Author:P Equity Research

Compilation: Shenchao TechFlow

Shenchao Commentary: P Equity Research presents a judgment that few have seriously considered: the three memory giants (Samsung, SK Hynix, Micron) are pushing the AI capital expenditure cycle towards a breaking point with price hikes. DRAM contract prices are approaching a 700% year-over-year increase, and memory is projected to account for 40% of cloud providers' capital expenditures by 2027. The author predicts an inflection point arriving around mid-2027, much earlier than the widely anticipated 2030. A contrarian take on the memory cycle.

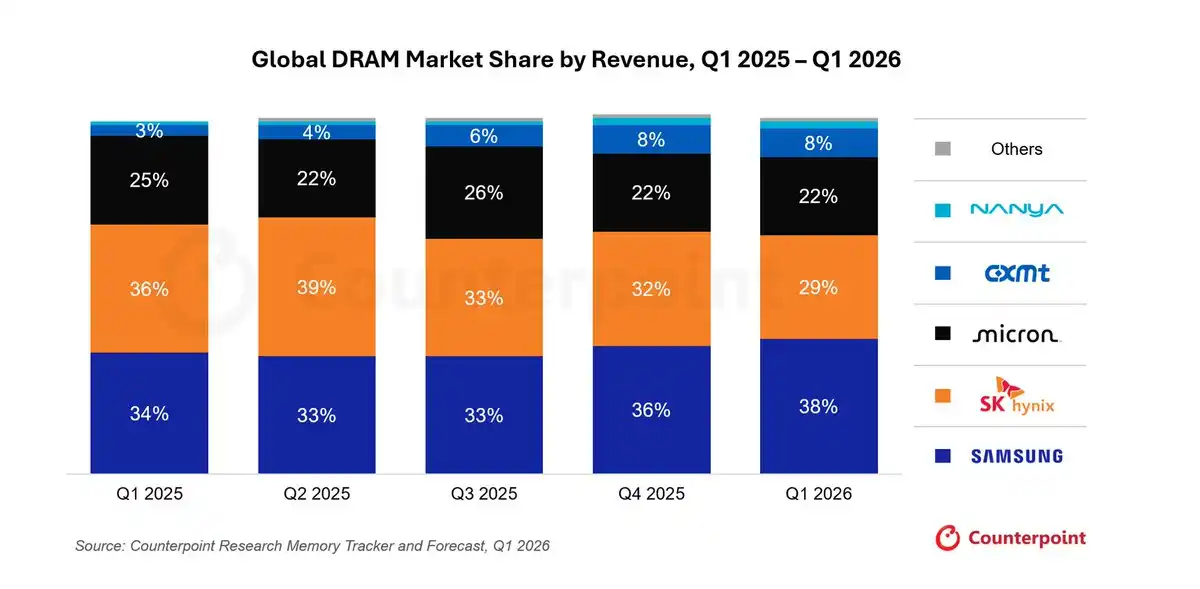

Three Giants Control 89% of the DRAM Market

SK Hynix (000660.KS), Micron (MU), and Samsung ($005930.KS) dominate the DRAM market with a combined 89% share, with Samsung alone holding 38%. This is an oligopoly.

Chart source: Counterpoint Research

These DRAM manufacturers have seized the supply-constrained situation, pushing prices higher quarter after quarter to an alarming level.

The logic is simple: to build advanced chips, you need DRAM.

