Author: David, Shenchao TechFlow

At this time last year, a 16GB DDR4 RAM stick cost just over 200 RMB. Now, the same model is priced at 600 RMB, with some models even approaching 700 RMB.

The direct reason for the price increase is a tightening of supply. The three major memory giants have collectively shifted their production capacity towards the AI market. And Micron is the latest to lay its cards on the table.

On January 27, Micron Technology announced a $24 billion (approximately S$31 billion) investment to build an advanced NAND (flash memory) wafer fabrication plant in Singapore. The investment will be phased over 10 years, with shipments starting in the second half of 2028. Singapore's Deputy Prime Minister Gan Kim Yong attended the groundbreaking ceremony.

This is Micron's second major investment in Singapore.

In January 2025, Micron had already begun construction on a $7 billion HBM (High Bandwidth Memory) advanced packaging facility within the same campus, scheduled for production in 2027. Combined, these two projects represent over $30 billion in new investments by Micron in Singapore.

Image source: Lianhe Zaobao, photo by Tang Jiahong

Yet, this is the same company that just two months ago announced the shutdown of its 29-year-old Crucial consumer brand—the memory sticks and solid-state drives you can buy on JD.com and Taobao.

On one hand, spending billions to build factories; on the other, cutting the consumer business. Both point to the same clue: the demand for memory from AI remains high.

Capacity Reallocation After China Market Contraction

Micron's increased investment in Singapore has a clear geopolitical background.

In May 2023, China's Cyberspace Administration announced that Micron's products had not passed the cybersecurity review and required domestic critical information infrastructure operators to stop procurement. In 2018, the Chinese mainland market contributed 58% of Micron's revenue (approximately $17.36 billion); by fiscal year 2022, this had fallen to 10.8% (approximately $3.31 billion).

Production capacity needs a new outlet.

Currently, Micron already has three 3D NAND fabrication plants and several packaging and testing facilities in Singapore, employing about 9,000 people and producing 98% of Micron's flash memory chips.

Micron stated in its latest announcement that the HBM factory is expected to make a significant contribution to supply by 2027 and mentioned that as HBM becomes part of the Singapore manufacturing operations, "synergistic effects" in both NAND and DRAM (Dynamic Random-Access Memory, the common memory chips) production are anticipated.

But the priority of this "synergy" is clear: HBM capacity for 2026 is completely sold out, data center customer demand cannot be fully met, and the consumer brand is being shut down simultaneously.

Within the same campus, consumer-grade production lines are making way for AI production lines.

The Business Logic of Exiting the Consumer Market

On December 3, 2025, Micron announced via its official website a complete exit from the Crucial consumer business, including the sales of RAM sticks and SSD (Solid State Drive) products through global retailers, e-commerce platforms, and distributors.

Shipments will continue until the end of February 2026, at which point this brand, founded in 1996, will bid farewell to the retail market.

In the statement, Micron's Executive Vice President, Sadana, stated that the surge in memory and storage demand driven by AI in data centers prompted Micron to make the "difficult decision" to exit the Crucial consumer business in order to more effectively supply and support large strategic customers in high-growth areas.

Data supports this judgment.

Micron's fiscal year 2025 third-quarter HBM product income reached $1.98 billion, with an annualized revenue close to $8 billion. According to TrendForce data, the unit price of HBM memory required for AI servers is about 8 times that of ordinary servers.

Micron predicts the HBM market size will grow from approximately $35 billion in 2025 to about $100 billion in 2028, by which time it will exceed the size of the entire DRAM market in 2024.

In contrast, consumer-grade storage is a business with thin profits and fierce competition.

Micron's exit means the world's major consumer DRAM manufacturers are reduced from three—Samsung, SK Hynix, Micron—to two.

