Written by: Henry Kim, Ryan Yoon

Compiled by: Luffy, Foresight News

TL;DR:

- Crypto payment cards currently resemble debit cards on the eve of their commercialization in the 1990s: both leverage existing payment networks to bypass merchant acceptance. However, the daily financial relationships built around a primary bank account (such as salary deposits, recurring payments) have not yet formed.

- The annualized transaction volume of crypto payment cards is approximately $18 billion, with RedotPay alone commanding over half of the market share, and its users are concentrated in emerging markets. At this stage, crypto payment cards are merely a supplementary tool in regions with scarce access to US dollars, far from becoming a universal financial infrastructure.

- Growth in payment transaction volume alone cannot establish crypto payment cards as foundational infrastructure. The ultimate market landscape will be determined by three types of players: platforms that control fund flows, service providers that capture areas underserved by traditional finance, and businesses that build daily core account relationships on top of the underlying payment layer.

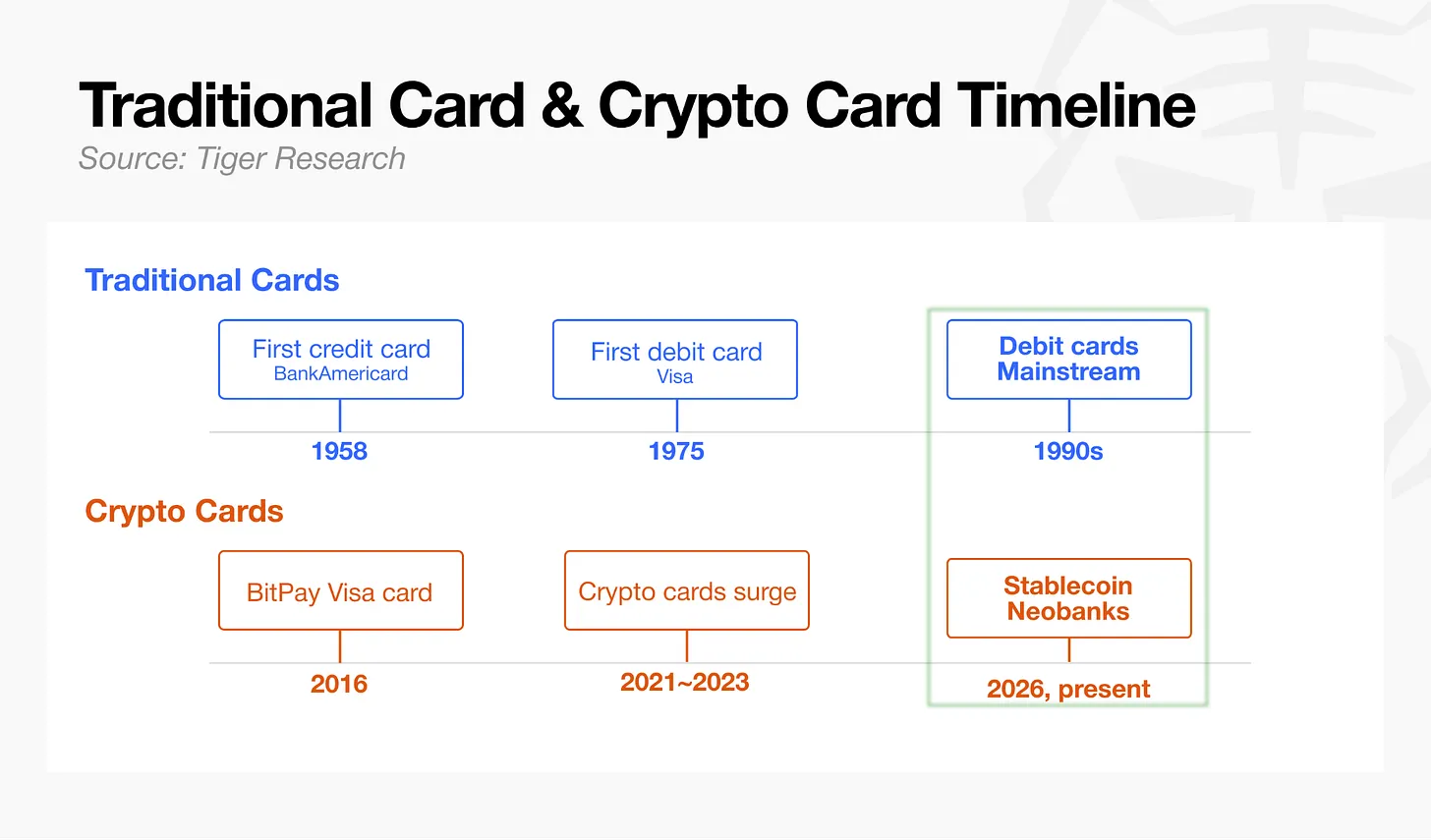

The Parallel World of Debit Cards in the 1990s

In September 1958, Bank of America mass-mailed credit cards to 65,000 residents of Fresno, California, marking the first payment card launched without supporting underlying infrastructure. A year after launch, the business performed poorly, with a delinquency rate of 22% and losses as high as $20 million. The industry spent 15 years building an electronic settlement system. Debit cards officially debuted 17 years later, and Visa took a full 20 years to establish a global universal payment standard.