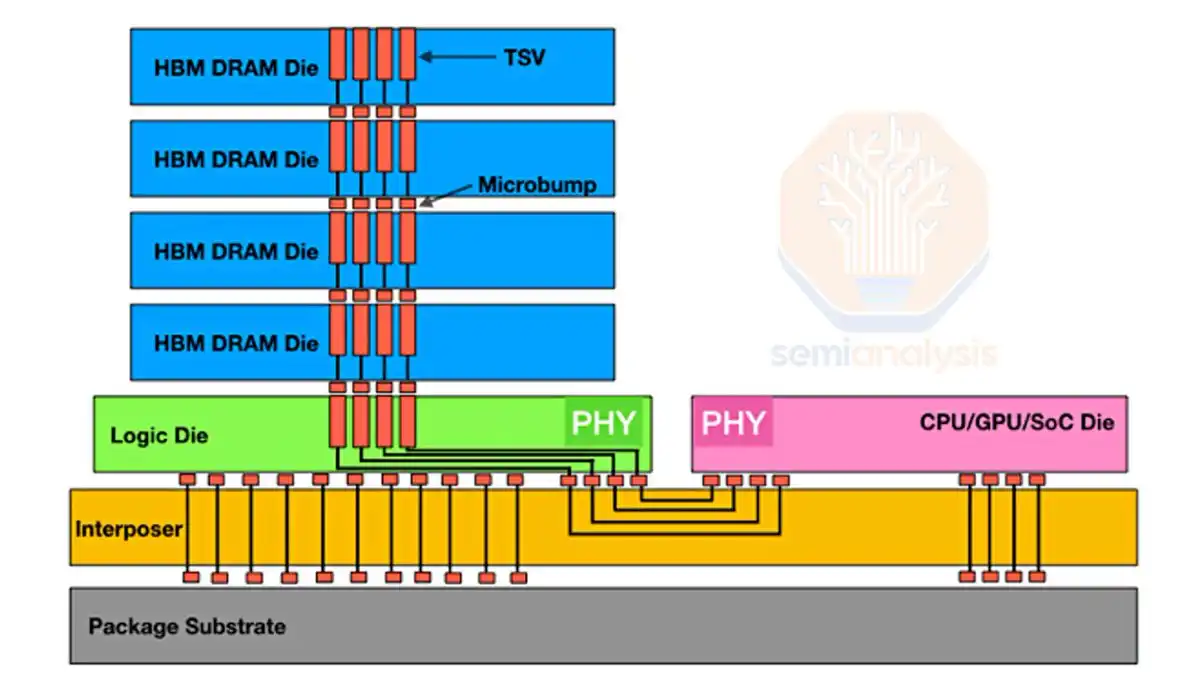

How DRAM Becomes HBM

A brief aside to explain how DRAM turns into HBM.

Stack DRAM dies layer by layer, connecting them in the middle with TSVs (Through-Silicon Vias), and you get HBM.

Chart source: SemiAnalysis

In a regular DRAM chip, data has to travel to the edge of the silicon die to find wires. HBM is different. Manufacturers use lasers and chemical etching to drill thousands of micron-sized holes in the middle of the die, fill them with copper, creating TSVs. These act like vertical shafts, penetrating the entire chip stack.

Between each DRAM layer, thousands of tiny solder balls called microbumps are placed. The entire stack is heated, the solder melts, connecting the TSVs of the upper and lower layers, forming a continuous, ultra-high-speed vertical data highway.

That's the process of turning DRAM into HBM.

Chart source: Bloomberg

As computing power demands more advanced chips, the number of layers in HBM also increases. HBM3 has 12 layers, HBM4 aims for 16. More layers mean higher bandwidth and capacity—this is the trend.

Back to DRAM demand: stronger chips require more memory, tightening the memory market further.

My Grievance with These Manufacturers: 60% Gross Margin Isn't Enough

These manufacturers could live like kings on 60% gross margins, yet they keep squeezing for more. I believe they are actively sacrificing the AI capital expenditure cycle for higher profits.

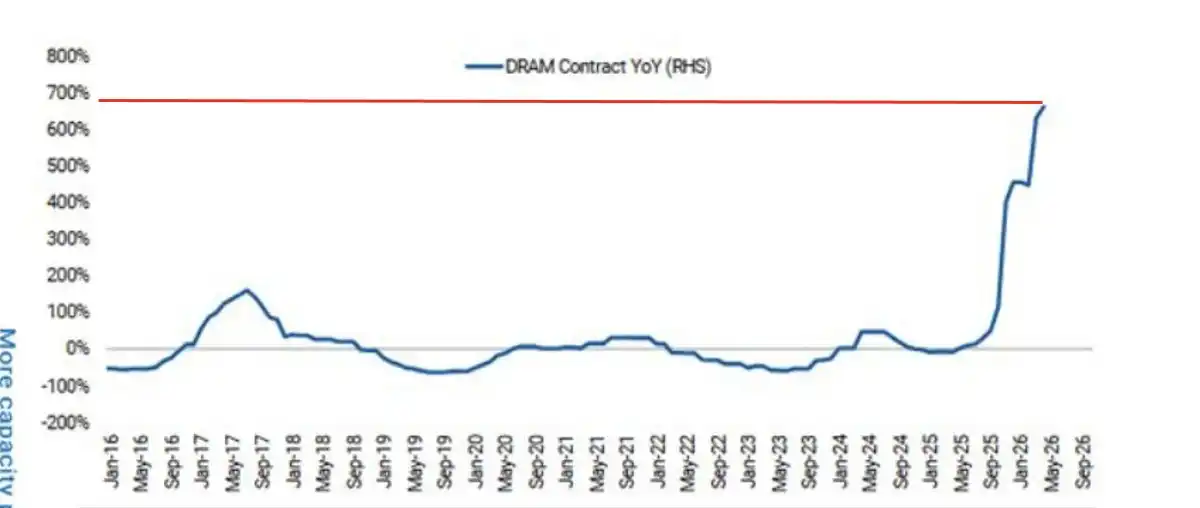

So far, no one knows when the peak in gross margins will occur. This is one reason I'm writing this.

