Written by: Suvashree Ghosh, Matt Haldane

Compiled by: Saoirse, Foresight News

Not long ago, the crypto industry was chanting the slogan "blockchain, not Bitcoin," claiming that distributed ledger technology would go beyond financial applications and completely reshape the internet. However, recent financing trends indicate that in the real world, cash is still king.

Since the Web3 and NFT craze subsided in the early 2020s, investment enthusiasm in the crypto industry has noticeably cooled. But one niche has bucked the trend, attracting increasing venture capital—stablecoin payments.

Stripe's acquisition of Bridge for $1.1 billion last year was an early signal of traditional financial institutions beginning to lay out stablecoin payments. Since then, a batch of startups including ARQ, KAST, and RedotPay have successively secured new funding to build cross-border payment channels and stablecoin-based financial services. Mastercard's acquisition of BVNK for $1.8 billion last week further confirms the market's strong interest in this sector.

"Startups related to stablecoins are almost the hottest area for venture capital financing right now," said Rob Hadick, General Partner at Dragonfly Capital. "Stablecoins have broken away from the entire crypto industry to become one of the few truly breakthrough applications with widespread real-world adoption."

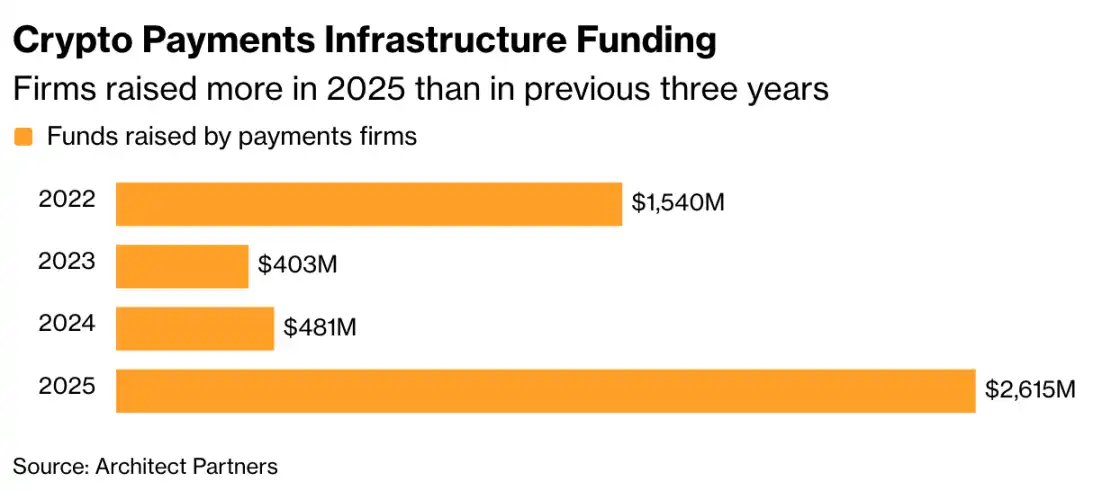

According to data from Architect Partners, which specializes in annual crypto financing reports, the total financing for crypto payment companies soared to $2.6 billion in 2025, exceeding the sum of the previous three years. Driven by Mastercard's acquisition of BVNK, this number is expected to continue climbing this year.

Crypto Payment Infrastructure Financing: 2025 company financing exceeded the sum of the previous three years

Meanwhile, overall private financing in the crypto industry increased from nearly $13 billion in 2024 to $20.4 billion in 2025, but still fell short of the 2022 peak of $27.6 billion.

