Author: Nancy, PANews

From the former "investment风向标" to the current "fear of VCs," crypto venture capital is undergoing a necessary process of demystification and clearing.

The darkest moment is also the moment of rebirth. This brutal process of defoaming is forcing the crypto market to establish healthier and more sustainable valuation logic, while also driving the industry back to rational construction and maturity.

The Fall of Star VCs: The Demystification Moment of Elite Glory

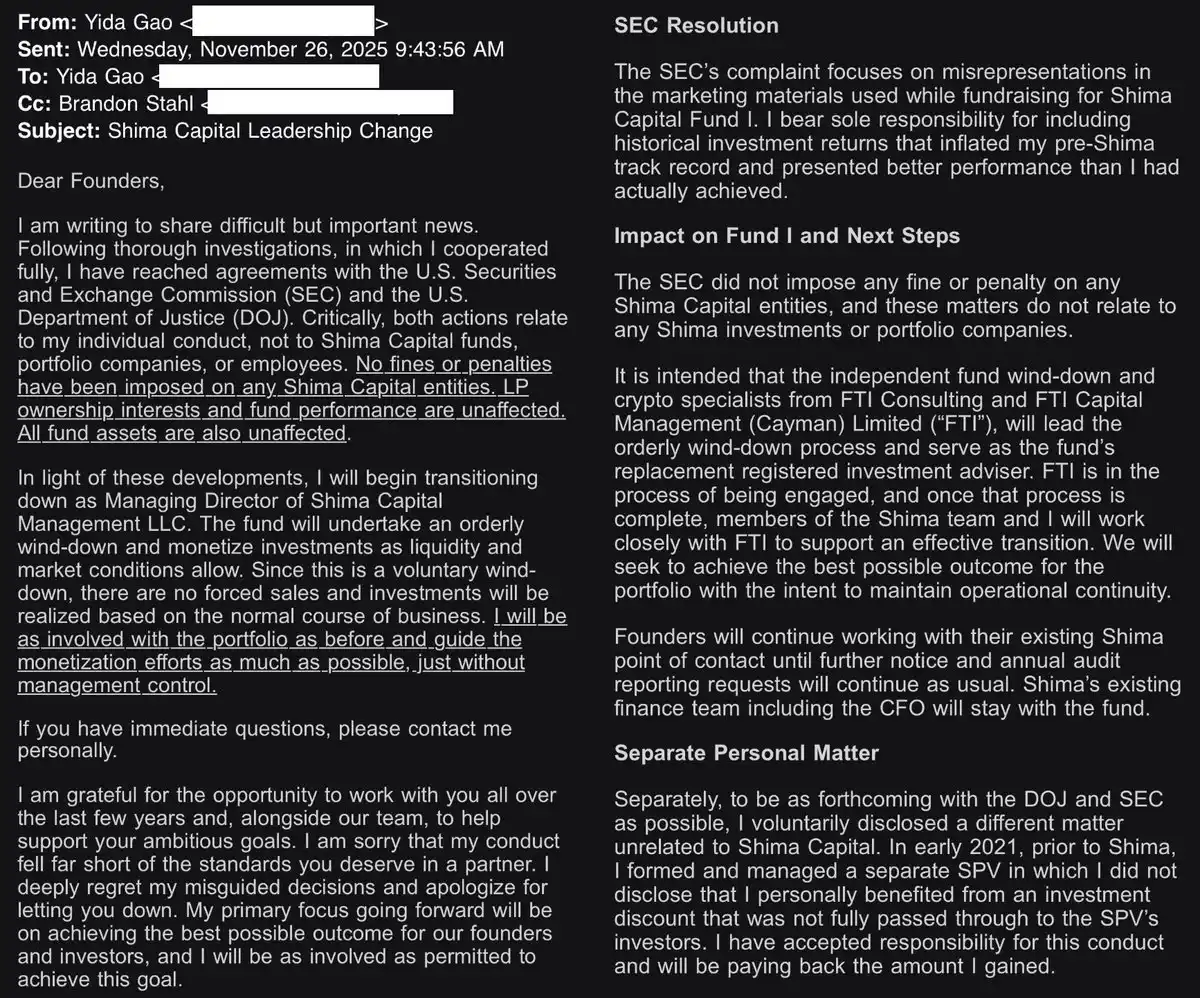

Another crypto venture capital firm has fallen. On December 17, Shima Capital was exposed to be quietly winding down its operations.

In this brutal crypto cycle, the exit of VCs is not uncommon, but Shima Capital's departure is not dignified. Unlike other VCs that died from liquidity drying up or were dragged down by poor investment portfolios, Shima Capital's downfall stemmed more from internal moral hazards and management chaos.

The direct trigger for this decision was the lawsuit filed by the U.S. SEC against the institution and its founder Yida Gao three weeks ago. The charges alleged that they violated multiple securities laws and illegally raised over $169.9 million from investors through fraudulent means.

