On April 8, Hyperliquid's native protocol Hyperbeat launched Liquid Banking, a self-custodied 'bank' deployed on HyperEVM, integrating stablecoin deposits, VISA card spending, perpetual contract trading, and multi-currency fiat on/off ramps into a single on-chain smart wallet.

The Hyperbeat team transitioned from being among the first validators on the Hyperliquid testnet. Initially just 5 people, they self-funded a start with approximately $200,000. The two co-founders, Kilian Boshoff(@Fundi_Crypto) and 800.HL(@degennQuant), maintain a low profile; the former has a background from Stellenbosch University in South Africa. The company is registered in the Cayman Islands.

In August 2025, it completed a $5.2 million seed round co-led by ether.fi Ventures and Electric Capital, with participation from Coinbase Ventures, Maelstrom, Anchorage Digital, and others, valuing the company at approximately $40 million.

Morpho Provides the Engine, Building a 'Bank' in Ten Months

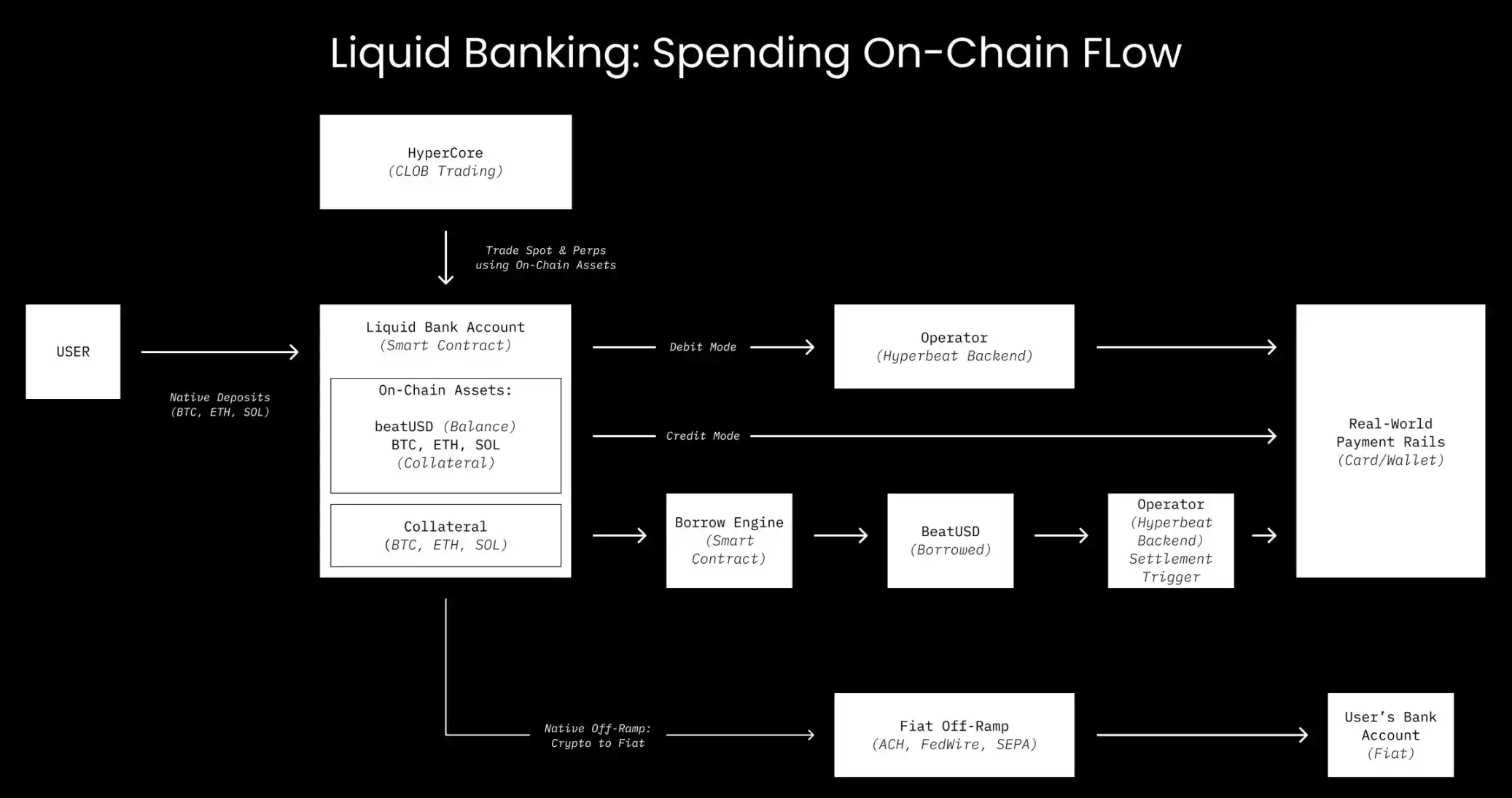

The core selling point of Liquid Banking is Credit Mode.

Users deposit assets like BTC, ETH, HYPE, etc., as collateral. When swiping the VISA card, the system instantly borrows stablecoins through the Morpho Blue market to complete the payment, while the collateral remains on-chain, continuing to generate yield. The user never interacts with a borrowing interface; the act of swiping the card is itself an on-chain loan.

The underlying lending engine comes from Morpho. Hyperbeat integrates Morpho into the user's smart wallet through an on-chain whitelist mechanism. Currently, Credit Mode operates on six isolated markets, with collateral covering HYPE, UBTC, UETH, USOL, and even the gold token XAUT.

Hyperbeat does not touch the core lending logic; Morpho does not touch the user interface. The former builds the 'bank frontend,' the latter supplies the 'credit engine.'

Stablecoin deposits for Liquid Banking center around beatUSD, a native stablecoin issued in partnership with Paxos Labs. Paxos provides the stablecoin infrastructure (underpinned by USDG0). The yield from the reserves flows directly back into Hyperbeat's rewards program and is ultimately distributed to users, rather than remaining with the issuer.

