Kraken parent Payward has partnered with Nasdaq to build what the companies describe as an “equities transformation gateway,” a new infrastructure layer designed to connect regulated tokenized equity markets with permissionless blockchain networks. For crypto markets, the significance is clear: one of the largest traditional market operators is now working directly with a crypto-native tokenization framework to move equities between institutional rails and DeFi environments.

The partnership centers on xStocks, Kraken’s tokenized equities product, which Payward said has surpassed $25 billion in total transaction volume less than a year after launch. More than $4 billion of that volume has been settled on-chain, and the framework now counts over 85,000 unique holders across supported networks, giving Kraken a sizable footprint as tokenized stocks move from concept toward market structure.

Nasdaq And Kraken Join Forces

Under the proposed setup, xStocks will power the permissionless infrastructure layer for Nasdaq’s upcoming issuer-sponsored equity token design. That design, which Nasdaq expects to become operational starting in the first half of 2027, is meant to preserve issuer control, existing regulatory frameworks, and the rights attached to the underlying shares while still allowing those assets to interact with blockchain-based financial systems.

In practical terms, the gateway is supposed to let eligible users swap tokenized equities between a regulated, permissioned market environment and open on-chain ecosystems. Payward said this would allow assets to move “fluidly” between institutional trading infrastructure and decentralized financial networks, while Payward Services handles KYC and AML onboarding for participants accessing the bridge through Kraken.

Arjun Sethi, co-CEO of Payward and Kraken, framed the effort as a structural change to how equities can be used once they are placed on programmable rails. “Tokenization upgrades market infrastructure at the asset layer by allowing equities to exist as programmable financial instruments that can operate across both regulated capital markets and open blockchain networks,” he said. “Today most equities sit inside brokerage systems where their utility is largely limited to directional exposure and, in some cases, broker-specific margin arrangements.”

He argued that the current model leaves capital trapped inside siloed venues. “That structure fragments liquidity across venues and leaves a meaningful amount of capital static relative to its potential utility,” Sethi said. “With xStocks, our goal is to make equities natively interoperable across trading venues, financial applications and blockchain networks while preserving issuer rights, regulatory protections and price integrity.”

Sethi went further, tying tokenized equities to a broader capital-efficiency thesis that will be familiar to crypto derivatives traders. “Bringing equities onto programmable infrastructure expands how they can function within a portfolio,” he said. “Instead of simply representing exposure to a company, tokenized equities can operate as collateral within unified trading systems that support spot markets, cross-margin trading, derivatives, perpetual futures, and financing environments.”

That point sits at the heart of the announcement. Payward is not pitching tokenized stocks merely as wrappers for traditional shares, but as collateral that can move across trading, lending and hedging systems under a unified margin framework. In jurisdictions where xStocks are already available, Payward will also serve for an initial period as the primary settlement layer for transactions tied to Nasdaq’s equity token design.

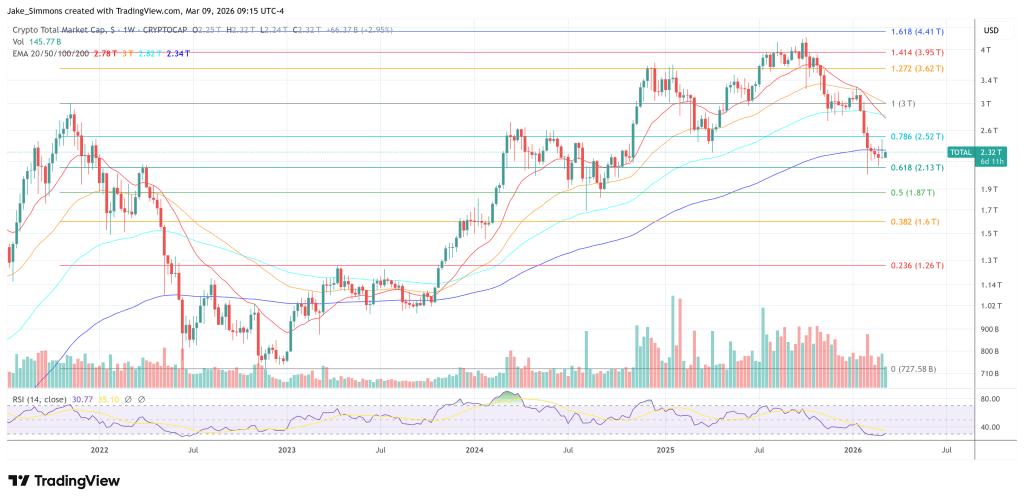

At press time, the total crypto market cap stood at $2.32 trillion.