Under regulatory pressure, Yida Gao quickly chose to settle with the SEC and the U.S. Department of Justice. While paying a fine of approximately $4 million, he decided to close the fund and announced his resignation from all positions, expressing deep regret for his "misleading decisions." The foundation will enter a liquidation process and will gradually liquidate assets to repay investors as the market allows.

As a once high-frequency star venture capital in the crypto field, Shima Capital's rise relied more on the founder's elite光环. American-Chinese Yida Gao was a Wall Street top student with a background from MIT. He even took over the crypto course taught by former SEC Chairman Gary Gensler at MIT. His resume also includes well-known institutions like Morgan Stanley and New Enterprise Associates.

With this background, Shima easily raised $200 million for its first fund, with backers including Dragonfly, hedge fund billionaire Bill Ackman, Animoca, OKX, Republic Capital, Digital Currency Group, and Mirana Ventures.

Holding huge funds, Shima became one of the most active hunters in the last cycle, betting on over 200 crypto projects, including hot projects like Monad, Puddy Penguins, Solv, Berachain, 1inch, Coin98, etc. Despite the vast investment portfolio, Shima and its team were evaluated by investors as young and lacking experience, not truly understanding the industry, and merely following the speculative wave of cryptocurrency.

More seriously, all this was built on lies. According to the SEC's lawsuit documents, when raising $158 million for Shima Capital Fund I, he fabricated past performance, claiming that one of his investments had achieved a 90x return, while the actual data was only 2.8x. When the lie was at risk of being exposed, he even tried to brush it off as a "typo" to investors.

Not only that, Yida Gao raised funds from investors through an SPV to purchase BitClout tokens, promising discounts and principal protection. However, in reality, although he bought the tokens at a low price, he did not offer them to investors at the original price but instead resold them to his own SPV at a markup, secretly profiting $1.9 million without disclosure.

From a long-term perspective, Shima's exit also sends a positive signal to the market: crypto wrongdoing is no longer outside the law, and the industry's transparency and ethical standards will be better improved.

Related reading: Unveiling the Founder of Shima Capital Suspected of Misappropriating Assets: From Fujian Immigrant to Wall Street Financial Elite

The Era of Easy Money is Over, VCs Enter an Evolution Period

The so-called failure of the VC model is essentially the market forcing the industry to evolve.

Currently, the assembly-line model of "VCs forming a syndicate, retail investors taking the bag" has been broken, and funds are rapidly withdrawing from air projects. For example, not long ago, Monad, with its豪华 investment lineup, still couldn't escape price difficulties after launch, which also made a group of VCs "break defense," and venture capital firms like Dragonfly engaged in fierce debates around value valuation.

The industry's rules of the game have changed. Whether it's the success of projects without VC funding (like Hyperliquid) or the community's resistance to high-valuation projects, they are actually pushing venture capital institutions out of their arrogant ivory towers. Only when the path of making quick money simply by "issuing and selling tokens" is blocked will VCs truly settle down to find projects with造血能力 that can solve practical problems.

This阵痛 is obvious. As retail investors exit leading to liquidity drying up, the traditional exit channels for VCs are blocked. Valuation adjustments not only lengthen the return cycle but also leave a large number of investments facing serious paper losses.

Not long ago, Akshat Vaidya, co-founder of Arthur Hayes' family office Maelstrom, publicly complained that the principal of his investment in a certain Pantera fund four years ago had nearly halved, while Bitcoin had risen about twofold during the same period.

Another VC confided to PANews that they were overwhelmed by exits. Even though they participated in the seed round, the current token price they hold is lower than the cost price. Even if a project is listed on a top exchange like Binance, years later they only recovered one-fifth of the principal. Many projects choose to随便 list on a small exchange to give investors an交代, but there is simply no liquidity to exit. Some projects even choose to lie flat, and when asked, the answer is always to wait for the right time.

Glassnode data shows that currently only about 2% of the altcoin supply is in a profitable state, showing an unprecedented market differentiation. During Bitcoin bull markets, it is historically uncommon for altcoins to consistently underperform.

The data confirms that the era of making money with eyes closed is彻底 over.

The end of one era means the beginning of another. Rui from HashKey Ventures pointed out on social media that VCs are not afraid of熬, they are afraid of快, which is also why bear markets are more suitable for VCs. To truly succeed, one must survive until the next dead period. Unlike project parties, VCs are quite good at enduring. At the same time, most crypto VCs essentially arbitrage information asymmetry, coupled with some path dependence, earning some hard money and channel fees. More importantly, many of these people have now turned into market agents or market makers, which is essentially not much different.

Build Roads Before Buildings, Seeking Certain Opportunities

Facing the receding hot money, VCs are not all "fleeing" but are making strategic contractions and adjustments to their battle lines.

"If a project doesn't have a data dashboard, we won't invest in it." Recent participants at a Dubai crypto event revealed that VCs now pay more attention to actual business data rather than单纯 stories. Facing the bleak reality, VCs have significantly raised investment thresholds or even completely abandoned new investments.

Dovey Wan, founder of Primitive Ventures,坦言 that for investors, the ratio at which strength and luck can be exchanged (at present) is becoming increasingly苛刻, especially in the post-GPT era. This is true for all industries: choice is more important than effort, but choice is much harder than effort.