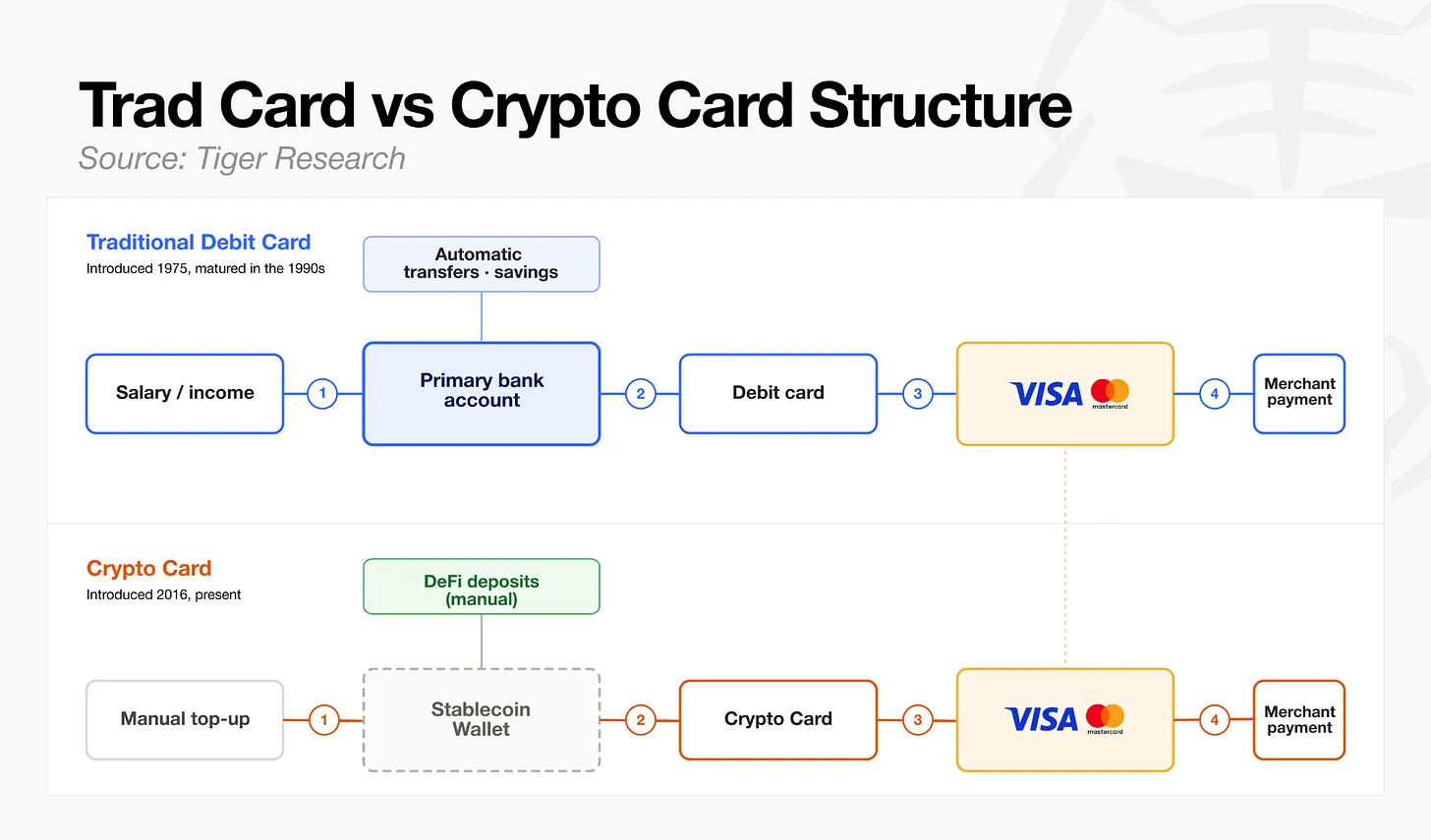

The biggest watershed between traditional payments and crypto payments lies in whether they establish users'常态化 financial account relationships. Debit cards were born in 1975, but it wasn't until the widespread adoption of direct salary deposits in the 1990s that they became a standard tool linked to a personal core bank account. In contrast, today's crypto payment cards primarily have user self-topped-up stablecoins as their funding source; the vast majority of crypto wallets cannot handle daily financial flows like salary deposits or fixed deductions. The industry's overall development stage is roughly equivalent to that of debit cards around 1990.