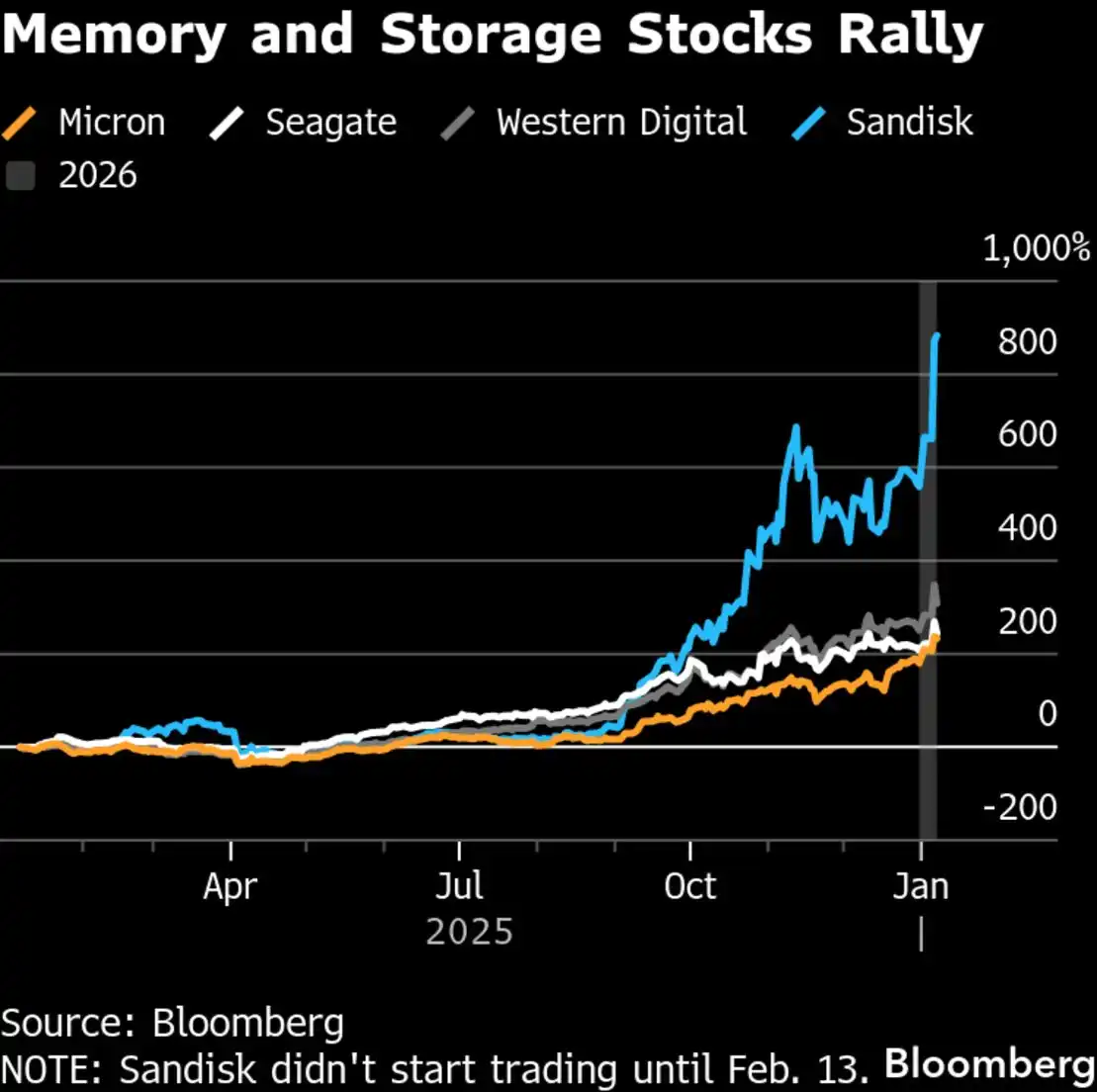

The AI Rally of Memory Stocks

The capital market has already priced in this shift.

According to statistics from *National Business Daily*, memory stocks occupied the top four spots on the U.S. stock gainers list for the full year 2025:

SanDisk rose 577%, becoming the S&P 500's top performer for the year; Western Digital rose 281%; Micron rose 236%; Seagate rose 216%.

For comparison, Nvidia rose 39% in the same period, ranking 71st.

It was reported that tech giants like Google and Amazon presented Micron with "unlimited purchase demands" in October 2025. Micron CEO Mehrotra revealed on an earnings call that the company's entire HBM supply for 2026 is already sold out, and currently, it can only meet half to two-thirds of the demand from key customers.

Micron's latest financial report shows revenue of $13.6 billion for September-November 2025, a year-on-year increase of 57%, with DRAM revenue of $10.8 billion, up 69% year-on-year.

Consumer Side: Price Hikes May Continue

Samsung, SK Hynix, and Micron had all previously announced plans to gradually phase out DDR4 production from late 2025 to early 2026. Micron issued an end-of-life notice for DDR4/LPDDR4 in June.

Although Samsung and SK Hynix later extended their DDR4 production plans to the end of 2026 due to soaring DDR4 prices, the overall trend of tightening supply remains unchanged.

The price reaction has been intense. According to TrendForce data, since 2025, the spot price of DDR5 memory chips has risen over 300%, while DDR4 has risen over 150%. DDR4 has even seen a "price inversion," with the price of some specifications exceeding that of DDR5.

ADATA Chairman Chen Libai also publicly stated that the comprehensive shortage and price increase across the four major storage categories—DRAM, NAND, SSD, HDD—is a situation he is witnessing for the first time in over thirty years in the industry.

If you want to add memory to your old computer or build a new desktop, the cost remains high. Because AI needs computing power, and computing power needs memory. Your old computer is probably still behind AI demand in the queue.

Memory stocks have risen, and memory stick prices have risen too.

One is an investment opportunity; the other is paying the bill for that opportunity.