Last weekend, Harvard Management Company (HMC) filed its latest 13F holdings report with the U.S. Securities and Exchange Commission. Its holdings in the BlackRock Bitcoin Spot ETF (IBIT) shrank by 43% compared to the previous quarter, while the Ethereum ETF (ETHA) purchased during the same period was completely liquidated.

In just two quarters, Harvard's public holdings in crypto assets fell from a peak of $443 million to about $117 million. As one of the top-tier institutions managing the world's largest university endowment fund, this move has sparked market questioning: Can even top talent escape the trap of buying high and selling low?

In fact, Harvard's connection with cryptocurrency goes far beyond this. As early as 2018, several Ivy League endowment funds showed keen interest in blockchain technology through venture capital funds focused on cryptocurrencies. It was reported that Harvard, Yale, Brown, and the University of Michigan began quietly purchasing Bitcoin through exchanges like Coinbase around 2019.

Among them, HMC first publicly disclosed its holdings in Q2 2025. According to the 13F filing submitted in August of that year, HMC held approximately 1.9 million shares of IBIT, valued at about $117 million, and simultaneously established a position in the Gold ETF (GLD) worth about $102 million.

Matt Hougan, CIO of Bitwise, interpreted this set of operations as a "depreciation hedge trade," simultaneously betting on Bitcoin and gold to hedge against the risk of global currency oversupply. IBIT thus became Harvard's fifth-largest public holding, surpassing its holdings in Alphabet, Google's parent company.

Entering the third quarter, HMC made a significant increase in its position. As of September 30, 2025, its IBIT holdings expanded to approximately 6.81 million shares, valued at about $443 million, a quarter-over-quarter increase of over 257%. IBIT surpassed Microsoft, Amazon, and Nvidia to become the single largest holding in HMC's publicly disclosed portfolio, accounting for about 20% of its public U.S. stock portfolio.

At that time, facing persistently low expected returns from traditional assets, many university endowment funds were quietly adjusting their investment strategies.

Kim Lew, CEO of Columbia Investment Management Company, stated that expected returns and alpha from traditional asset classes would both be compressed, forcing institutions to move further out on the risk curve. Carlos Rangel of the W.K. Kellogg Foundation bluntly said that the traditional foundation model would be difficult to sustain if an 8% return rate couldn't be achieved.

Simultaneously, even Harvard's own economics professors couldn't sit still. In August 2025, Kenneth Rogoff, former IMF Chief Economist and Harvard economics professor, publicly reflected on his mistaken 2018 prediction—he had predicted that Bitcoin was more likely to fall to $100 than rise to $100,000 within a decade, yet at that time, the Bitcoin price had already exceeded $113,000, representing over a 10-fold increase since his prediction.

Rogoff admitted he had been "overly optimistic about the prospects for sensible crypto regulation in the United States" and had underestimated the demand support for Bitcoin in the global underground economy. The public admission of error by such an academic figurehead provided an additional layer of emotional endorsement for this wave of institutional buying. And Bitcoin subsequently approached its historical peak of $126,000 in October 2025.

In Q4 2025, after the market peaked and began to retreat, HMC adjusted its positions accordingly. IBIT holdings decreased by about 21%, falling to approximately 5.35 million shares valued at about $266 million. Simultaneously, the BlackRock Ethereum Spot ETF (ETHA) appeared for the first time in the report, with a holding of about 3.87 million shares valued at approximately $86.8 million.

As disclosed by Bloomberg ETF analyst James Seyffart, hedge funds were net sellers of Ethereum ETFs this quarter due to the collapse of basis trade returns, becoming the largest net sellers. Harvard precisely entered the market against the trend during this time window, becoming the largest new buyer of Ethereum ETFs for the quarter.