The future leader in the crypto payment card space will not be determined by the number of cards issued, but by who first builds a true core account serving daily income and expenses, or finds a growth driver that encourages long-term user retention.

Monthly Transactions of $1.5 Billion Do Not Signal Industry Maturity

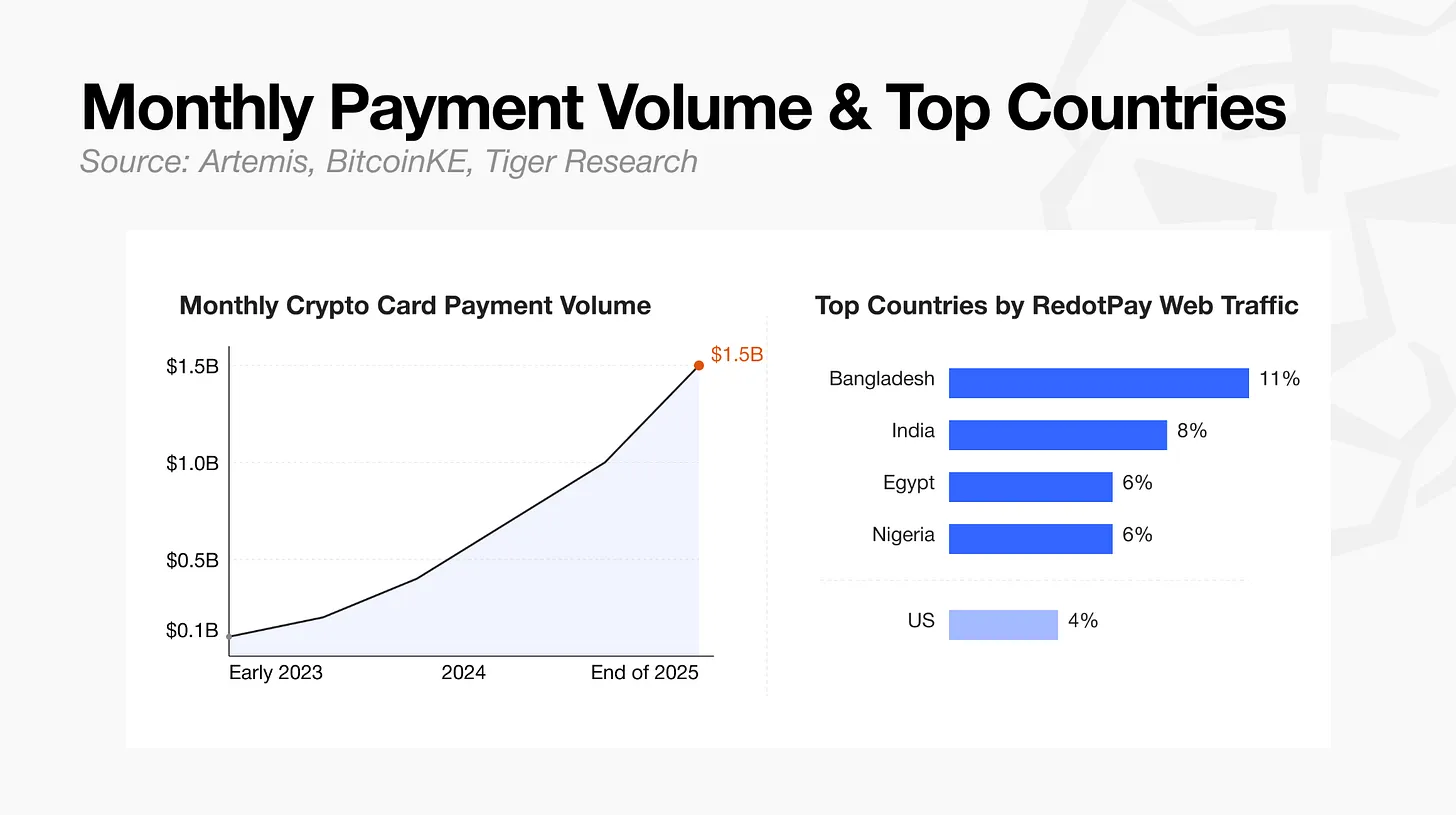

According to data from analytics firm Artemis, the monthly transaction volume of crypto payment cards grew from $100 million at the beginning of 2023 to $1.5 billion by the end of 2025, an annualized scale of approximately $18 billion. Influenced by on-chain data统计口径, the actual annualized figure may fluctuate slightly, but the explosive growth in transaction volume is an established fact.

