New revenue hierarchy? How Hyperliquid is outpacing legacy chains

ambcryptoPublished on 2026-04-06Last updated on 2026-04-06

Abstract

The blockchain value capture model is shifting from passive transfers to active trading, with perpetual trading volume ($8.4B) far exceeding spot DEX activity ($3.7B). Hyperliquid exemplifies this trend, capturing 36.4% of DeFi fees by March 2026, while Ethereum and Solana see declining shares. Its derivatives platform generated $154.95B in total volume from 212,843 traders, driving $12.43M in fees. A key mechanism redirects fees—$403,475 in 24 hours—to buybacks, removing 10,794 HYPE tokens from circulation. This creates a feedback loop where trading activity fuels fees, buy pressure, and token value appreciation, highlighting how specialized trading platforms now dominate value capture over general-purpose chains.

The way blockchains capture value is shifting, as activity moves from passive transfers toward active trading flows. Earlier models relied on broad usage, where simple transactions supported network value.

Now, trading dominates the landscape.

Perpetual volume hovered around about $8.4 billion in 24 hours, far exceeding the $3.7 billion seen across Spot DEX activity. This shows capital now concentrates around continuous trading rather than one-time transfers.

Fee distribution follows this shift, with Hyperliquid contributing about $618,377 out of $41.45million total DeFi fees. This evolution reshapes the market, where value depends more on trading intensity, which favors specialized platforms over general-purpose networks.

Hyperliquid dominance signals a new revenue hierarchy

A clear shift is unfolding in how blockchains earn, and it starts with where user activity is actually happening.