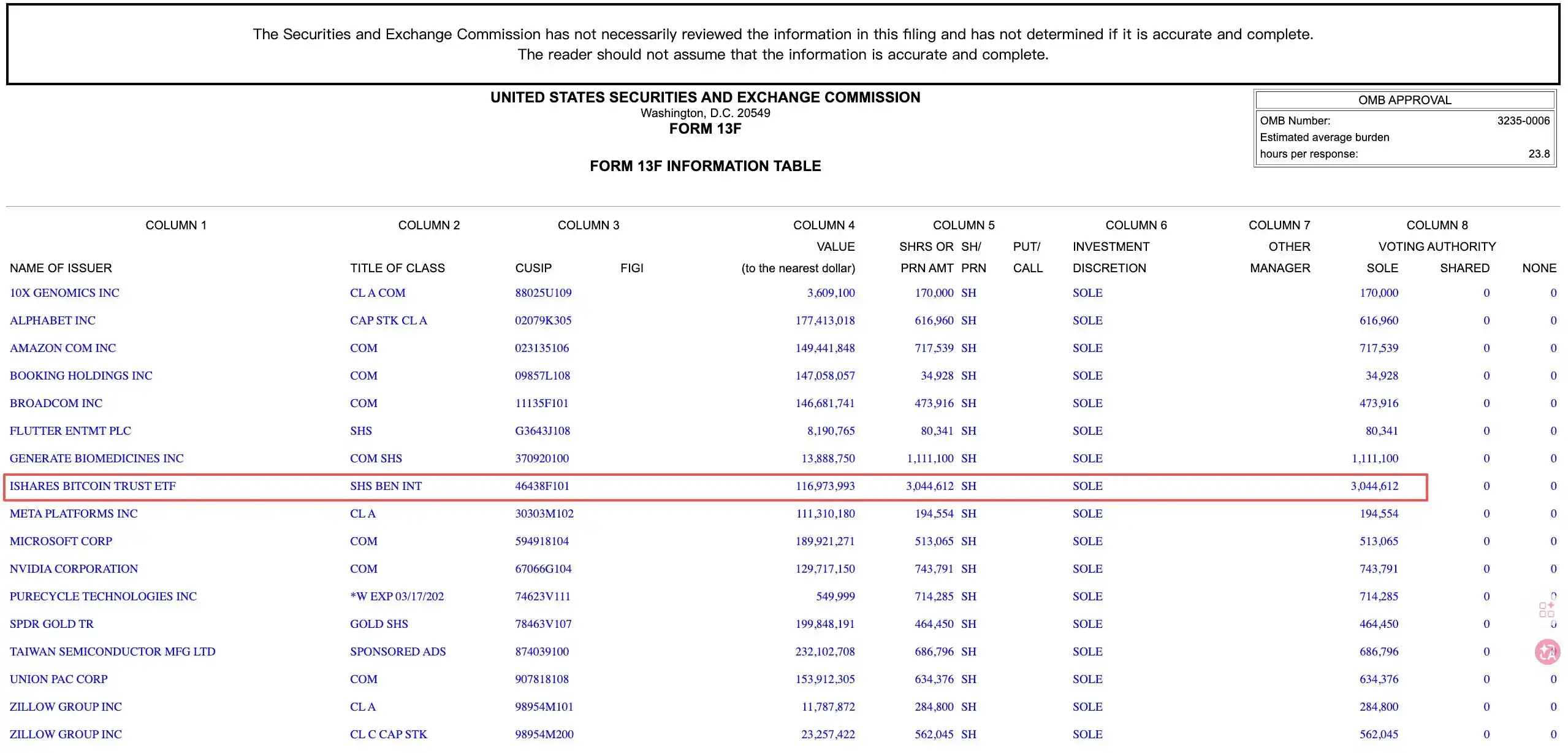

The latest disclosed holdings for Q1 2026 show that ETHA, which had just been established less than a quarter ago, has been completely liquidated. Meanwhile, HMC significantly reduced its IBIT holdings again, cutting its position by about 43%, leaving about 3.04 million shares valued at about $117 million. IBIT has also fallen out of Harvard's top five holdings, surpassed in turn by TSMC, Alphabet, Microsoft, and SPDR Gold Trust.

According to estimates by well-known crypto KOL Chen Jian, HMC's average purchase price for IBIT was around $110,000, with an average selling price of about $80,000, resulting in a loss of approximately 28%, with a paper loss on the Bitcoin portion exceeding $100 million. Regarding Ethereum, the average purchase price for ETHA was about $4,000, and it was liquidated at around $2,600, estimated to incur a single-quarter loss of over $30 million (-35%). Combined, these crypto operations are suspected to have resulted in losses exceeding $150 million.

Is this chasing rallies and selling on dips, or routine institutional rebalancing?

One perspective argues that HMC made its largest-scale increase in position when Bitcoin was near its historical high, then sold more as it fell lower, drawing a classic curve of buying high and selling low. The Ethereum position was even completely liquidated less than a quarter after purchase, almost capturing the entire decline. This is typical behavior of chasing rallies and selling on dips.

Another perspective points out that by the end of Q3, IBIT already accounted for 20% of HMC's public portfolio, a clearly excessive concentration. Subsequent reductions were necessary actions from a risk control standpoint. Moreover, HMC still maintains a base position of about $117 million in IBIT, indicating it hasn't completely exited the market.

However, this round of position reduction must also consider the current real-world pressures Harvard is facing.