A closer analysis of these metrics reveals clear concentration in services and regions. Top provider RedotPay commands over half of the entire industry's transaction flow; platform访问 users are highly concentrated in emerging markets: Bangladesh accounts for 11%, India 8%, Egypt 6%, Nigeria 6%, while the United States represents only 4%.

This shows that the real demand for crypto payment cards does not come from developed mainstream markets, but from developing regions with insufficient financial services and limited access to US dollars.

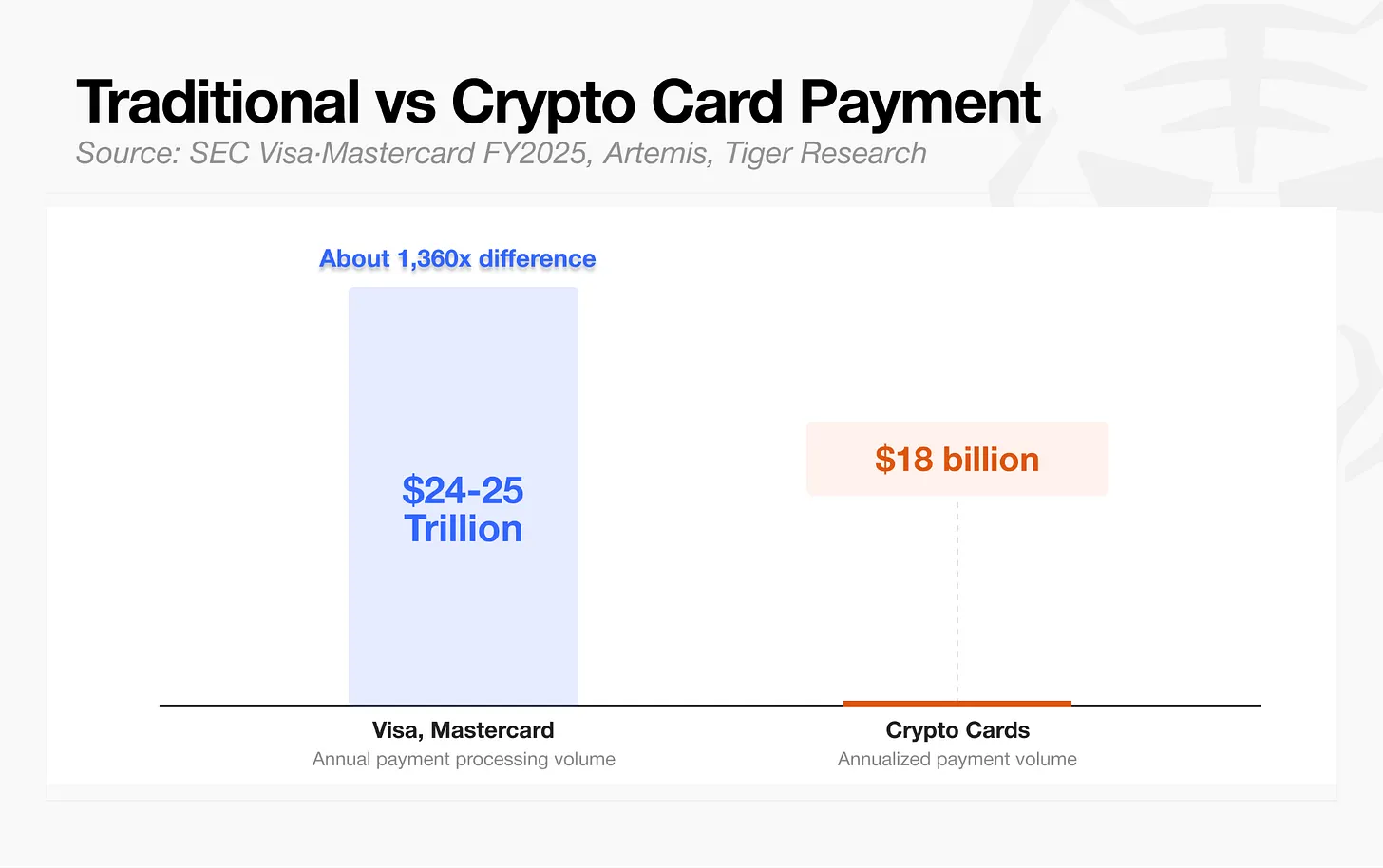

Compared to mature financial networks, the scale gap for cryptocurrencies remains enormous. Visa and Mastercard's annual payment volumes reach $24 to $25 trillion, while crypto payment cards' annualized transaction volume is only $18 billion—they are completely不在同一量级.