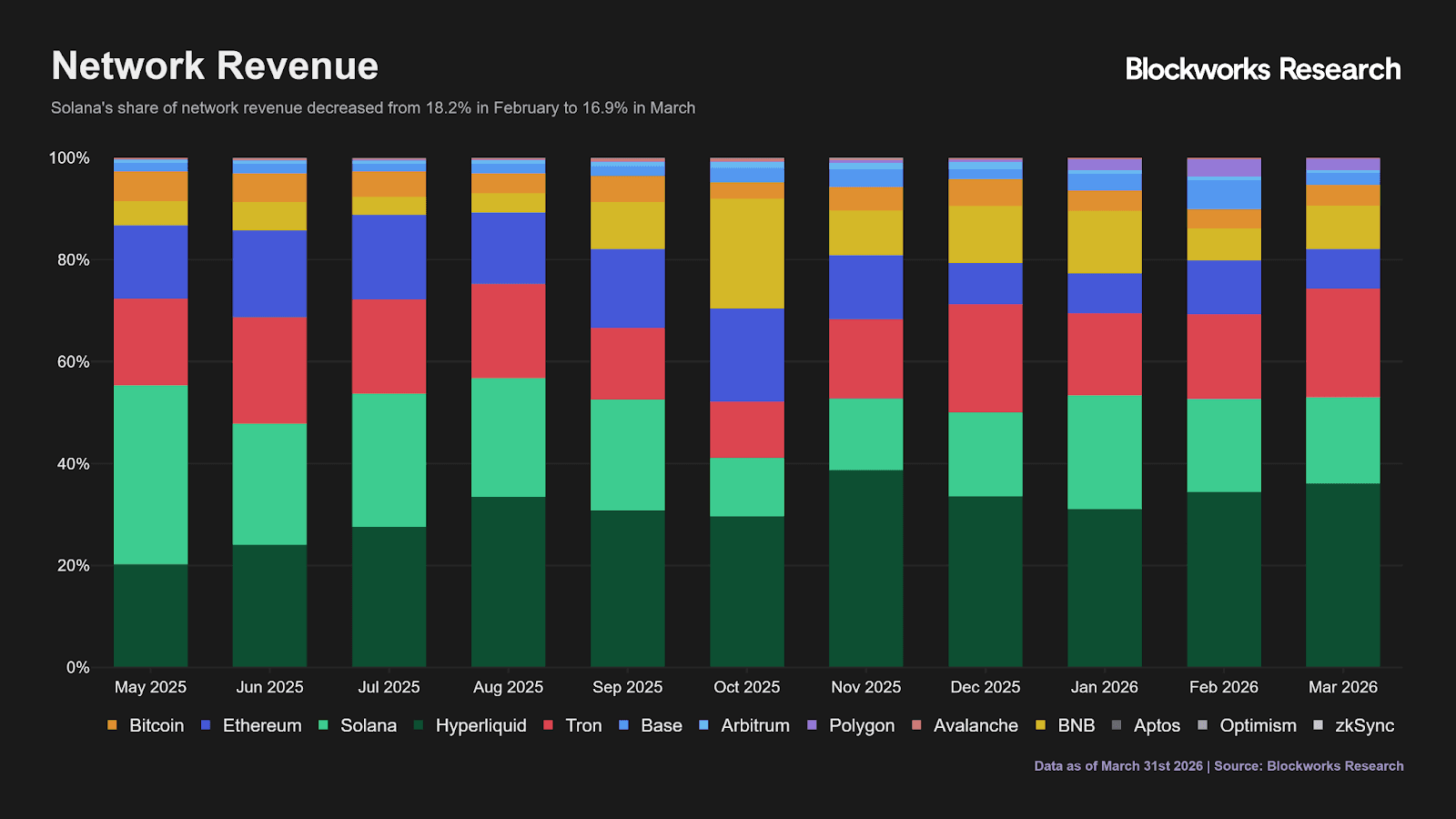

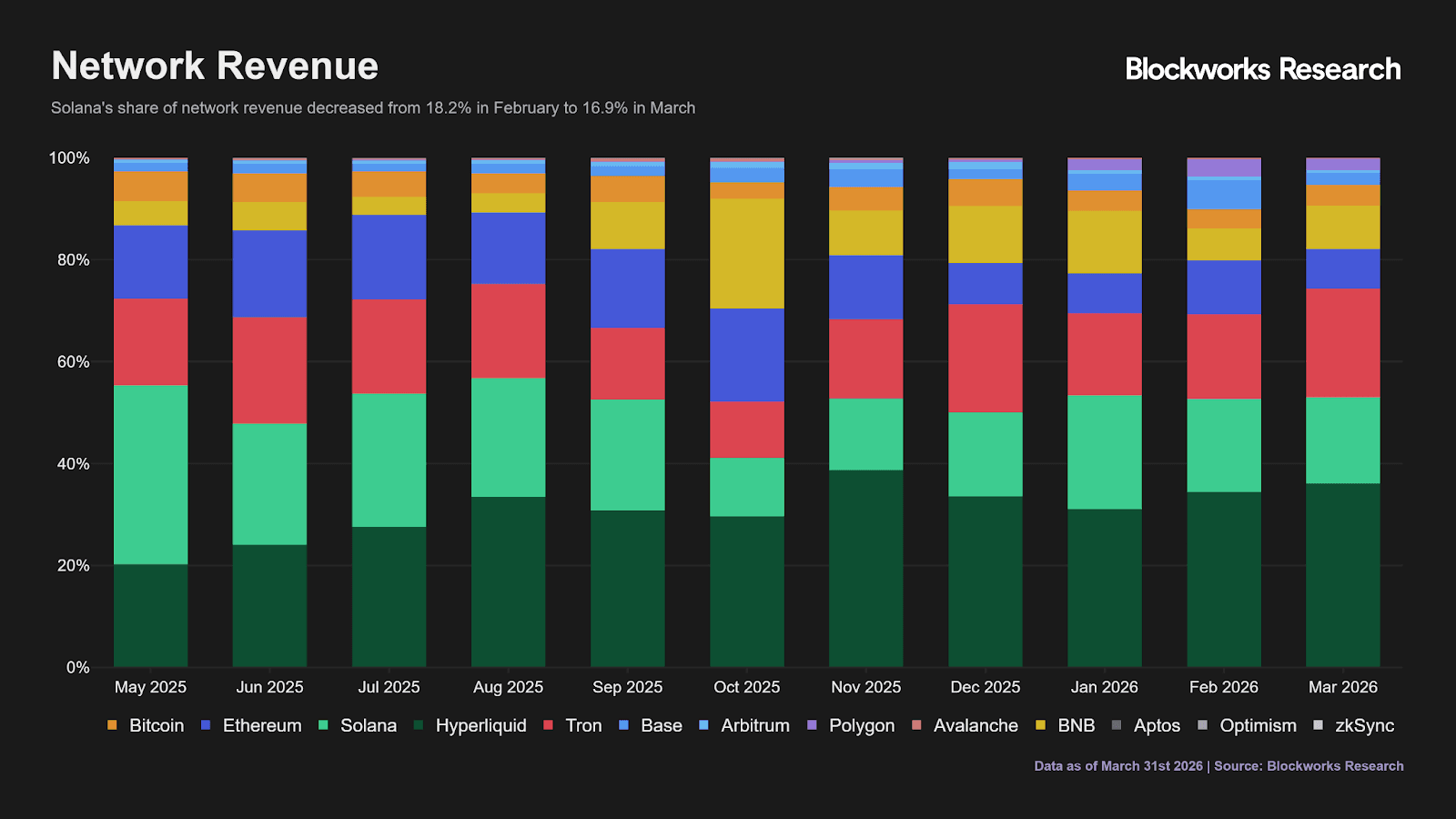

Hyperliquid’s share rose steadily through 2025, reaching about 36.4% by March 2026, which shows traders are concentrating on derivatives platforms.

Source: Blockworks Research

This shift builds as perpetual trading creates continuous fee flow rather than one-off transactions. Capital prefers environments where it can rotate quickly, which naturally pushes revenue toward trading-focused chains.

Solana [SOL] holds near 16%, slipping from 18%, which suggests usage remains strong but loses share as competition intensifies. Meanwhile, Ethereum [ETH] drops toward 7.7%, and Base near 2.4%, showing that broad activity does not translate into fee capture.

This changes market dynamics, where value follows trading intensity, pushing users and liquidity toward platforms that monetize activity more efficiently.

