Author: momo,chaincatcher

The number of Solana nodes has dropped by 70% from its historical high. In early April, according to Solana Compass data, the number of validators plummeted from 2,560 in March 2023 to approximately 756; during the same period, the Nakamoto coefficient dropped from 31 to 20, a decrease of 35%, indicating a simultaneous weakening of decentralization.

This change comes precisely as Solana is attempting to tell a grander narrative—becoming the "on-chain Nasdaq" to host global capital markets. The sharp decline in nodes and the膨胀的野心 create a tension that is hard to ignore.

Regarding node and centralization issues, Solana has not been without responses in the past, but the results have been unsatisfactory. Recently, according to a SolanaFloor report, the Solana Foundation is set to implement a new validator policy, officially effective on May 1. What is the focus of this new policy? And can it change the current situation?

I. Why Has the Node Count Dropped Significantly?

Judging from the trend of changes in the number of Solana nodes, the sharp decline in the number of validators is not a sudden drop. Since the beginning of 2024, the node count has been continuously declining, gradually falling below 1,000.

The significant drop in the number of nodes caused panic in the community earlier this year. Solana founder Toly later responded that the main reason was the end of subsidies.

For a long time, Solana has been criticized for insufficient nodes and excessive centralization. To quickly expand the validator scale, Solana early on launched the Solana Foundation Delegation Program (SFDP), which provided support to small and medium-sized nodes through three methods: staking matching,剩余委托, and voting cost subsidies.

Simply put, the Foundation matched external staking at a 1:1 ratio, up to a maximum of 100,000 SOL; the remaining SOL after matching was evenly distributed to all eligible validators; and daily voting transaction fees were also subsidized. This mechanism was indeed effective in the short term. A report released by Helius in August 2024 showed that at its peak, over 70% of validators relied on this system to varying degrees.

However, problems soon emerged. These subsidy-dependent nodes, although accounting for the majority in number, controlled only about 19% of the total network stake; in contrast, the approximately 420 nodes that did not rely on subsidies controlled over 80% of the staking share, with the top 20 nodes accounting for over one-third of the stake.

Clearly, a large number of nodes does not mean "decentralization." The subsidies attracted a large number of low-stake, low-performance "nominal nodes" that, although分散, were unable to participate in real staking competition; institutions and large holders with substantial SOL preferred to allocate resources to large nodes that were technically reliable and operationally stable.

This also explains why the Nakamoto coefficient did not increase同步ly during the previous period of虚高 growth in node numbers.

For Solana, rather than maintaining a large number of underperforming, minimally contributing "nominal nodes," it is better to establish a smaller but more professional validator set to ensure the long-term stability and security of the network. Thus, Solana began主动ly收缩 subsidies.

Starting in 2025, the Foundation gradually adjusted its delegation strategy, phasing out nodes that had long relied on subsidies. The core mechanism was summarized as "one in, three out": for every new subsidized node added, three old nodes were to be淘汰 based on two criteria—having obtained Foundation delegation eligibility for at least 18 months and having external staking below 1,000 SOL. According to estimates at the time, about 51% of nodes met the淘汰 criteria, potentially around 686 nodes.

After the subsidies exited, survival became more difficult for small and medium-sized nodes. Analysis indicated that a node needed to have approximately 3,500 SOL for staking and annual maintenance costs of about $45,000 (with voting fees being the major component, around 400 SOL) to survive.

At the same time, competition within the network intensified, with top validators competing for delegation with almost zero fees, further compressing the profit margins of small and medium-sized nodes.

Furthermore, network upgrades like Alpenglow, which increased hardware performance requirements, led to the gradual淘汰 of older equipment, raising the entry barrier for validators.

However, the出清 of small and medium-sized nodes and the significant drop in node count still raised community concerns about excessive power concentration. A Twitter user commented: "Users use PoS chains for security, but the chain becomes centralized in the pursuit of security. So what are we supporting?"

II. What Is the Purpose of Solana's New Validator Policy?

Against this backdrop, let's examine Solana's latest validator delegation plan.

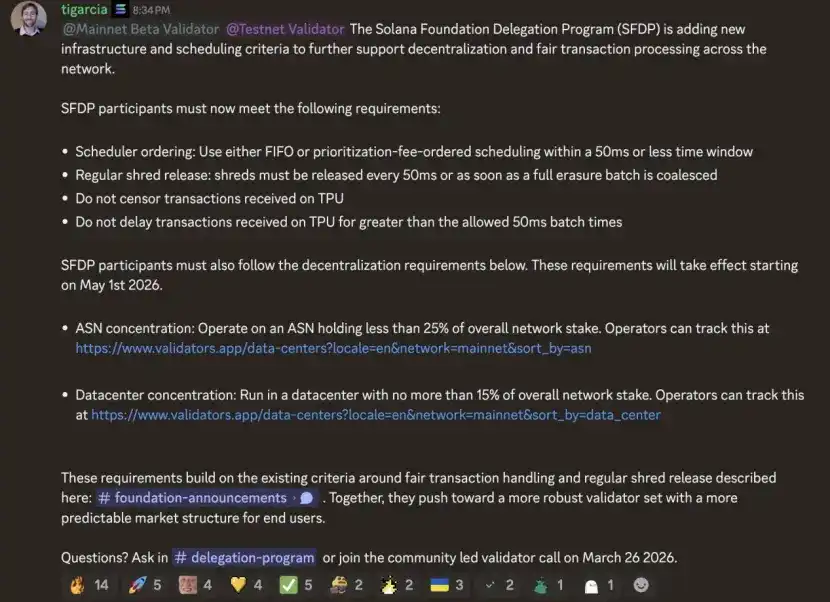

The most core change focuses on strong constraints on the infrastructure layer.

