Author: Tara Tan

Translation: Deep Tide TechFlow

Source: The Strange Review

Deep Tide Introduction: xAI, under SpaceX, acquired Anysphere, Cursor's parent company, for $60 billion in stock—not for market share, but for the high-quality training data generated by 7 million developers writing code every day. Strange Ventures partner Tara Tan uses this deal to put forward a judgment: to be a major AI player, you must integrate the entire stack of compute, models, and applications. This short review breaks down Anthropic's path to a 540-fold revenue increase in 28 months and explains why model companies will aggressively acquire into the application layer next. Note the author's identity as a VC, and full-stack is precisely her own investment thesis.

Code generation is by far the strongest killer application for large language models, bar none.

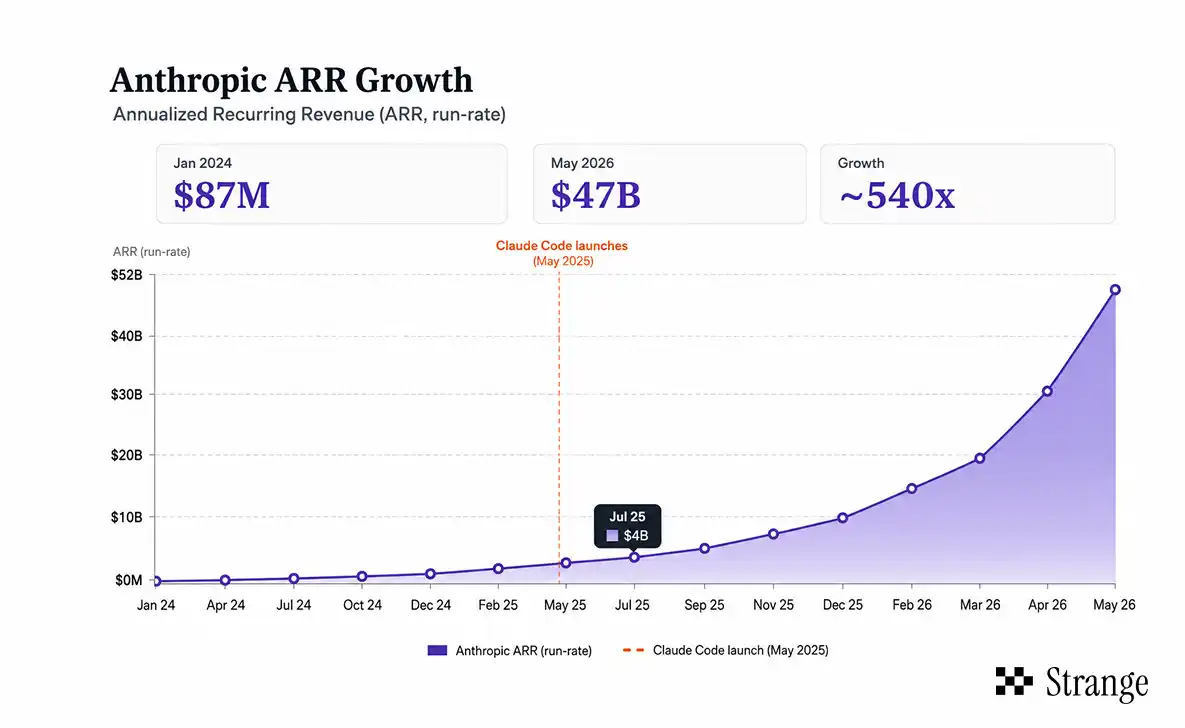

Anthropic's revenue grew from an annualized rate of $87 million in January 2024 to $47 billion in May 2026, an approximately 540-fold increase in 28 months. This growth was driven by two engines firing simultaneously: top-down enterprise partnerships (Claude is the only frontier model available on all three major cloud platforms) and bottom-up developer penetration, powered by Claude Code. This product is the fastest-growing in the company's history, going from zero to $2.5 billion in annualized revenue in 9 months. Anthropic now holds 54% of the enterprise AI programming market.

Cursor is the same bet SpaceX is making.

Yesterday, SpaceX announced the acquisition of Anysphere, the company behind Cursor, for $60 billion in stock. This AI programming tool is used daily by 7 million developers. Incubated at MIT four years ago, its annualized revenue has surged to $2 billion, making it the highest-revenue AI programming tool in its category. Over the past year, its market share has been declining, from 41% to 26%, as Claude Code gained ground. But xAI isn't buying market share.