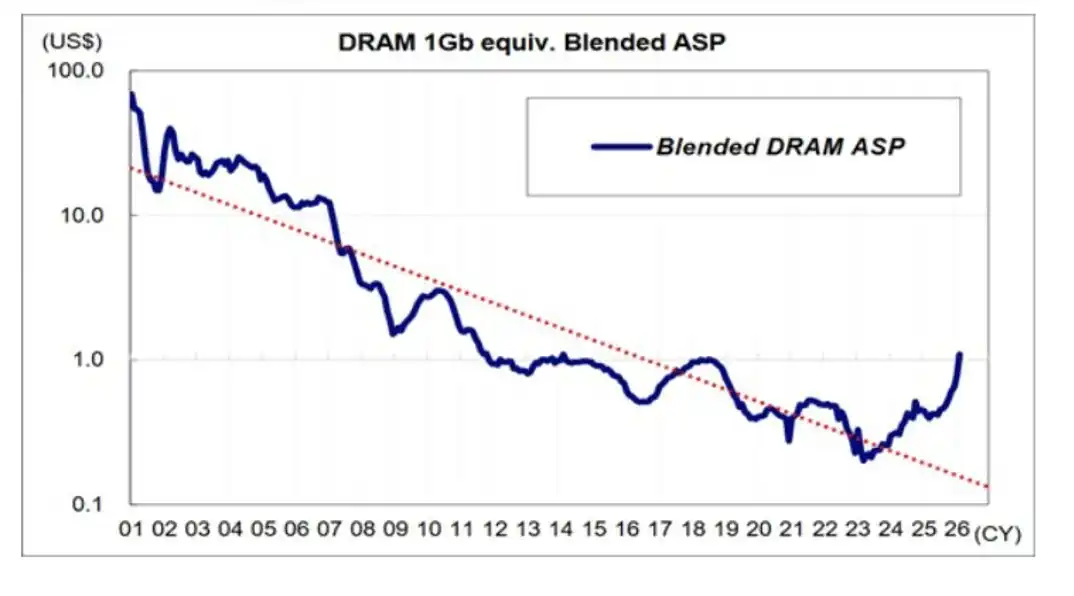

What is certain is that for the remainder of calendar year 2026 (CY26), prices will continue to rise. DRAM contract prices are nearing a 700% year-over-year increase.

Chart source: Morgan Stanley

Micron, Samsung, and SK Hynix delayed large-scale capacity expansion plans until 2024-2025. These companies have all experienced boom-and-bust cycles before—prices rise, then when demand recedes and supply exceeds, prices crash.

Chart source: Morgan Stanley

I don't blame them for delaying this long, for two reasons:

Past expansions have crushed memory margins; staying patient during an expenditure cycle provides better demand visibility.

The problem is, they now hold global pricing power, enough to strangle the entire capital expenditure cycle, and this point hasn't garnered enough attention.