Hyperliquid turns trading activity into direct value capture

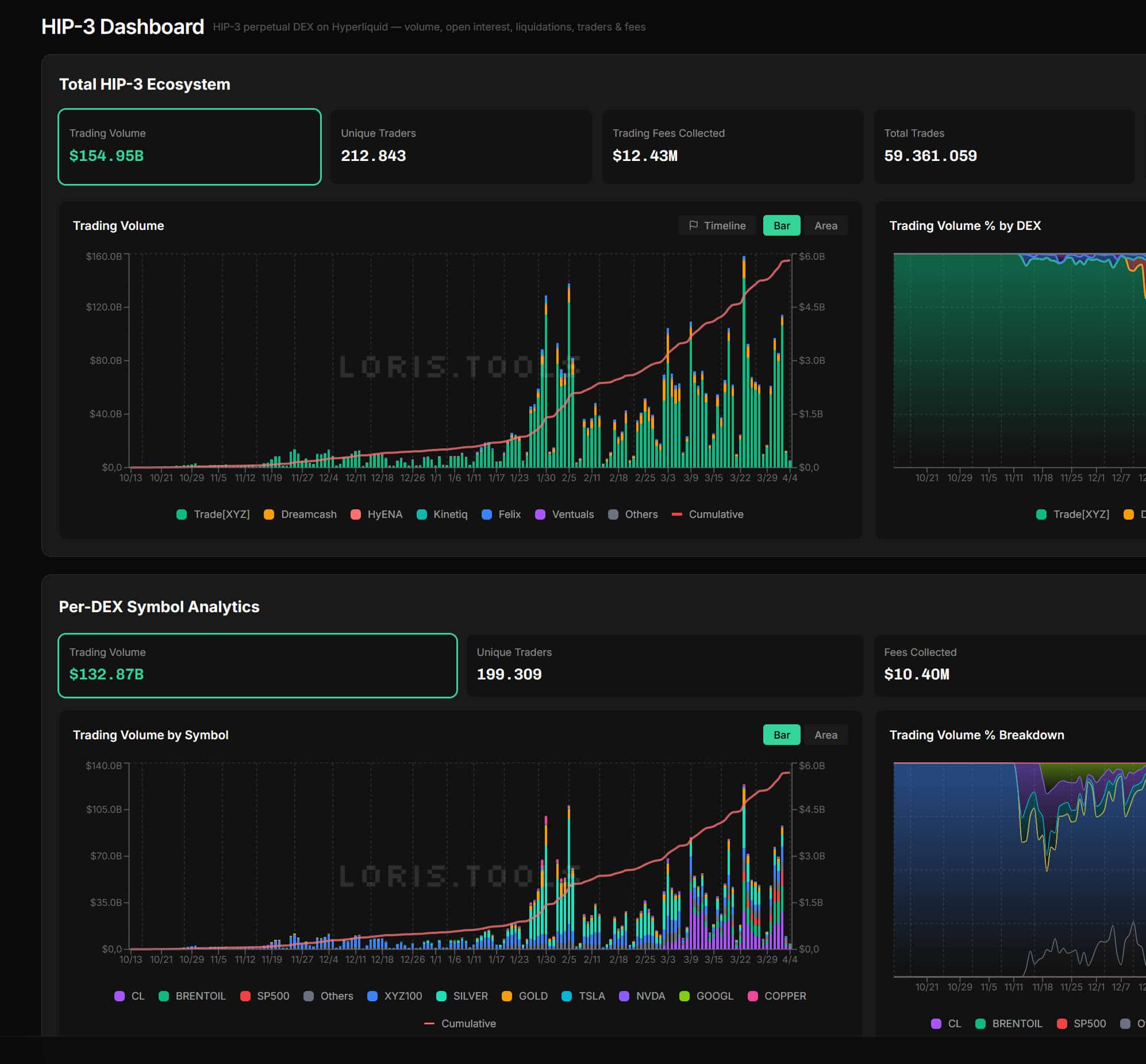

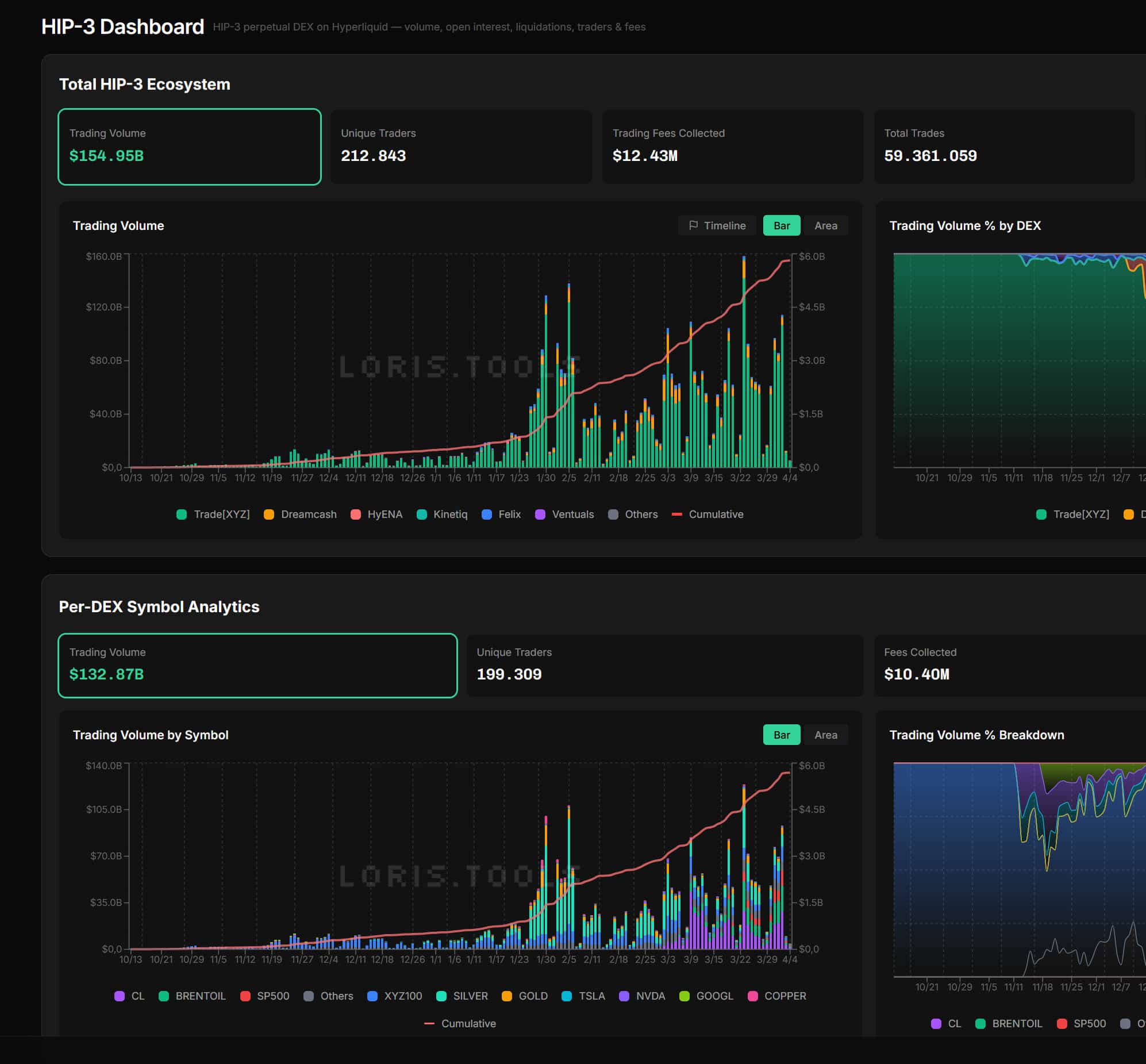

HIP-3’s growth shows how quickly derivatives activity can scale when real trading demand enters the system. Total volume reaches about $154.95 billion, supported by 212,843 traders executing roughly 59.36 million trades.

Source: X

This progression builds gradually, then accelerates into sharp spikes from January, where daily volumes expand and cumulative growth trends higher.

As participation increases, fees rise to about $12.43 million, confirming steady monetization alongside activity.