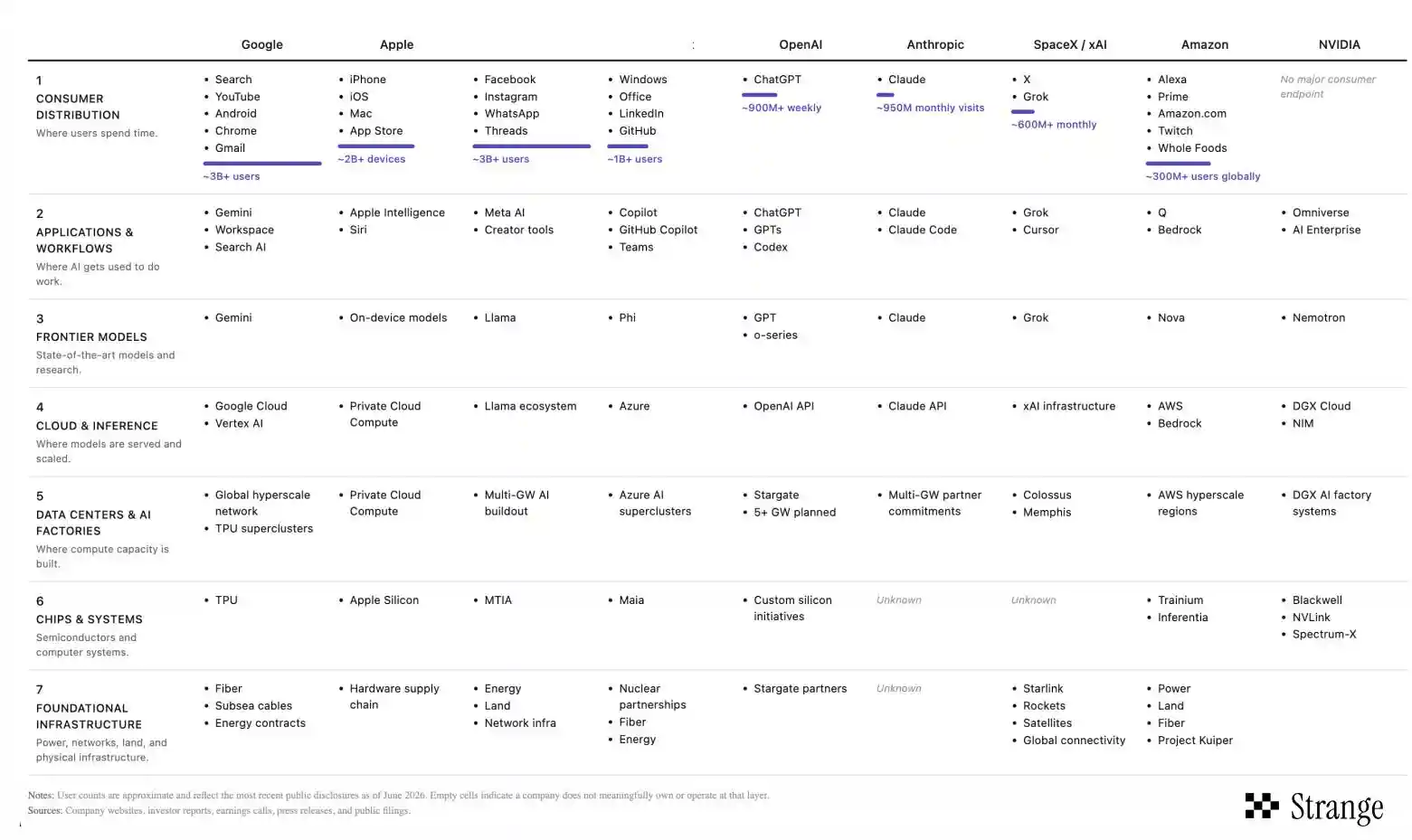

xAI already has the full stack: Colossus for compute, Grok for the model, and X for the application. The problem is that X is for browsing, while Cursor is for writing code. The data generated by developers writing code is arguably the highest-signal training data in the AI field, and that's precisely what Grok lacks to complete its competitive edge.

This confirms a thought I've been pondering since the OpenAI-NVIDIA deal last September:

To be a major AI player, you must go full-stack.

The logic is becoming increasingly clear. Better products lead to better infrastructure (more data), and better infrastructure, in turn, leads to a better experience. This has always been the core investment logic at Strange.