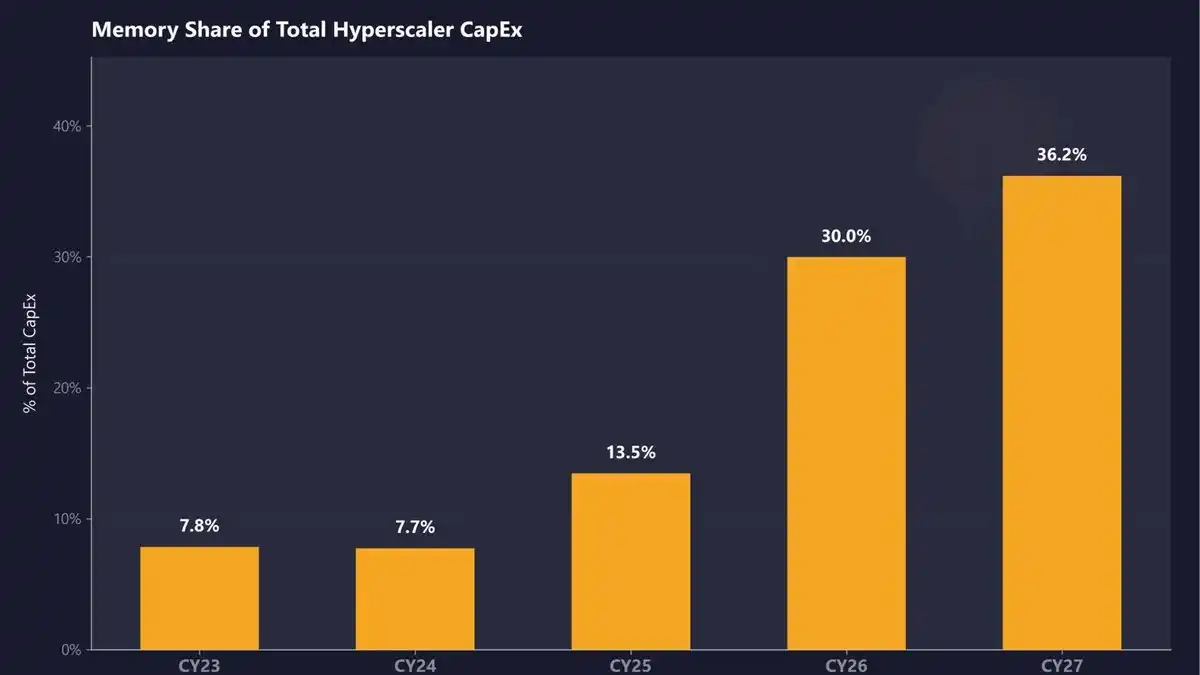

Memory to Account for 30% of Cloud Provider Capex in 2026, I Bet It Hits 40% by 2027

Memory is projected to account for 30% of hyperscaler capital expenditure in CY26, rising to 36.2% in 2027.

Chart source: SemiAnalysis

I believe even these estimates are low, as memory prices have consistently exceeded forecasts. I predict the memory share will reach 40% in CY27.

Take ALETHEIA CAPITAL as an example:

"We now expect server DRAM ASPs to jump another 30% in FQ3 2026 (previously expected 10-15%); a further 10-15% increase is possible in FQ4 (consistent with prior expectations). For HBM ASPs, we expect a year-over-year doubling in 2027."

Chart source: ALETHEIA CAPITAL

They even forecast that memory's content value within AI hardware will rise from just over 40% in 2025 to over 70% by 2027, exceeding 90% for some memory-intensive racks.

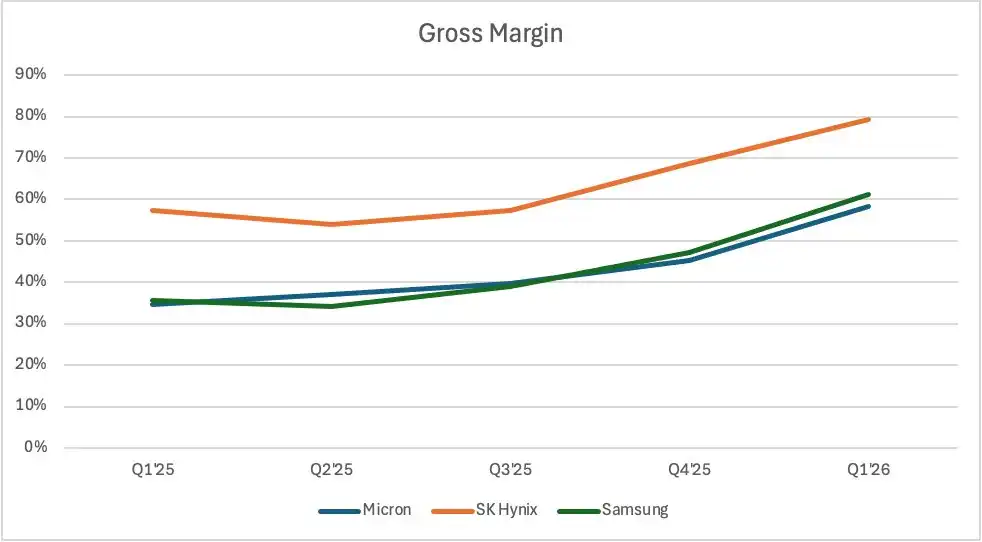

Chart source: Company financial reports, P Equity Research

Samsung and Micron's gross margins could touch the low-to-mid 70%s, SK Hynix the mid-80%s. This situation could persist through 2027 and into 2028.

Micron CEO Sanjay Mehrotra said in a Bloomberg interview that meaningful new capacity won't come online until 2028.

Video: https://x.com/MilkRoadAI/status/2066231053749006634/video/1

Wait until 2028?

Memory costs might not peak until 2028, while cloud providers with already tight free cash flow (FCF) will have to adjust spending to counter rising memory costs.