Last October, Harvard's financial report for fiscal year 2025 showed that due to the Trump administration halting almost all federal research funding in the spring, Harvard incurred an annual operating loss of $113 million on total revenue of $6.7 billion, marking the first budget deficit since the pandemic.This deficit represents 1.7% of total revenue, with the operating shortfall standing in stark contrast to the $45 million surplus in 2024.

The endowment fund contributes about 37% of Harvard's operating income. In fiscal 2025, it provided approximately $2.5 billion in spending support, but 80% of these funds are restricted by donor purposes and cannot be reallocated at will.

Simultaneously, the Republican tax bill formally signed into effect in July 2025 significantly raised the maximum tax rate on endowment income from 1.4% to 8%. Harvard estimates this will result in an additional annual tax burden of approximately $300 million.

Under such pressure, the asset structure itself determines where cuts are easiest to make.

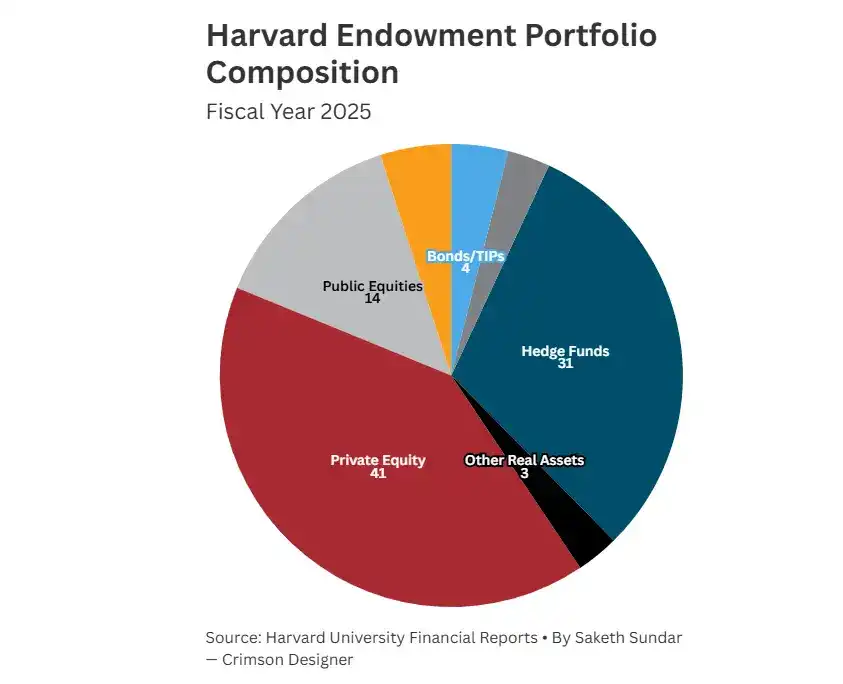

Private equity accounts for about 41% of Harvard's endowment fund, and hedge funds about 31%. These assets have long lock-up periods and extremely high costs for discounted sales. IBIT and ETHA, as intraday-tradable public market ETFs, offer the strongest liquidity and lowest liquidation costs, naturally making them the first targets for adjustment.

Furthermore, N.P. Narvekar, the current CEO of HMC, has revealed plans to retire around 2027 and is currently discussing succession arrangements with the board. In an environment where fiscal pressure, political uncertainty, and leadership transition overlap, holding a large-scale, highly volatile crypto position becomes an additional reputational risk.

In contrast to Harvard's retreat are the distinctly different choices of other institutions. Among them, the Abu Dhabi sovereign fund Mubadala continued to increase its IBIT holdings by about 16% in Q1 2026, raising its position to about $566 million, marking its fifth consecutive quarter of increasing its Bitcoin ETF stake.

As another university endowment fund, Dartmouth maintained its IBIT position unchanged, swapped its Ethereum ETF for a staking version, and added approximately $3.67 million in the Bitwise Solana Staking ETF, becoming one of the first U.S. university endowment funds to extend its crypto allocation beyond Bitcoin and Ethereum.

Brown University kept its 212,500 IBIT shares unchanged, while Emory University exited its small IBIT position, instead increasing its holdings in the Grayscale Bitcoin Mini Trust.

Overall, Harvard's round of operations is the result of the combined effects of fiscal pressure, liquidity needs, and triggered risk budgets, making it difficult to simply attribute it to chasing rallies and selling on dips.

When the world's top university endowment fund enters the crypto market, it does not do so with a crypto-native belief-based approach, but rather with Wall Street's risk-ledger logic. Crypto ETF products certainly provide an institutional entry point, but they also bring institutional-style selling pressure during risk-off periods.