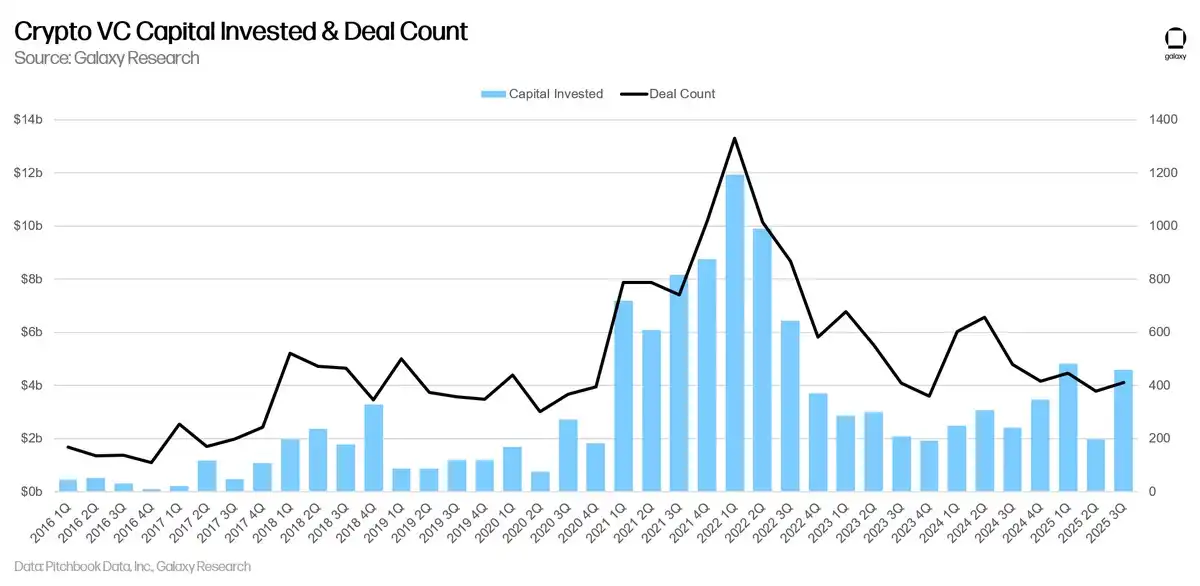

Pantera Capital revealed a positive trend in a recent video. According to its disclosure, although the total financing amount in the crypto field reached $34 billion this year, exceeding the records of 2021 and 2022, the number of transactions decreased by nearly 50%. This phenomenon has several main reasons: First, the investor structure has changed. Family offices and individual investors active during 2021-2022 have become more cautious after experiencing bear market losses, with some even choosing to exit the market. Second, the investment strategies of existing VCs have become more concentrated. These VCs prefer to put funds into a few high-quality projects rather than casting a wide net as before, because the capital, time, and resource costs required to launch new projects are higher now. On the other hand, some funds have shifted to relatively safer assets, which also explains why大量资金 is highly concentrated in Bitcoin and a few mainline assets in this cycle. Third, funds are ample but deployment节奏 has slowed. Many venture capital funds raised large amounts of money in 2021 and 2022 and are currently holding sufficient "ammunition," mainly used to support existing investment portfolios and are in no hurry to invest in new projects. From a longer-term perspective, this change is not a negative signal but rather a sign of the market maturing.

Galaxy Research's recent analysis of Q3 investment reports also pointed out that crypto VC investment额 in the quarter increased but was concentrated. Meanwhile, nearly 60% of investment funds flowed to late-stage companies, the second-highest level since Q1 2021. Compared to 2022, venture capital fundraising data also shows a significant decline in investor interest. This data also shows that VCs are more willing to heavily bet on certain opportunities.

To hedge against the risks of a single market, some crypto VCs have started to "not focus on their main business,"瞄准 markets outside of crypto-native. For example, the recent investment list of YZi Labs shows that its gaze has turned to biotech, robotics, and other圈外 sectors. Some crypto-native funds have long started investing in AI projects. Although they don't have significant pricing advantages compared to tech funds, it's an attempt at transformation.

Pantera also reflected on the investments of the last cycle. "In the last cycle, a large amount of capital flowed into speculative areas like NFTs and the metaverse. These projects tried to skip infrastructure and directly build the 'cultural top layer.' But it's like building a castle on sand: the underlying infrastructure wasn't ready, payment rails were not mature, the regulatory environment was unclear, and the user experience was far from mainstream level. The industry was too eager to seek killer apps and invested resources in the application layer where the soil wasn't ready."

Pantera believes that this crypto cycle is undergoing a necessary "correction." Now more funds are flowing into infrastructure construction, such as more efficient payment chains, more mature privacy tools, and stablecoin systems. This path is the correct sequence, and the applications of the next cycle will have the conditions to truly explode.

Lay the foundation first, then build the building.

The brutal clearing of crypto VCs at present is both a阵痛 and a reshaping.