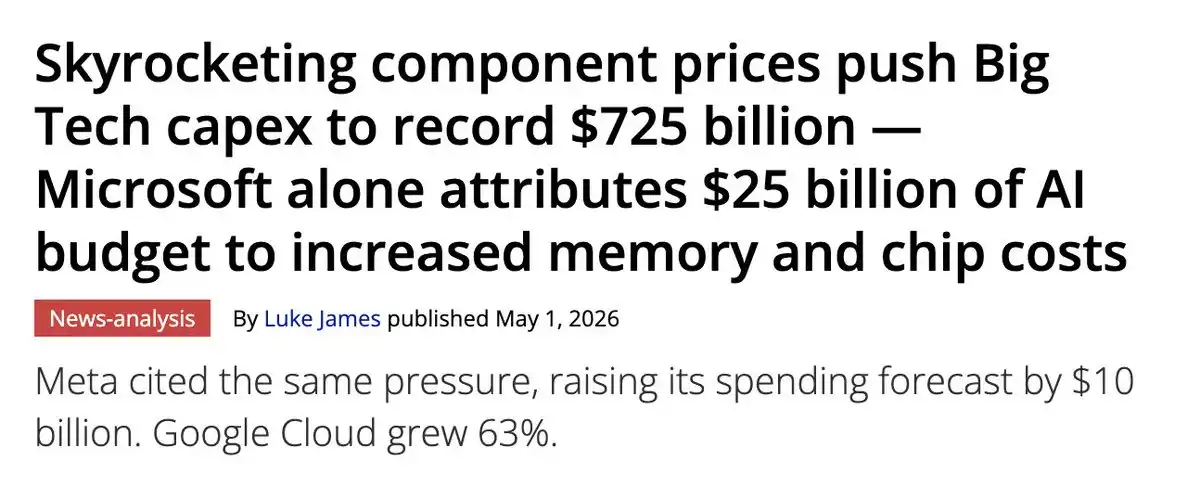

Microsoft Throws an Extra $25 Billion at Memory and Chips

Chart source: Tom's Hardware

To cope with memory and chip price increases, Microsoft raised its capital expenditure guidance by $25 billion. $25 billion.

Other cloud providers haven't given specific numbers directly tied to memory costs, but the wording is similar, or indirectly acknowledges it:

Meta said "component pricing is higher this year, particularly for memory"; Microsoft said "component pricing is higher"; Amazon said "memory pricing has spiked due to supply constraints and strong industry-wide demand."