The staking proportion carried by any single ASN (which can be understood as a cloud provider or network service provider) must not exceed 25%, and the proportion of any single data center must not exceed 15%.

In other words, even if you run a compliant and stable node, you may lose the Foundation's delegation support simply because "too many people are in the same place."

The logic behind this is not complicated. Currently, Solana's validators, although seemingly分散 in number, are highly concentrated in terms of physical location within a few cloud providers and data centers. A Helius report once mentioned that two hosting service providers controlled over 40% of the network's total staking, mostly concentrated in Europe. According to sources who spoke to ChainCatcher, the Solana Foundation has also begun有意ly supporting nodes in Asia.

Therefore, this new rule is more like a "forced split." The goal is not to increase the number of nodes, but to require nodes to migrate out of overly concentrated infrastructure,重新分散 the risks that were originally stacked behind a few nodes.

At the same time, the rules further tightened the freedom of validators at the execution layer. This includes requiring transaction ordering to be completed within 50 milliseconds, processing transaction priority according to既定 rules,强制 releasing data shards according to a schedule, and explicitly prohibiting the审查 or delaying of transactions received by the TPU. This series of constraints directly addresses the long-standing issues of MEV competition and execution opacity. Essentially, it compresses the "operational space" of validators,换取 network consistency with more standardized rules.

In terms of direction, this is a further upgrade on last year's "one in, three out" policy, using rules to screen out more qualified nodes.

But controversy也随之而来. Node operator Chainflow raised concerns in public discussions.

On the one hand, according to the current rules, whether a node can continue to receive delegation does not depend entirely on its operational quality, but on its "location." If a particular cloud provider or data center has already reached the upper limit, then regardless of the node's own performance, as long as it remains deployed there, it may be excluded from the subsidy system. This means that some long-term, stable small validators may lose their生存空间 simply because they are "in an overly crowded environment."

On the other hand, the more realistic issue is the migration itself. High-quality infrastructure resources are already concentrated in the hands of a few large service providers. Once small and medium-sized nodes are forced to migrate, they often have to choose data centers with worse performance and stability. In this case, node performance declines, block production rates drop,进而 affecting收益, which may反而 accelerate their淘汰 by the market.

In summary, Chainflow believes that for small and medium validators, the biggest uncertainty brought by the new rules is not the technical threshold, but an淘汰 mechanism "unrelated to their own capabilities." Therefore, Chainflow suggests that instead of setting a rigid upper limit on the "全网占比," it would be better to refine the restrictions to the proportion of subsidy allocation within individual data centers, achieving more精细化分散 while retaining high-quality infrastructure.

The new policy has less than a month to be implemented and is likely to further squeeze some small and medium validators, causing the node count to drop. But the final effect will have to be seen from the data on the Ghost platform and the Foundation's implementation details after May 1.

III. The "On-Chain Nasdaq" Competition

Public chains have now entered the competition to host global capital markets—the "on-chain Nasdaq"之争.

For traditional financial capital, "fast" and "cheap" are important, but the前提 is "security" and "compliance." This means that the node centralization issue long criticized in Solana will be significantly放大 when facing institutional narratives.

According to data from RWA.xyz, Ethereum still dominates in RWA asset value, with on-chain deployed assets exceeding $16 billion, accounting for over 55% of the market share; BNB Chain ranks second with $3.5 billion and a 12.13% share; Solana ranks third with approximately $1.9 billion and a 6.65% share. Large tokenized treasury and private credit platforms on the institutional side are mostly still deployed on the Ethereum ecosystem.

In terms of RWA assets, Solana's number of wallets and active addresses have now surpassed Ethereum's. The growth of on-chain RWA users mainly stems from the launch of tokenized xStock stocks in mid-2025. Solana,凭借 its speed and low cost, has torn open a gap on the retail user side.

In this competitive landscape, both Ethereum and Solana are undergoing key upgrades in 2026, each addressing their shortcomings. Ethereum's main line is through the two major upgrades, Glamsterdam and Hegotá, the core of which is to make the mainnet faster and more efficient—through parallel execution, increasing the Gas limit, optimizing transaction ordering, while simultaneously lowering the node门槛 to allow more people to participate in validation.

On Solana's side, the focus is on补课 stability and risk resistance. In addition to the aforementioned node新政, it has upgraded the consensus mechanism to compress final confirmation time from seconds to milliseconds, and simultaneously introduced a second independent client to avoid "the entire network crashing if one software crashes."

These two routes are converging in the same direction. At the current stage, when真正的 institutional funds and RWA assets begin to大规模 move on-chain, the market优先 chooses infrastructure that is more mature, stable, and predictable. For Solana, the key lies in whether it can solve structural problems like centralization and turn "fast" into "trustworthy fast."