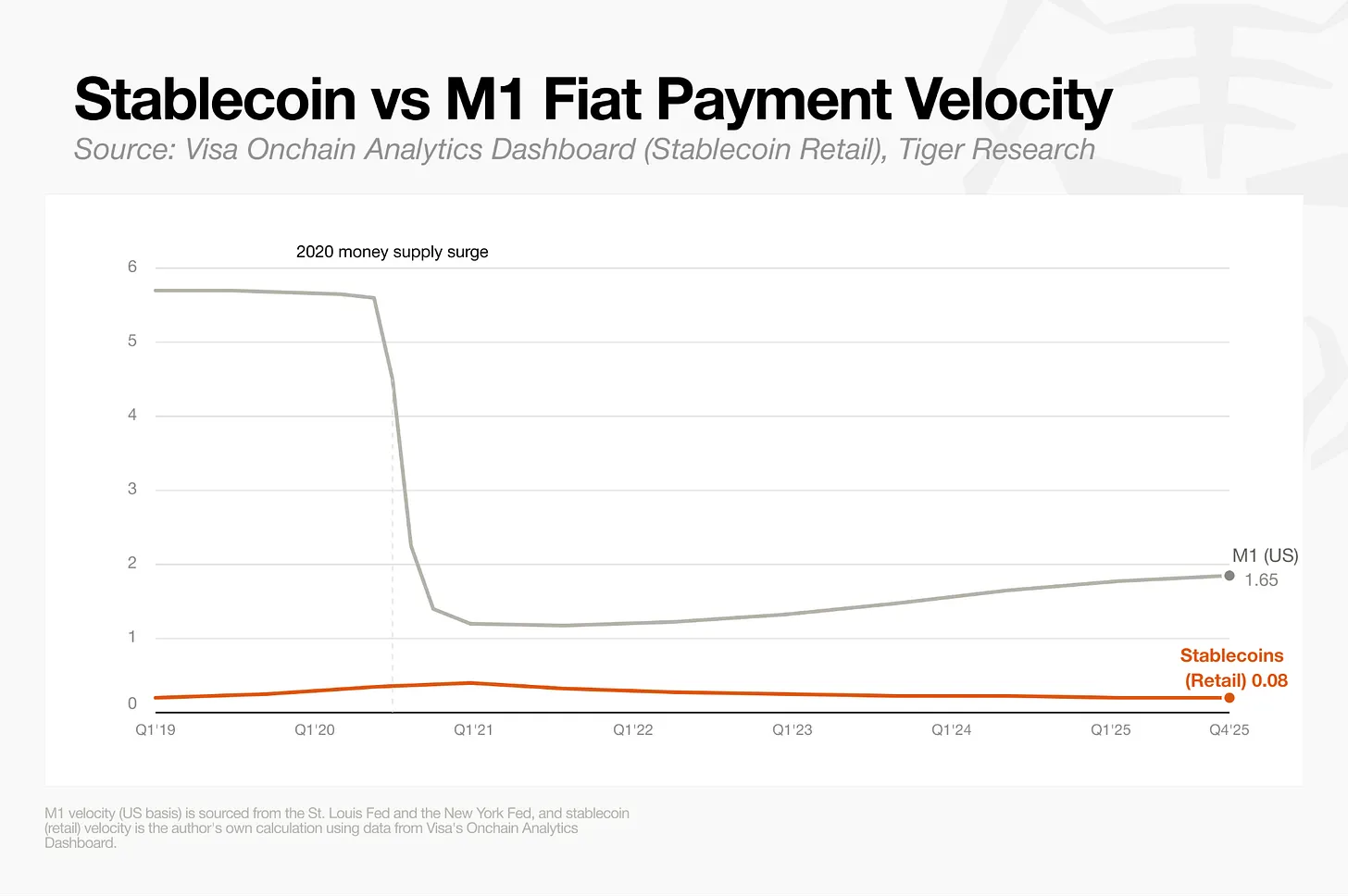

The velocity of circulation indicator, which measures the普及度 of daily payments, is also relatively low. According to Visa statistics, the retail velocity of on-chain stablecoins is only 0.08, merely one-twentieth of the velocity of narrow法定 money M1 (1.65). The user pattern for stablecoins is not a常态化流程 of salary deposit, daily spending, and循环充值. Instead, it's more often a one-time top-up followed by sporadic card usage.

Growth in transaction volume numbers does not equate to the market having formed a mature, universal clearing system. Currently, a large portion of crypto payment card transactions come from populations in emerging markets who cannot conveniently open US dollar accounts. For these users, crypto cards indeed offer practical financial value.

However, in developed markets, crypto payment cards have yet to find a stable product-market fit or establish the deep account绑定 relationships brought by direct salary deposits and automatic bill payments.

