Despite popular belief, Bitcoin’s [BTC] recent price decline was not because of the miners.

Instead, the downturn might be tied to weak demand. So, there are concerns about the market’s ability to absorb supply. With miner selling near lows, the next move will likely depend on whether buying interest returns or not.

Are loss-making miners causing the sell-off?

A common market narrative of recent times is that Bitcoin’s recent weakness has been caused by distressed miners offloading supply. Rising post-halving costs (spanning electricity, hardware, and operations) have allegedly pushed many miners close to or below breakeven, forcing them to sell.

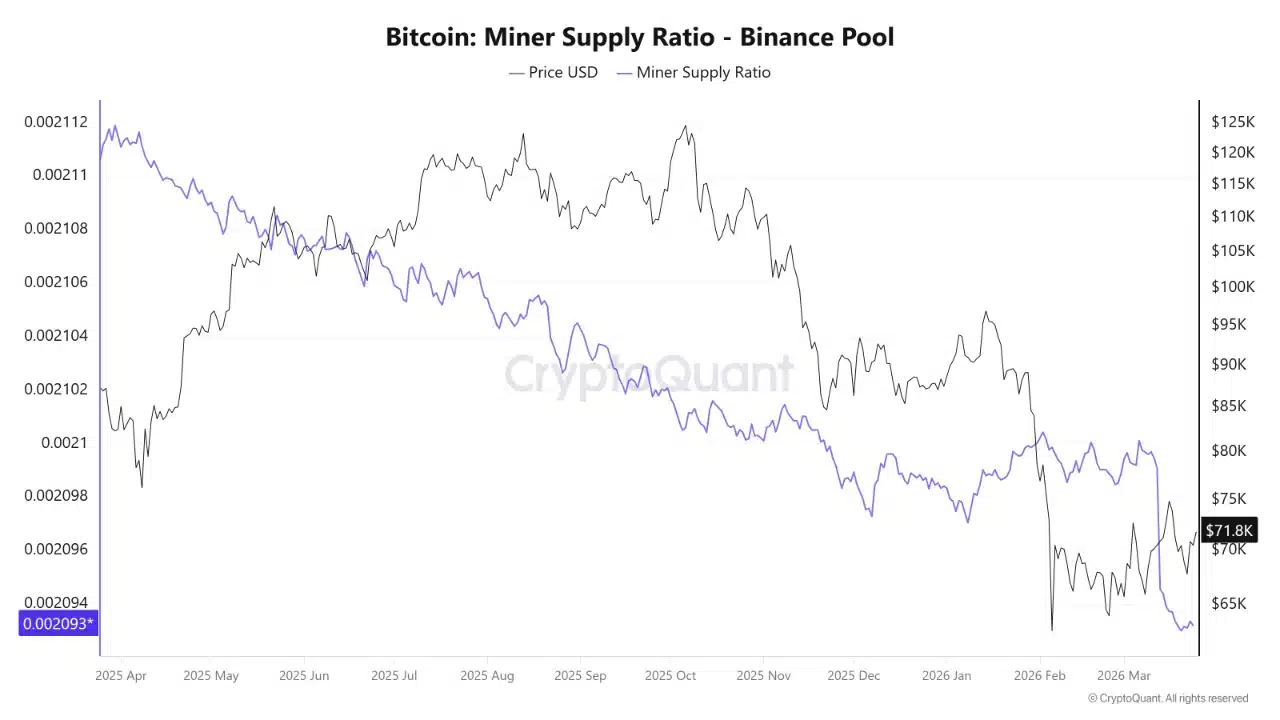

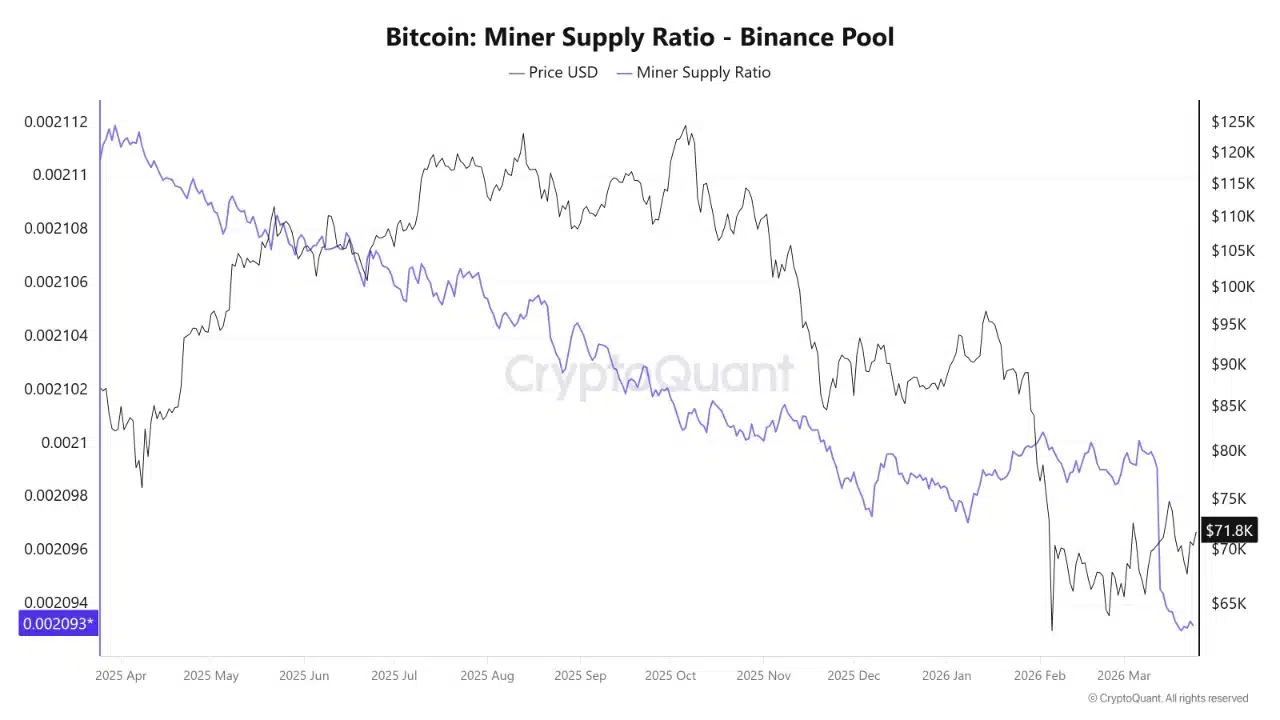

However, here’s a contrarian view. Miner Supply Ratio, which tracks BTC sent from miners to exchanges like Binance, has been steadily falling since early 2025.

Basically, miners are selling less, not more. Even so, Bitcoin’s price first rallied and then dropped during this period.