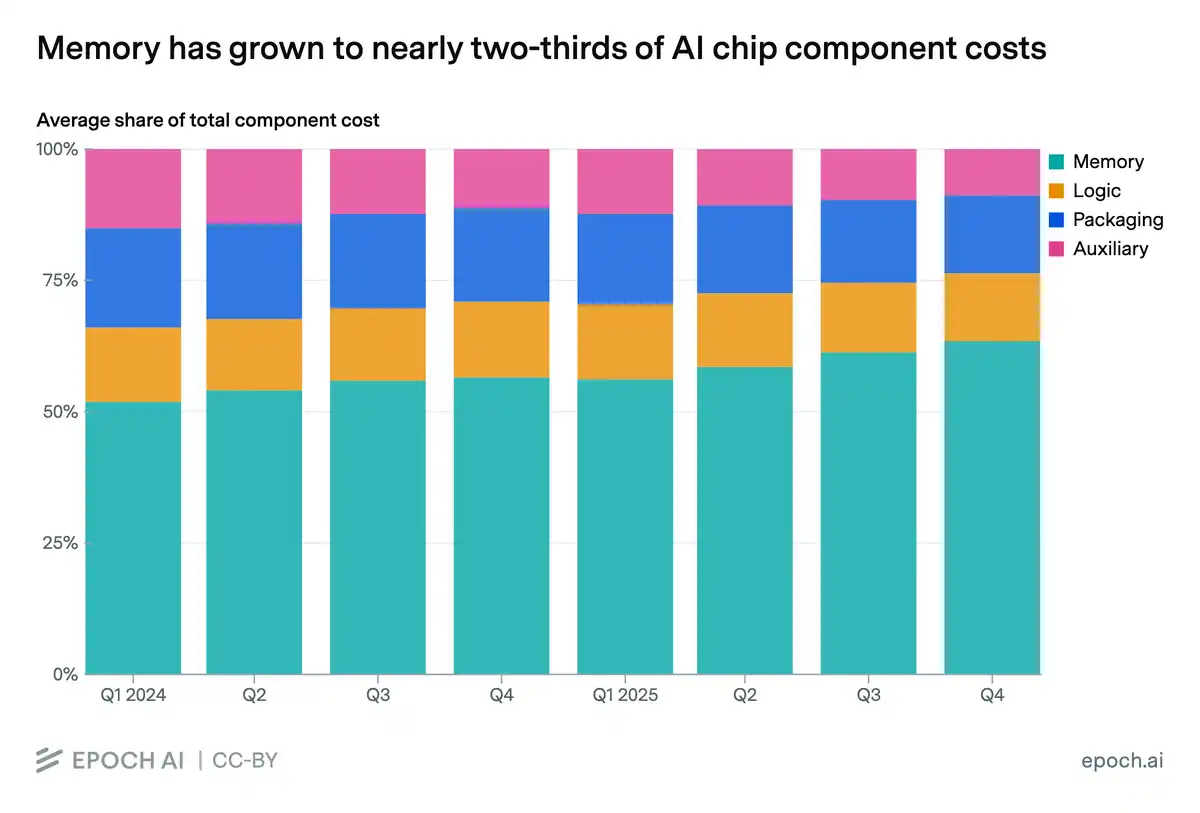

Chart source: EPOCH AI

Ask anyone, memory has become a cost threat to all. It accounted for 64% of total component cost in Q4, likely exceeding 70% by end-2026.

What can cloud providers do? Nothing. Not even Long-Term Agreements (LTAs) can save them.

Simply put, cloud providers face skyrocketing memory costs because they need both HBM and memory modules. HBM production consumes three times the capacity of regular server memory. Factories are frantically shifting equipment to HBM, causing supply for regular server memory to collapse, pushing prices up sharply.

LTAs have hard ceilings on the volume available at discounted prices. The AI boom came too fast, cloud providers almost instantly exhausted their contract allowances. Any additional demand must be purchased at current market prices.

Chart source: TrendForce

Cloud providers have no choice but to sign new LTAs with memory makers. These contracts are now for 3-5 years, not one. Chipmakers want to lock in quickly to hedge against rapid DRAM price hikes. Worse, these LTAs lock in older memory that won't be adopted at scale in the future. Transitioning from HBM3 to HBM4 means another price jump.

Cloud providers remain in a passive position, with pricing power firmly in the hands of this alliance.