Total Financing for Cryptocurrency Companies: The number of crypto financing deals rose last year but still hasn't reached the 2022 peak

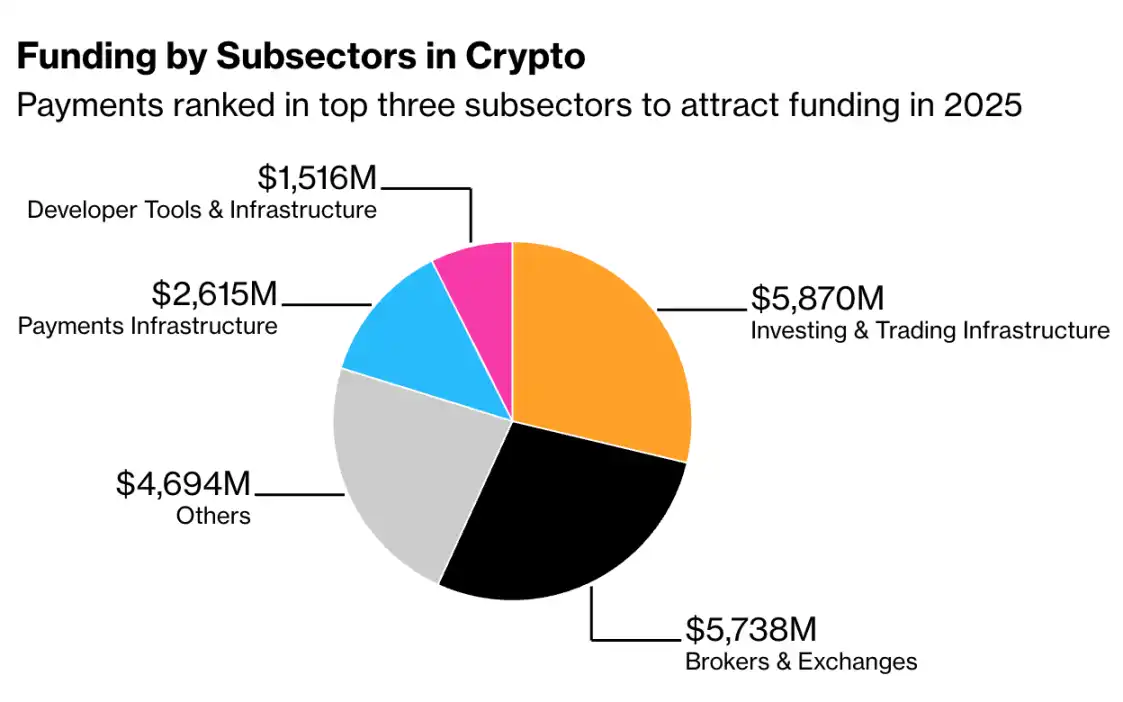

Currently, the two areas with the most concentrated private funding are "Investment & Trading Infrastructure" and "Brokers & Exchanges," both financial application businesses. Payment infrastructure firmly holds third place. In stark contrast, the blockchain gaming sector, which was once at the core of the Web3 and NFT frenzy, saw its financing drop from $3.76 billion in 2022 (about 14% of total financing) to the point where it was no longer listed as a separate category in 2025.

In fact, various types of decentralized applications (Web3 functional layer) collectively raised $5.2 billion in 2022; in the 2025 report, only the consumer DApp category remained, with financing of just $864 million.

Financing by Cryptocurrency Subsector: Payments跻身 among the top three sub-sectors attracting financing in 2025

Stablecoins are building more robust financial infrastructure for blockchain. These tokens are typically pegged 1:1 to the US dollar, with their value tied to underlying assets. Driven by the Trump administration's pro-crypto policies, market enthusiasm for stablecoins reached unprecedented heights last year.

According to Artemis Analytics data, the total transaction volume of stablecoins surged 72% in 2025, reaching $33 trillion. The two largest stablecoins by size are currently Tether's USDT and Circle's USDC.

Circle's stock price recorded its largest-ever drop on Tuesday as investors assessed potential adjustments to U.S. stablecoin regulations and the impact of intensifying industry competition. But the core appeal of stablecoins remains clear: transferring funds as efficiently as possible.