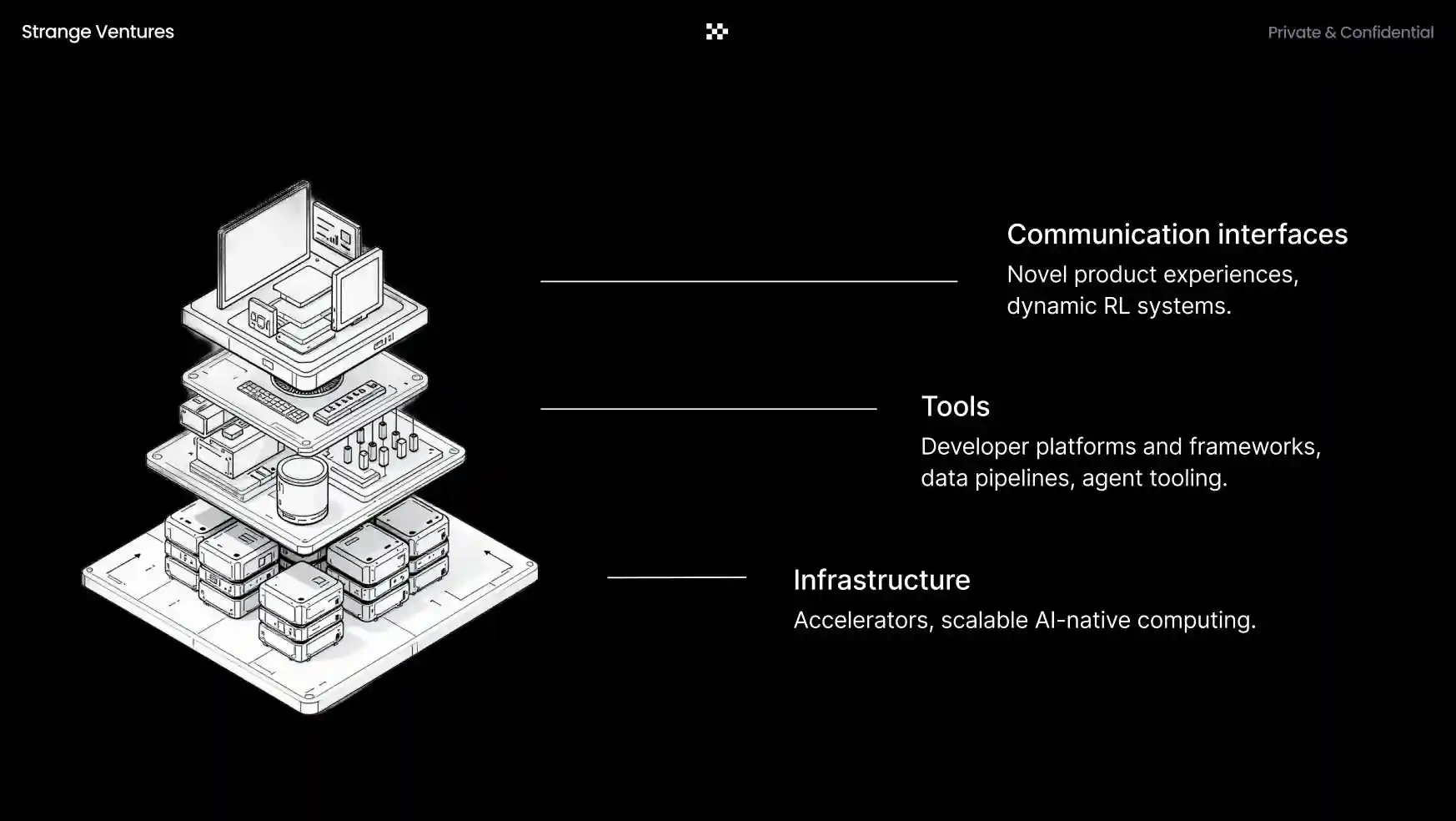

Caption: The author's team's investment logic diagram on "Full-Stack Flywheel"

Going full-stack achieves two things:

First, the unit economics of building and training models become sustainable.

Second, you gain proprietary training data from the application layer, differentiating yourself from other model vendors. User data and workflow lock-in then form a solid moat.

The next few years will likely see actions like these: model companies either internally develop applications or aggressively acquire upward, directly swallowing the application layer.

A popular saying among entrepreneurs now is: Because building products is 10 times easier than before, companies need to be 10 times more ambitious to succeed. Currently, this seems to be holding true across various sectors.

——Tara