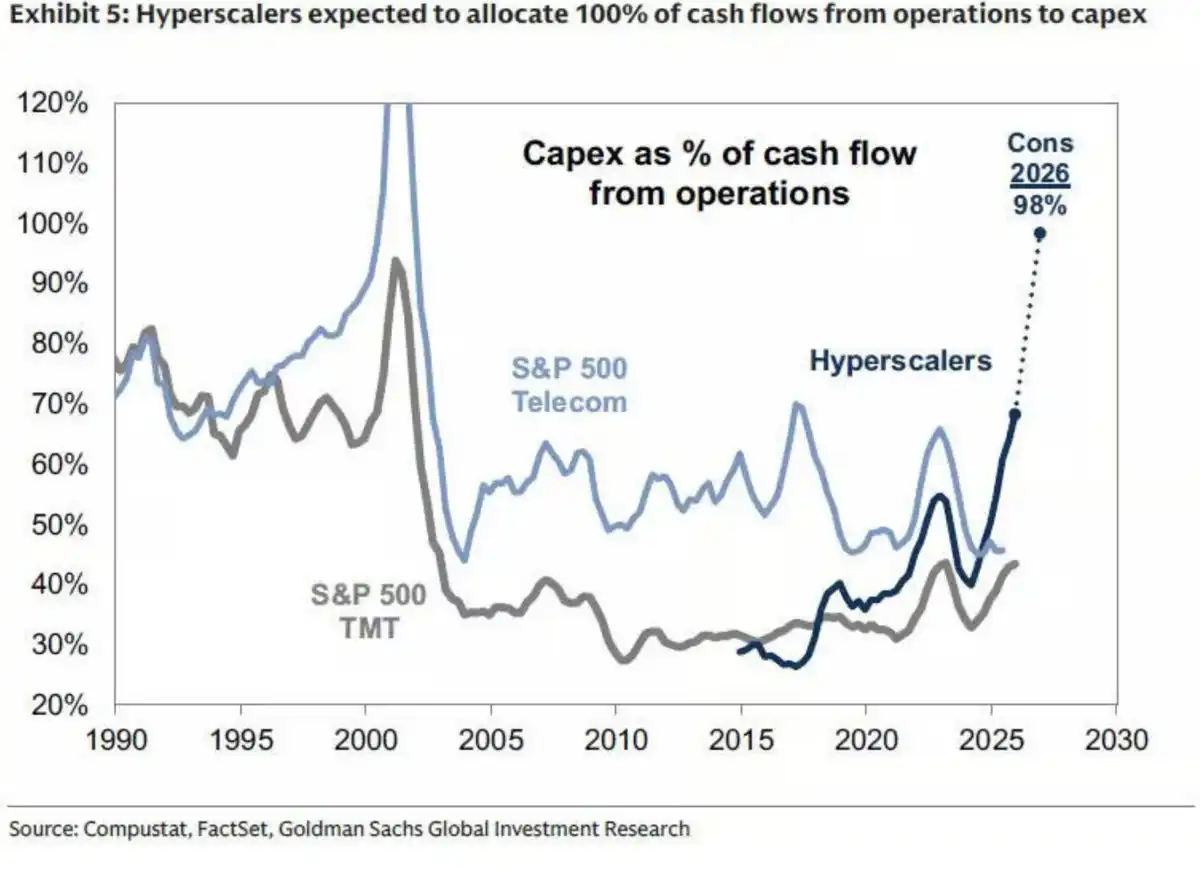

Free Cash Flow Bottoming: 98% of Operating Cash Flow Devoured by Capex

Cloud providers have no choice but to continuously issue equity and debt. Google and Meta (hinting they might?) are doing it, Amazon may follow soon.

Free cash flow is drying up fast. Cloud providers are putting 98% of their operating cash flow into capital expenditures. This is the highest level since the dot-com bubble.

Chart source: Goldman Sachs

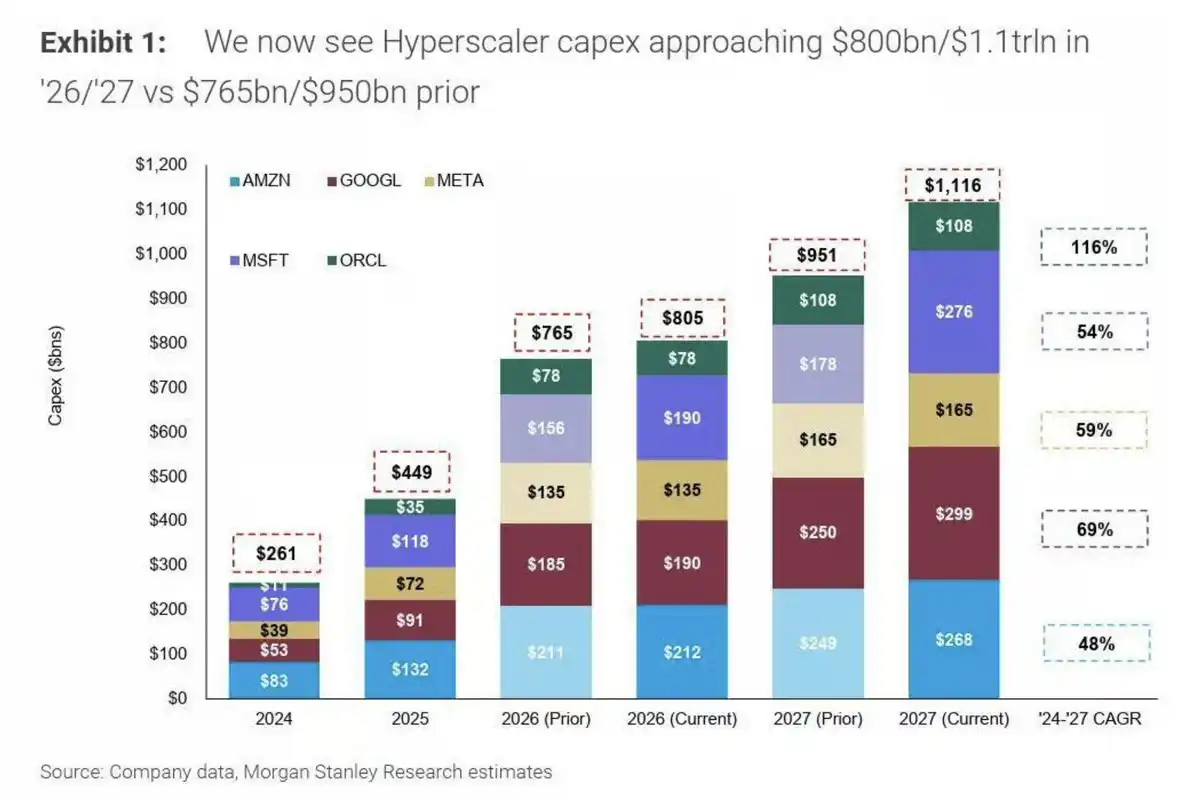

Meanwhile, Morgan Stanley forecasts robust capital expenditure of ~$1.1 trillion in 2027.