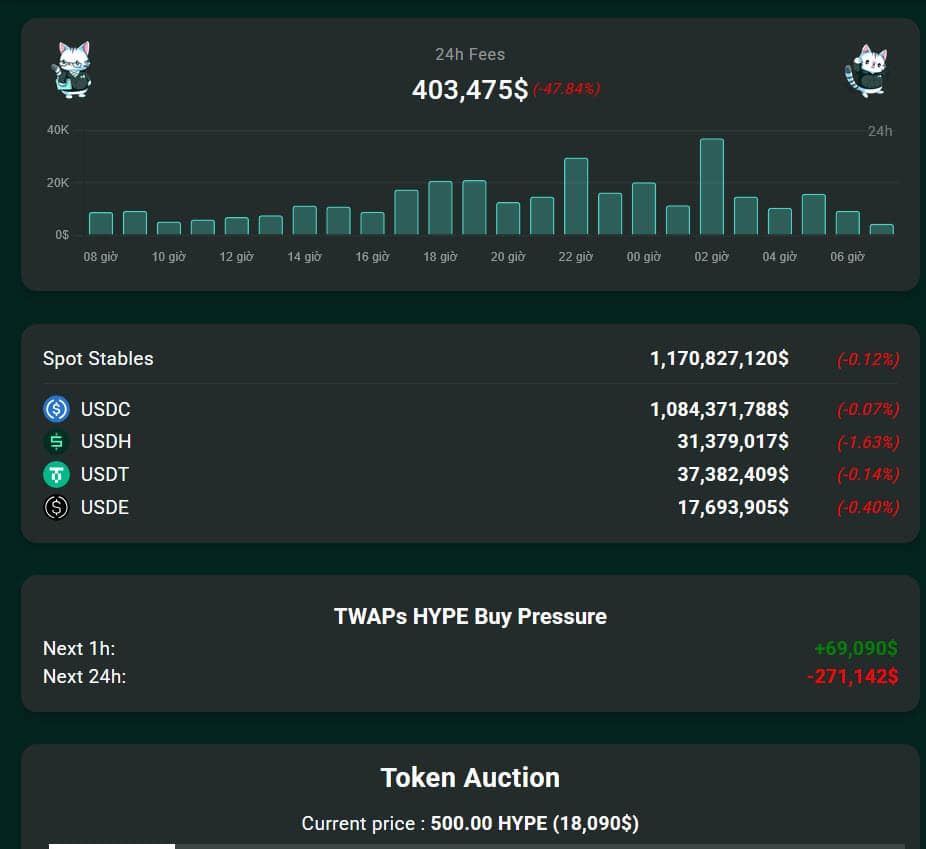

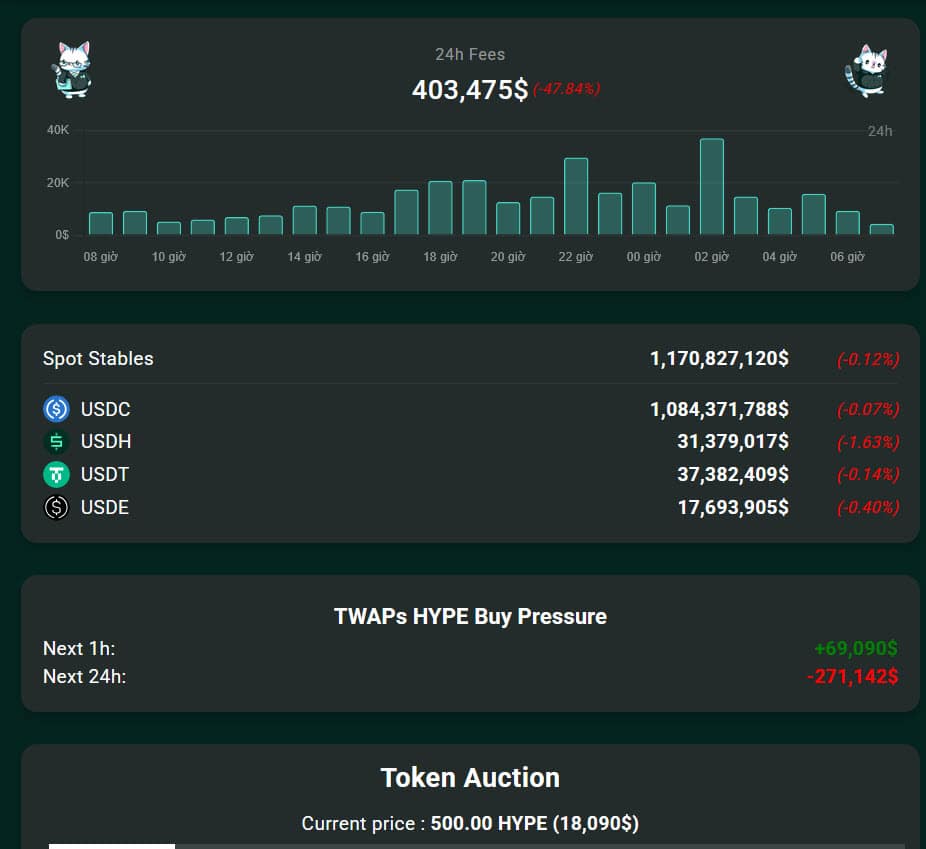

That activity does not remain abstract, as it feeds directly into token dynamics. Over the last 24 hours, fees reached about $403,475, all redirected into buybacks that remove roughly 10,794 HYPE from circulation.

Source: X

This creates a continuous loop, where trading drives fees, fees drive buy pressure, and reduced supply begins to support value as activity deepens.

Final Summary

Hyperliquid [HYPE] shows how trading-driven activity now dominates value capture, as continuous derivatives flow converts volume directly into fees and supply reduction.

Hyperliquid strengthens its market position as revenue concentration shifts toward specialized platforms, where sustained trading activity supports both liquidity and token value.

Related Questions

QWhat is the main shift in how blockchains capture value according to the article?

AThe main shift is from passive transfers toward active trading flows, with perpetual trading now dominating and creating continuous fee generation rather than one-off transactions.

QHow much of the total DeFi fees did Hyperliquid contribute, as mentioned in the article?

AHyperliquid contributed about $618,377 out of a total of $41.45 million in DeFi fees.

QWhat percentage of the market share did Hyperliquid reach by March 2026?

AHyperliquid reached about 36.4% of the market share by March 2026.

QHow does Hyperliquid's fee mechanism directly impact its token (HYPE)?

AFees generated from trading activity are used for buybacks, which remove HYPE tokens from circulation, creating buy pressure and supporting token value through supply reduction.

QWhat does the comparison between perpetual volume and Spot DEX activity indicate about capital concentration?

APerpetual volume of $8.4 billion far exceeded Spot DEX activity of $3.7 billion in 24 hours, showing capital now concentrates around continuous trading rather than one-time transfers.