Considering both funding inflow channels and spending scenarios, current crypto payment cards are more suitable for specific national细分需求, serving as a supplementary tool rather than universal financial infrastructure. Nonetheless, amid rapid industry growth, leading players across four major business models are simultaneously完善各环节产业链.

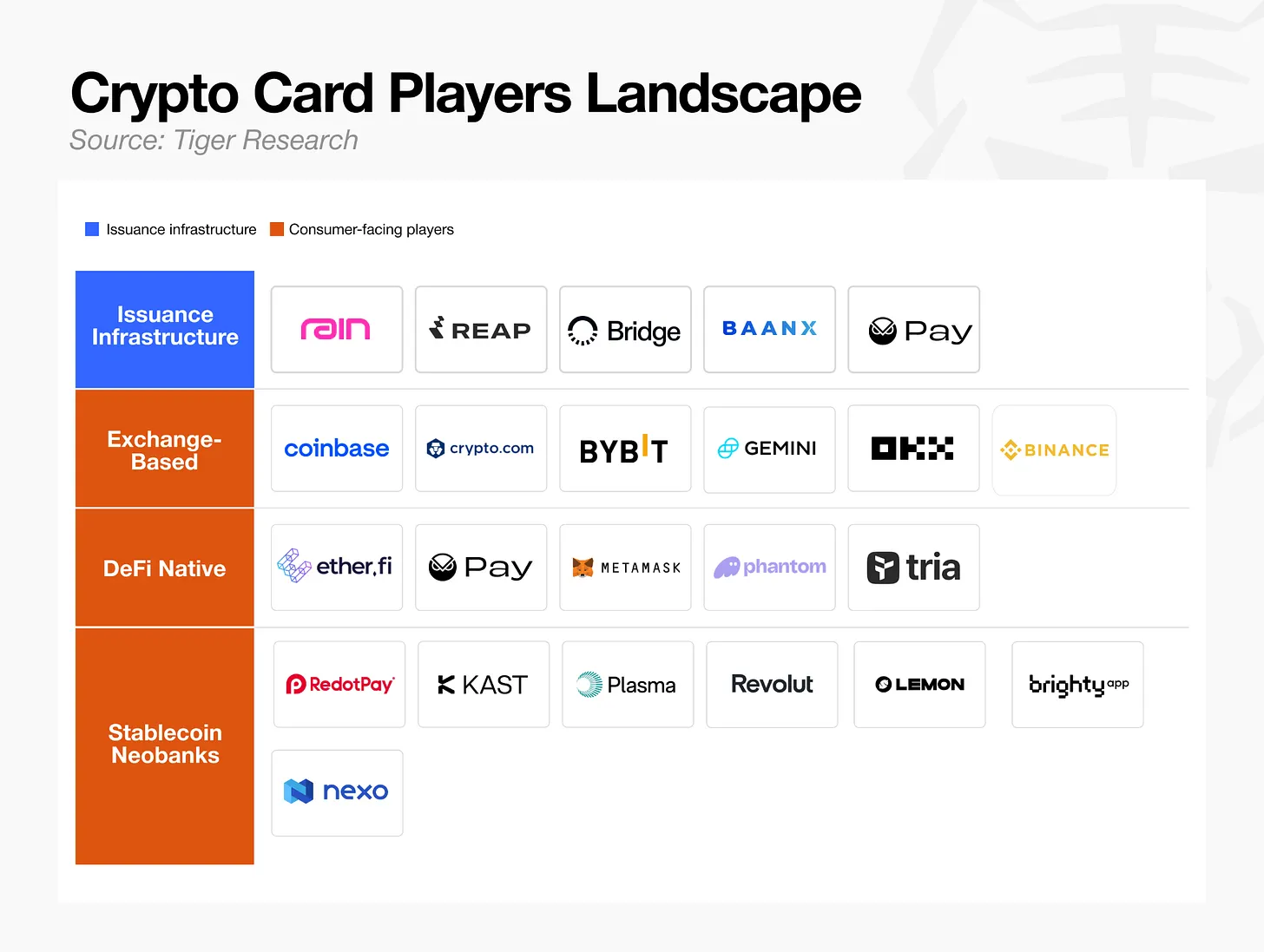

Four Mainstream Business Models for Crypto Payment Cards

The crypto card industry can be broadly divided into four business models, with various participants vying for领先地位 across different layers. These models are diverse, ranging from companies focused on providing backend infrastructure to those that merely borrow the card form but have completely different underlying structures.