Cross-border payments remain slow, costly, and capital-intensive. Despite years of fintech development, cross-border transfers still heavily rely on prefunded accounts in different jurisdictions.

"Stablecoins have completely changed this landscape," said Prajit Nanu, co-founder and CEO of cross-border payments company Nium. "They enable value to move globally in real-time without the same level of capital efficiency drain, which is why investors see them as the core infrastructure for the next generation of payments."

This industry still has powerful "gatekeepers." Large payment networks like Visa and Mastercard control access to payment terminals. Eric F. Risley, founder and managing partner of Architect Partners, wrote in the report that the channel distribution issue "is a major concern for every stablecoin and related payment company."

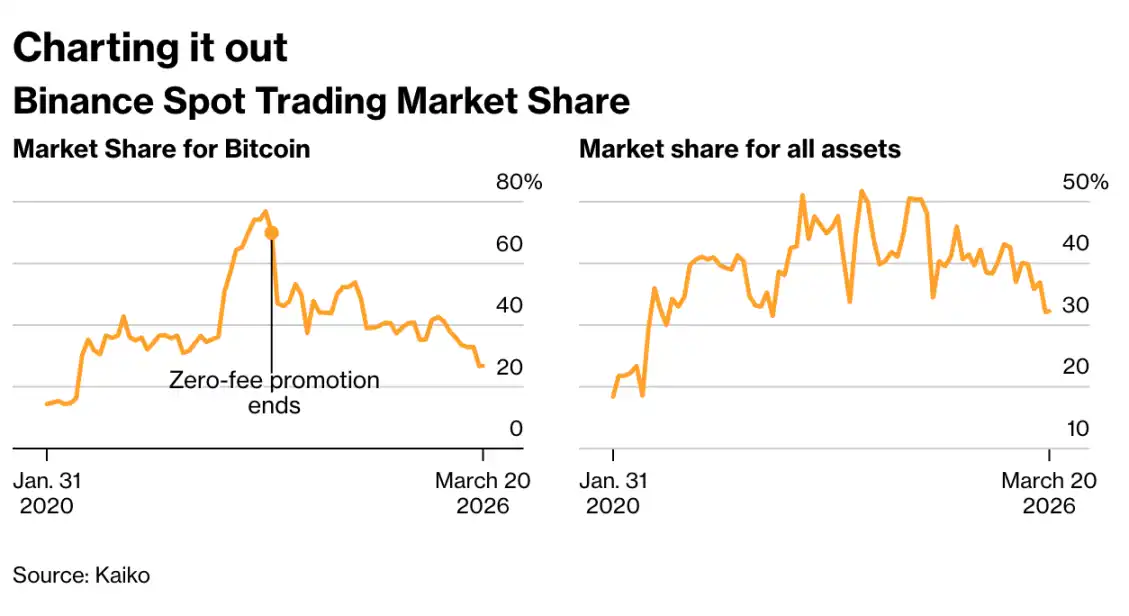

Binance Spot Trading Market Share Trend Chart

As of February this year, Binance's share of Bitcoin spot trading had fallen to 27% (this data varies slightly depending on the statistical method), and its share of all cryptocurrency trading fell from 52% to 32%. Its most profitable derivatives business also saw a significant decline, dropping to 34%.

Franklin Templeton partnered with Ondo Finance to launch an ETF tokenization product, tradable via crypto wallets 24/7, bypassing the broker accounts and limited trading hours that fund investments have relied on for decades.

Industry Voices

"The irony of holding this event in Las Vegas right now is just palpable," said Ben Johnson, Head of Client Solutions at Morningstar, stating bluntly that this industry has "completely crossed the line between investing and gambling, with no room for turning back."

ETFs, originally created to simplify investing, have now become a vehicle for the newest form of financial gambling in the U.S. Bloomberg Intelligence data shows that 36% of the 1,000 new funds launched last year were leveraged products or crypto-related funds.