Author: DFarm

First, let's sort out the recent timeline of events related to Polymarket's transaction fees.

-

Polymarket suddenly announced that it would charge a transaction fee for 15-minute cryptocurrency price prediction markets, but all fees collected would be rebated to market makers (those placing limit orders).

-

The fee rebate was changed from a 100% rebate to a partial rebate.

-

Until the 11th, the 100% fee rebate stopped. From the 12th to the 18th, 20% of the fees are being rebated.

Why Charge a Fee?

We all know that Polymarket previously did not charge any fees for basic transactions. Why did it specifically start charging fees on the 15-minute cryptocurrency markets this time?

This requires explaining what "latency arbitrage" bots are.

In very short-cycle markets like 15-minute intervals, outcomes are determined based on prices from major exchanges.

In the absence of fees, high-frequency trading bots exploit millisecond-level time delays to place orders on Polymarket before its price has had a chance to update, thereby securing profits.

For example, suppose the current probability for BTC going UP in the next 15 minutes on Polymarket is 90%. Suddenly, the BTC price on exchanges drops by 5%. A bot detects this and immediately buys the cheap DOWN shares. After it finishes buying, subsequent bots or traders come in to buy and drive the price, allowing the initial bot to profit and exit.

What is the consequence of this behavior? Market makers consistently get exploited by these high-frequency bots. Naturally, market makers become unwilling to continue providing liquidity by placing orders in these markets, ultimately leading to poorer liquidity in the 15-minute cryptocurrency markets.

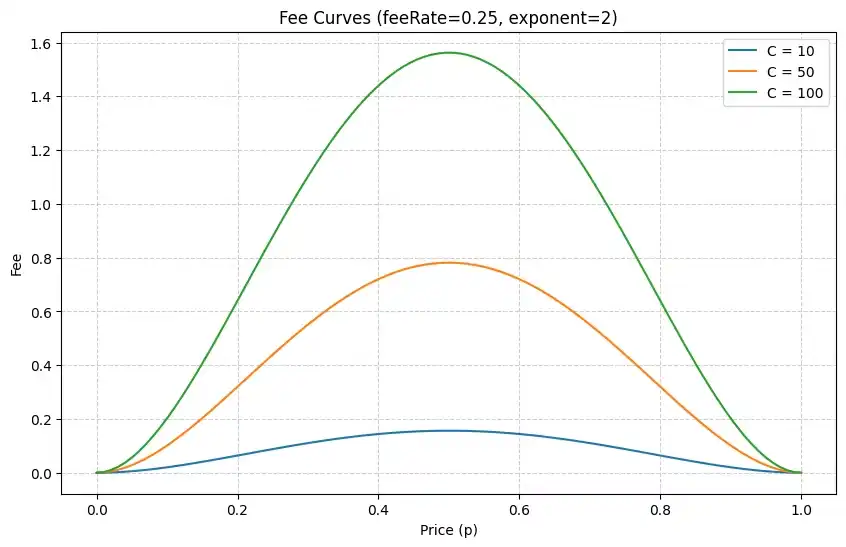

Therefore, the platform introduced a fee mechanism, with the highest fees specifically applied when the odds are 50:50 (as shown in the image). This directly makes the arbitrage cost for many bots higher than their potential profit, so these bots naturally shut down.

Why Subsidize Market Makers?

As mentioned earlier, market makers had too much capital extracted from them previously. To retain market makers, the platform distributes the collected fees to those placing limit orders (market makers).

So why was the rebate reduced from 100% to 20%?

The detail is in this phrase: "From the 12th to the 18th, 20% of fees are rebated." This tells us that the rebate percentage after the 18th is to be determined.

When fees were first introduced, market makers were actually uncertain—they didn't know if the fees would effectively block the bots. The platform initially rebated 100% of the fees to market makers to cover their risks and retain liquidity.

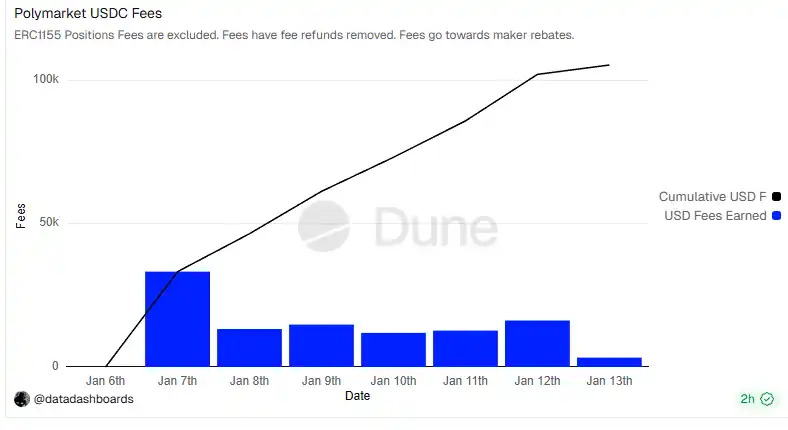

Why only 20% now? Let's look at the data first:

After fees were enabled, the total fee volume halved. What does this indicate? It confirms that many high-frequency bots indeed shut down.

Seeing that the bots are gone and the risk for market makers has decreased, the platform likely concluded that a 100% fee rebate is no longer necessary. They are trying 20% first to see the data performance.

This is why they are trialing a 20% fee rebate for one week first, to observe the data before deciding on the subsequent rebate ratio.

Ultimately, all this is about balancing the interests of market makers, bots, and regular traders.

The "Money Printer" Bots

There are many "money printer" entities present across various markets on Polymarket. Very few people in the market truly understand how they operate.

A very popular example is a post by X user: @the_smart_ape:

This post has nearly 2 million views. Many friends have tried the strategy described in the article, and indeed some have made profits.

But just a few days later, the fees were introduced, and many friends could no longer profit...

So have the "money printers" disappeared? Not entirely. Interested friends can check out these "money printers":

https://polymarket.com/@gabagool22?via=dfarm

https://polymarket.com/@distinct-baguette?via=dfarm

https://polymarket.com/@livebreathevolatility?via=dfarm

If you can decipher their strategies, your "money printer" isn't far away. But remember, don't tell anyone else—though you can secretly tell me.

Finally

Actually, on Polymarket, since there are no third-party commissions or fees, we are essentially betting against each other. Therefore, the platform's responsibility is to provide a fair playing field for both sides.

Players who enjoy PVP games also know that absolute fairness doesn't exist; it can only be approached through iterative version updates, striving for relative fairness.

This situation also shows us that "money printers" do exist on Polymarket, and it's all about competing on technology and strategy.

If this article was helpful to you, please help share it. Thank you.

If you are a newbie to Polymarket, be sure to check out this article → 《Beginner's Tutorial: Hand-Holding Guide to Getting Started with Polymarket from Scratch (Includes Anti-Ban + Low-Friction Deposit/Withdrawal Strategies)》