Ethereum is holding a commanding lead over Bitcoin in an interesting adoption indicator, even as its price action continues to face pressure around $2,000 to $2,100. New on-chain data shows that ETH’s network user base has expanded massively over the past decade.

As it stands, Ethereum now has more than three times as many wallets with balances as Bitcoin, showing that the market might actually be underpricing the world’s second-largest cryptocurrency.

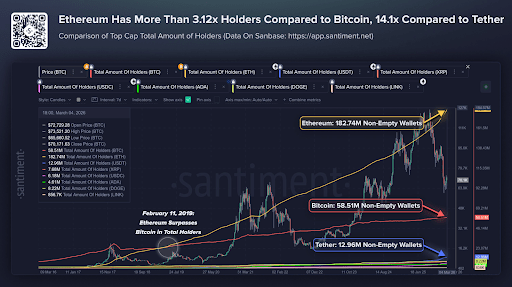

Ethereum’s Holder Base Goes Parabolic

On-chain analytics platform Santiment recently highlighted an interesting trend across the crypto market: Ethereum’s holder base has increased far more than that of any other major digital asset.

The data shows that ETH now has about 182.7 million non-empty wallets, compared with roughly 58.5 million for Bitcoin. That places ETH at more than 3.1 times the number of holders held by Bitcoin, and this gap has been widening steadily for years.

The turning point came in February 2019, when Ethereum first surpassed Bitcoin in the total number of addresses holding a balance. Since then, the divergence has increased, with ETH’s wallet growth curving upward while Bitcoin’s line has climbed at a much slower pace.

Tether, despite its ubiquity as the dominant stablecoin, holds just 12.96 million wallets, making Ethereum’s base more than 14 times larger. Interestingly, other notable altcoins also cannot keep up with ETH, where users are actively adding to positions. The number of non-empty wallets on the XRP Ledger sits at 7.68 million, Dogecoin at 8.22 million, and Cardano at 4.61 million. None comes close to Ethereum.

Price Lags Adoption, But The Rally To $5,000 Is Intact

The bullish case for ETH is easy to understand. A network with 182.74 million non-empty wallets has a much deeper base of users, and that kind of adoption can eventually feed into price. However, the disconnect between Ethereum’s on-chain strength and its current price around $2,000 is not lost on market participants.

For instance, crypto analyst Merlijn The Trader used the Ethereum Rainbow Chart to predict a notable rally for the leading altcoin. According to the analyst, the Rainbow Chart has entered its cheap zone for the first time since 2020, the same reading that preceded ETH’s run from $700 to $4,800 in 2021.

Right now, there are two important levels to watch for Ethereum. A move above $2,500 would unlock the next band on the chart, and this would open up the door to a slow distribution phase to new highs. On the other hand, a drop below $1,900 would push ETH into a steal zone based on the Rainbow model. At the time of writing, ETH is trading at $2,103, up by 2.9% in the past 24 hours.