The deposit-side USD+ vault automatically allocates user funds to protocols like Morpho, Hypuur, Hyperlend, Felix, etc., offering 3%-8% APY.

The yield comes from the real borrowing interest paid by Credit Mode consumers. The more spending, the higher the deposit yield. But the sustainability of this cycle depends on the volume of real consumption.

Spend Without Selling Crypto, But Interest Accrues Immediately on Swipe

Fiat on/off ramps for Liquid Banking are provided by Noah, supporting USD (ACH, FedWire) and EUR (SEPA) deposits, with a unique IBAN bound to each account.

In March 2026, direct top-ups and withdrawals for Vietnamese Dong and Malaysian Ringgit were added. Withdrawals also cover over ten currencies including British Pounds, Dirhams, and Thai Baht.

The VISA card is issued by Third National, with underlying infrastructure from Rain, a Visa Principal Member. By early January 2026, Rain's financing round valued it at $1.95 billion, with an annualized processing volume exceeding $3 billion, covering over a hundred countries.

The card tier is Visa Signature,附带机场贵宾厅等权益 (includes benefits like airport lounge access). Foreign currency transactions incur a 1% FX fee (based on Visa's official exchange rate), with no annual fee and no transaction fees; ATM withdrawals cost $1 + 0.65%; the default monthly spending limit is $100,000.

The borrowing利率 (interest rate) for Credit Mode fluctuates with the utilization rate of the Morpho market, but there is no grace period. Every instance of 'spending without selling crypto' starts accruing interest the second the card is swiped.

Hyperbeat's official 'no hidden fees' refers to the transparency of the yield strategy, not the card's fee pricing. The Credit Mode borrowing rate is dynamically determined by the Morpho market. The lack of a grace period means the real-time cost of the convenience of 'spending without selling crypto' exists and is not low.