Chart source: Morgan Stanley

Do the math: ~40% of that, roughly $440 billion, goes to memory. That's essentially the total capital expenditure for all of 2025.

Two things unsettle me:

First, equity and debt financing in the market is already sending negative signals to participants—cash is bottoming, price-to-sales and free cash flow multiples are exploding.

Second, cost pressures could slow capital expenditure growth, even halt it earlier than expected. By my estimate, around mid-2027, earnings calls will start showing signs of pulling back.

I believe the second point will start approaching memory manufacturers by end-2026, much earlier than many anticipate.

From then on, the number one question repeated on earnings calls will be component pricing—especially memory—and how it's squeezing spending budgets. I don't believe cloud providers will ignore this and continue ramping capital expenditure without reservation.

That's just my view.

Chipmakers Are Already Looking to Save on Memory

AMD, NVIDIA, Google are already moving towards memory optimization.

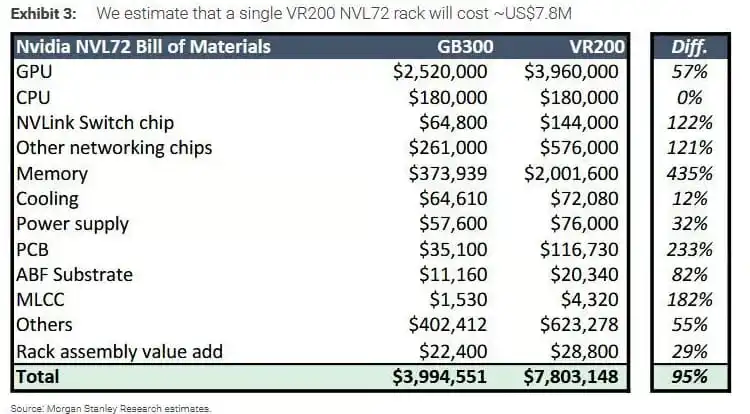

The CPU-side SOCAMM DRAM in NVIDIA's next-gen Rubin NVL72 rack could be cut from ~55TB per rack to ~28TB, nearly halved. This makes sense, as the VR200 bill of materials shows memory costs rising 435% compared to GB300.

Chart source: Morgan Stanley

SOCAMM isn't HBM, but the cost pressure driving cost-saving ideas is the same principle—whether it's AMD using MEXT for memory pooling (making flash behave like DRAM) or directly cutting SOCAMM DRAM.

Chipmakers have even fewer choices: they're already paying for HBM, and then adding SOCAMM costs on top? It hurts. Getting hit from both sides.

Memory is Still Cyclical, Inflection Point Mid-2027

Finally, on memory's cyclicality.

I disagree with the notion that "memory no longer has cycles."

Even if I'm completely wrong and capital expenditure remains strong for a decade, you'll still naturally hit boom-and-bust cycles. Those arguing against me must assume memory demand grows yearly and cloud provider spending never enters a cycle—that's simply impossible.

Chart source: SEMI

These manufacturers rushing to expand are betting on sustained capital expenditure growth (unlikely at this pace) and continued strong memory demand (which in turn relies on sustained capital expenditure growth).

My projection is that DRAM pricing peaks starting in 2027:

SK Hynix gross margin ~80%; Micron ~78-80%; Samsung ~70-75%.

The price curve flattens while capacity remains tight, around February or March. Then, around mid-2027, you'll sense signals of slowing or even paused capital expenditure growth.

I believe most memory stocks start giving back gains from this point, as investors price in the impending margin contraction.

By 2028, more capacity comes online (supply still tight), but demand expectations weaken, margins continue sliding to the low 60%s. From 2028 to 2030, capacity continues coming online, supply tightness eases, and capital expenditure sees no substantial growth. I predict the real crash happens in this phase, with significant stock price gains reversed starting end-2027.

Everyone believes memory will be strong until end-2030. My forecast is margin contraction starts mid-2027, and gains in many memory stocks reverse.

That said, if in 2027 cloud providers say 2028 capital expenditure will be significantly stronger, this article is worthless, and I'll look like a fool. Time will tell right or wrong, but I believe this is the path memory takes next.

Why I'm Not So Optimistic

My reasons for being less optimistic about memory than others are few:

Memory manufacturers are too greedy on margins; I believe memory remains cyclical, the "no-cycle" theory bets entirely on capital expenditure never entering a cycle; chipmakers finding ways to save memory itself proves they're fed up with high costs; CFOs' cash is almost 100% exhausted by capex, with memory taking 40% of costs in 2027, further debt/equity issuance becomes untenable.

The only good outcome is a sudden, massive wave of supply dumping crashing prices for the three manufacturers. In that case, the same capital expenditure would buy more output.