AI chips need to handle billions of tasks simultaneously, a top-tier AI server rack may require up to 600,000 MLCCs working in concert to maintain system stability.

Goldman Sachs analyst Nelson Armbrust further pointed out that MLCCs have become the third-most expensive component in the AI server bill of materials (BOM), trailing only GPUs and memory. The overall MLCC market is currently about $15 billion, with the server-related market at around $1.3 billion, expanding at a CAGR of 80%. In contrast, demand growth in other application areas like automobiles and smartphones has noticeably slowed. Daiki Takayama expects MLCCs' cost share in the AI server BOM to gradually rise from about 0.5% currently to about 1%.

Structural Supply-Demand Imbalance: Annual Capacity Growth of Just 10%, Unable to Withstand Fourfold Demand Shock

The core factor sparking market attention is the severe structural supply-demand imbalance facing the MLCC industry. Goldman Sachs analyst Allen Chang explicitly stated that the annual capacity growth rate for the entire MLCC industry is only slightly above 10%. Moreover, as equipment and materials rely heavily on in-house production, expansion progress is constrained by internal engineering resources, making it difficult to accelerate significantly. However, the demand shock from AI servers is on a completely different scale. Goldman Sachs estimates that MLCC demand driven by AI servers will grow by approximately 4.3 times between FY2025 and FY2030.

Adding to market concerns, demand for high-voltage, high-capacitance MLCCs driven by automotive electrification remains robust, with per-vehicle MLCC usage continuing to rise. These two demand pillars—AI servers and electric vehicles—are jointly consuming the limited new capacity. This situation has led consumer electronics clients, despite a downturn in demand, to actively seek long-term supply agreements to hedge against future shortage risks.

Signals of current market tightness are emerging on multiple fronts: lead times for high-end MLCCs (high-capacity, high-voltage specifications) exceed 20 weeks; prices for low-capacity and consumer-grade MLCCs in spot and distribution channels have risen 20% to 40% due to stockpiling and double-ordering; prices for key raw materials like nickel and silver remain elevated, putting pressure on costs across various products.

Price Increase Cycle Officially Begins: Japanese Leaders Initiate Hikes, Official Data Confirms Trend

Price signals are intensifying rapidly. Price hike actions by Japan's two leading companies, Murata Manufacturing and Taiyo Yuden, mark the official start of the MLCC price increase cycle. Effective April 1 this year, Murata increased prices for MLCC products used in AI servers and high-end automotive applications by 15% to 35%. Taiyo Yuden has also notified customers of price adjustments across multiple product lines starting in May, involving MLCCs, inductors, RF devices, FBAR/SAW devices, and aluminum electrolytic capacitors, citing continuously rising costs of precious metals and other raw materials.

Trade statistics released by Japan's Ministry of Finance on May 28th verify this price trend at a macro level. The data shows that the average export price of MLCCs in April rose 3% month-over-month and 16% year-over-year; export volume increased 10% year-over-year; and export value surged 28% year-over-year. Goldman Sachs believes this data confirms signals from recent financial reports of Japanese MLCC manufacturers: all companies affirmed that order momentum remains strong.

Examining the timeline of the entire AI supply chain, Goldman Sachs's analytical framework shows that MLCC price increases lag significantly behind other AI core components like DRAM, NAND memory, ABF substrates, and copper-clad laminate (CCL). Therefore, Goldman Sachs judges that among all AI components and materials, MLCCs have the longest runway and strongest sustainability for price increases. Goldman Sachs has revised its forecast for the year-over-year MLCC price change in 2026 from approximately 0% previously to 0% to +5%, emphasizing that actual future increases could far exceed this level.

Remarkable Profit Elasticity: 5% Price Hike Could Boost Operating Profit Up to 37%

For investors, the profit elasticity resulting from the MLCC supply-demand mismatch should not be underestimated. Daiki Takayama estimates that a mere 5% product price increase could theoretically boost Murata's FY2027 operating profit by about 13% and Taiyo Yuden's operating profit by up to 37%.

Goldman Sachs expects Murata's FY2027 sales to reach ¥10.5 trillion (about $66 billion), a 13% year-over-year increase, and Taiyo Yuden's sales to reach ¥286 billion (about $1.8 billion), also a 13% year-over-year increase. Goldman Sachs maintains a "Buy" rating on Murata, Taiyo Yuden, and TDK. Its constructed Asia MLCC thematic stock portfolio has recently started to strengthen but still shows significant catch-up potential compared to other popular AI themes.

Morgan Stanley Disassembles Nvidia's New Rack: Rising Importance of Peripheral Components, MLCC Usage Soars 182%

Another major catalyst comes from Nvidia's next-generation Vera Rubin AI rack. Morgan Stanley, upon disassembling Nvidia's latest VR200 rack, found that the importance of peripheral components in the latest BOM is rapidly increasing.

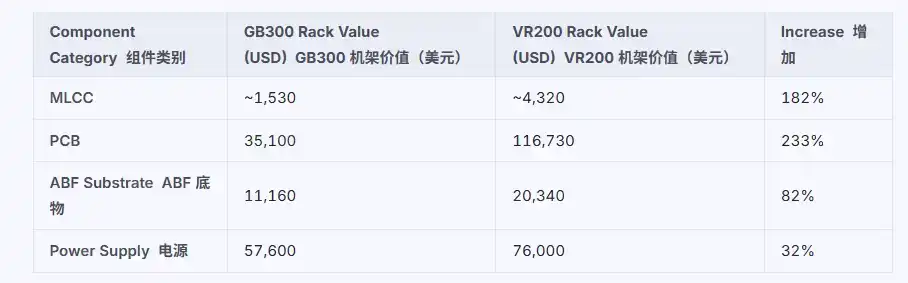

The MLCC value within a single rack has increased from about $1,530 in the previous-generation GB300 era to about $4,320, a surge of 182%. Although the absolute dollar amount of MLCCs remains lower than that of GPUs, memory, and PCBs, their growth rate among peripheral components is exceptionally prominent.

Morgan Stanley's channel checks further reveal that MLCC usage has increased significantly on both compute boards and switch boards, with the increase being more pronounced on compute boards. Additionally, the newly introduced BlueField and ConnectX modules will further boost the total MLCC usage per rack. This partly explains why current demand for high-end AI server MLCCs is so strong, prompting multiple ODM manufacturers to actively stockpile in preparation for the mass production and delivery of Rubin racks in the second half of 2026.

Morgan Stanley's disassembly of the Nvidia Vera Rubin rack shows the following changes in key component values:

Market intelligence indicates that in the infrastructure arms race of the AI supercycle, the sequential rotation of supply bottlenecks has already spawned wave after wave of market winners. Goldman Sachs's latest assessment describes MLCCs as the "new memory chip"—a passive component sub-industry standing at the starting point of a cycle of simultaneous volume and price growth.

As exponential demand shocks from AI servers and Nvidia Rubin racks emerge, lead times for high-end MLCCs exceed 20 weeks, Japanese industry leaders initiate price hikes, and official export data remain robust. All signals point to the same conclusion: this AI-driven MLCC supercycle has only just begun.