The Cost of Self-Custody is a One-Day Cooling Period

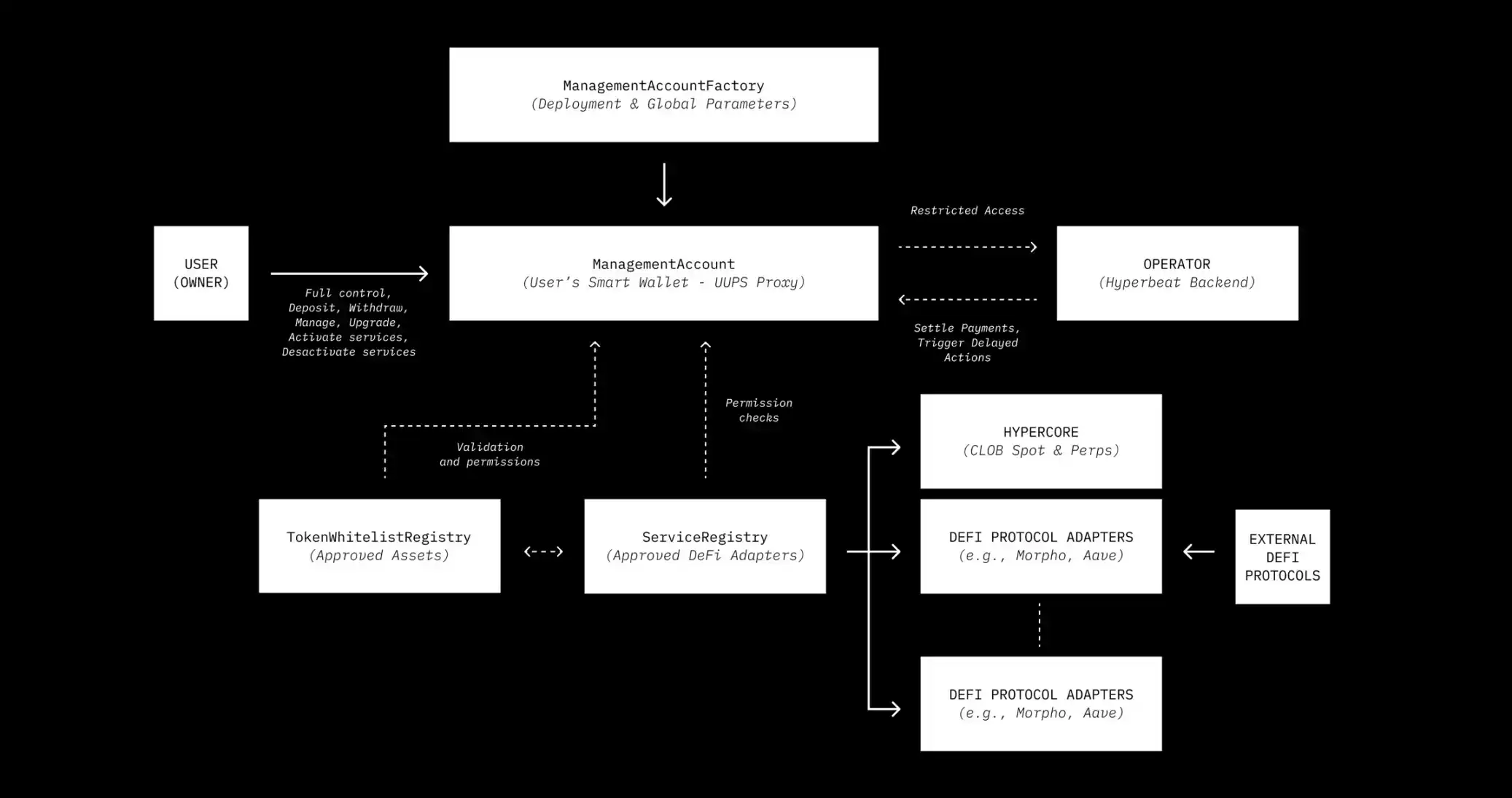

Unlike all centralized crypto cards, user assets always remain in their self-controlled ManagementAccount smart wallet. The Hyperbeat backend only has a restricted Operator role, able to execute settlements only within user-set limits and unable to transfer assets to unauthorized addresses.

But self-custody must solve one problem: what if a user withdraws funds right after swiping the card? Hyperbeat introduces an on-chain timelock mechanism.

Withdrawing settlement tokens requires a cooling period and a confirmation process. Withdrawing collateral requires Operator approval to prevent bad debt. Switching modes also has a delay. The contracts were audited by Zellic and Nethermind, with key management provided by Turnkey.

These frictions are not a bug; they are a feature. They acknowledge the speed difference between on-chain settlement and offline consumption, filling the gap with contract rules rather than 'please believe us.' But users must monitor their health factor themselves; there is no customer service to undo operational mistakes.