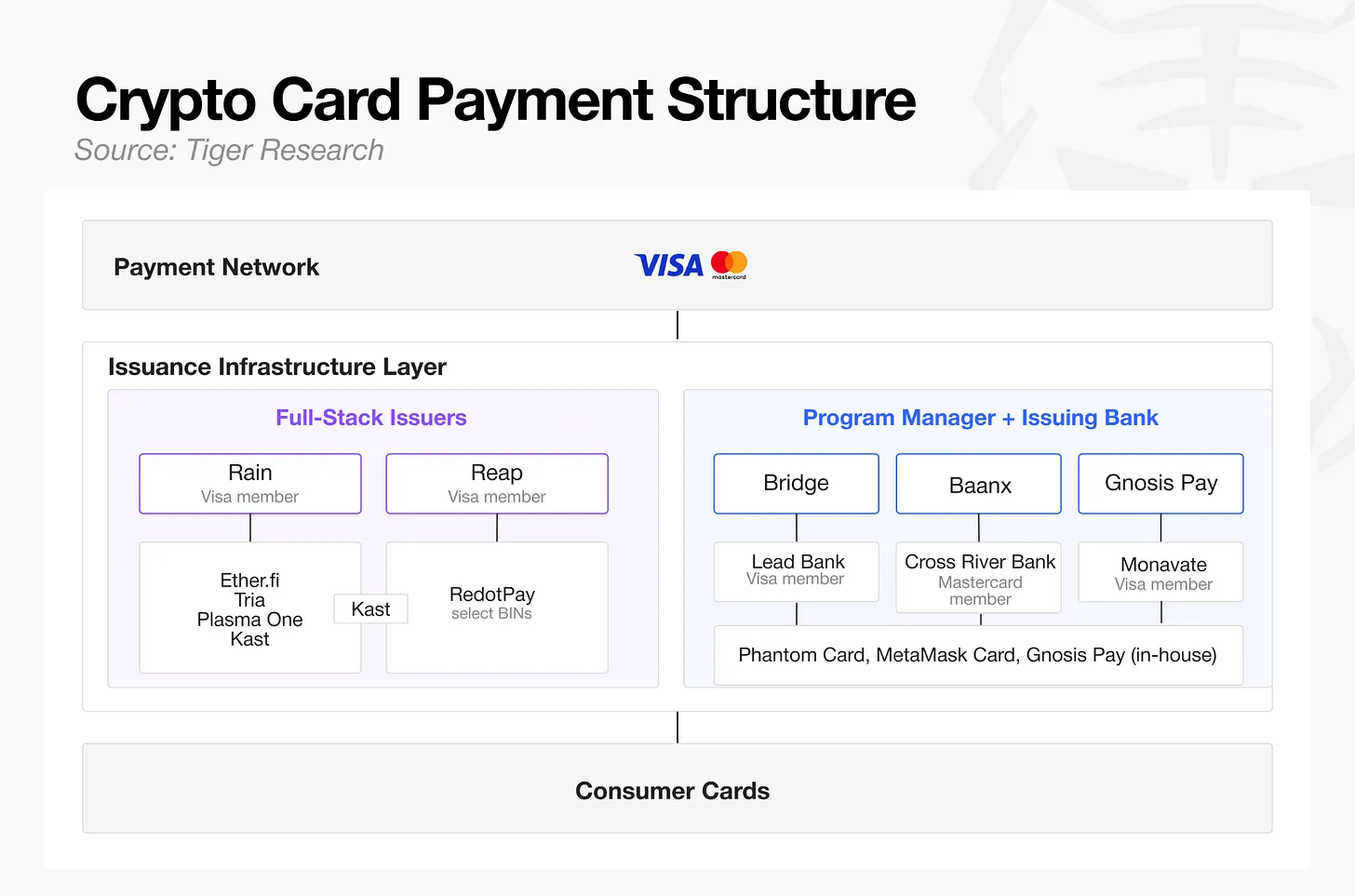

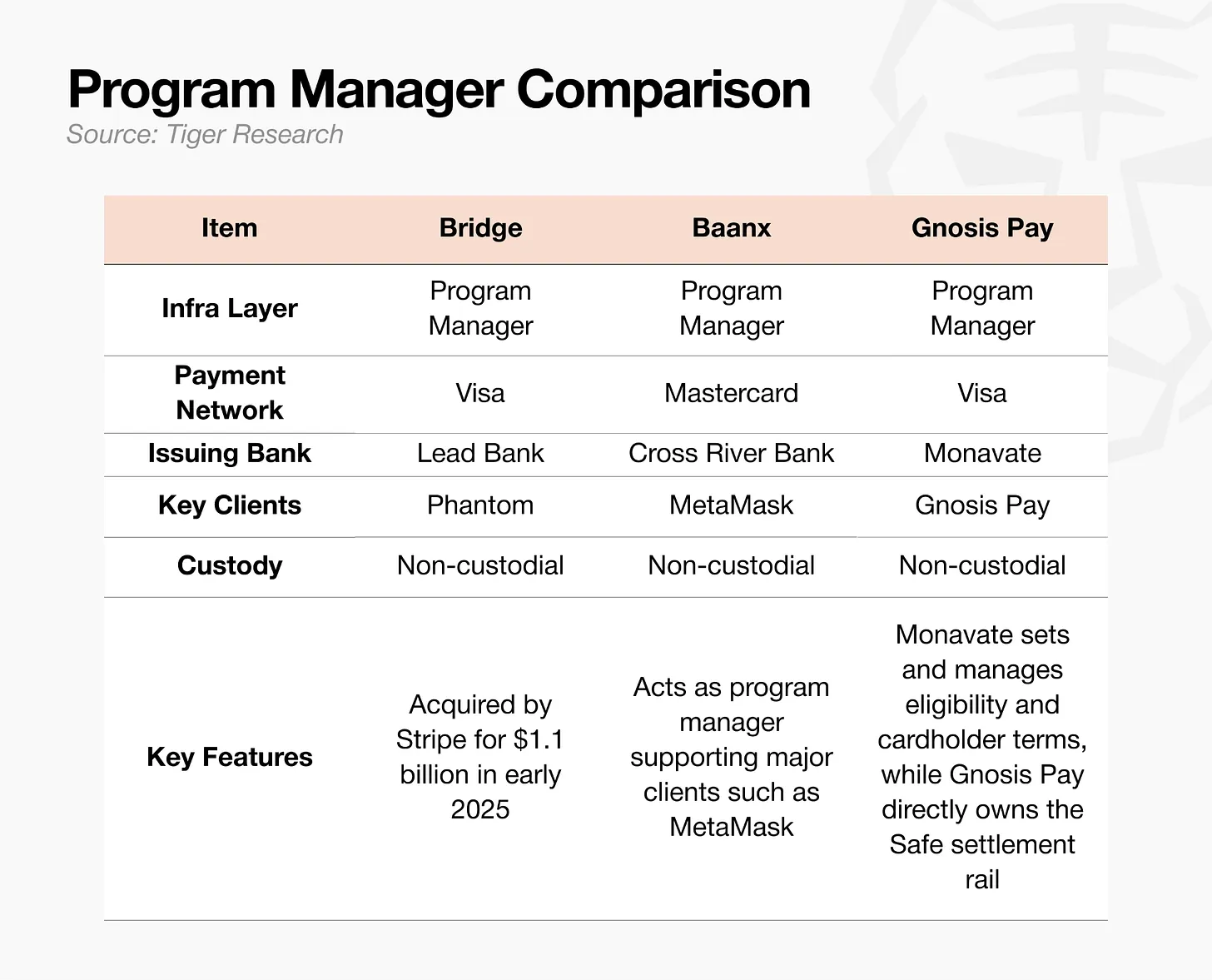

Card Issuing Infrastructure

The two well-known payment networks, Visa and Mastercard, are also applied within the cryptocurrency card ecosystem. Beneath them lies the card issuing infrastructure layer, which ultimately extends to the consumer card. As shown in the diagram above, there are two structures within the issuing infrastructure layer. The first is the traditional two-tier structure, where the program manager responsible for operations is separate from the issuing bank responsible for membership management and settlement. The second is the full-stack issuer, such as Rain and Reap, which combine these two roles.

Multiple seemingly independent payment card brands复用 the underlying infrastructure of a few key program service providers. Phantom Card, MetaMask Card, and Gnosis Pay are typical examples.

Seemingly independent payment card products like Kast, Ether.fi, Tria, and Plasma One also share underlying infrastructure with a small number of service providers. Rain handles the majority of consumer card business.

The high concentration in issuing infrastructure has also attracted traditional digital banks with mature experience to enter the field. In March 2026, Nium launched a stablecoin issuing platform supporting both Visa and Mastercard networks; other traditional financial infrastructure vendors include Bridge, acquired by Stripe for $1.1 billion in early 2025, and BVNK, acquired by Mastercard for up to $1.8 billion in March 2026.

Competition in the issuing space is intensifying, with full-stack issuers, established program managers, and new fintech players all competing.单纯 issuing业务 can no longer easily build high barriers.

Rain has formed a差异化优势 through its daily stablecoin settlement capability. Traditional card settlement cycles take several days, but Rain achieves T+0 stablecoin settlement via Visa, significantly improving capital turnover efficiency for partners like Ether.fi. Recently, the platform launched an AI agent control layer supporting the programmatic generation of disposable virtual cards, moving functionality beyond basic issuing infrastructure.

To stand out, issuing service providers cannot merely offer basic payment channels; they must also quickly implement differentiated value-added features that traditional infrastructure cannot provide.

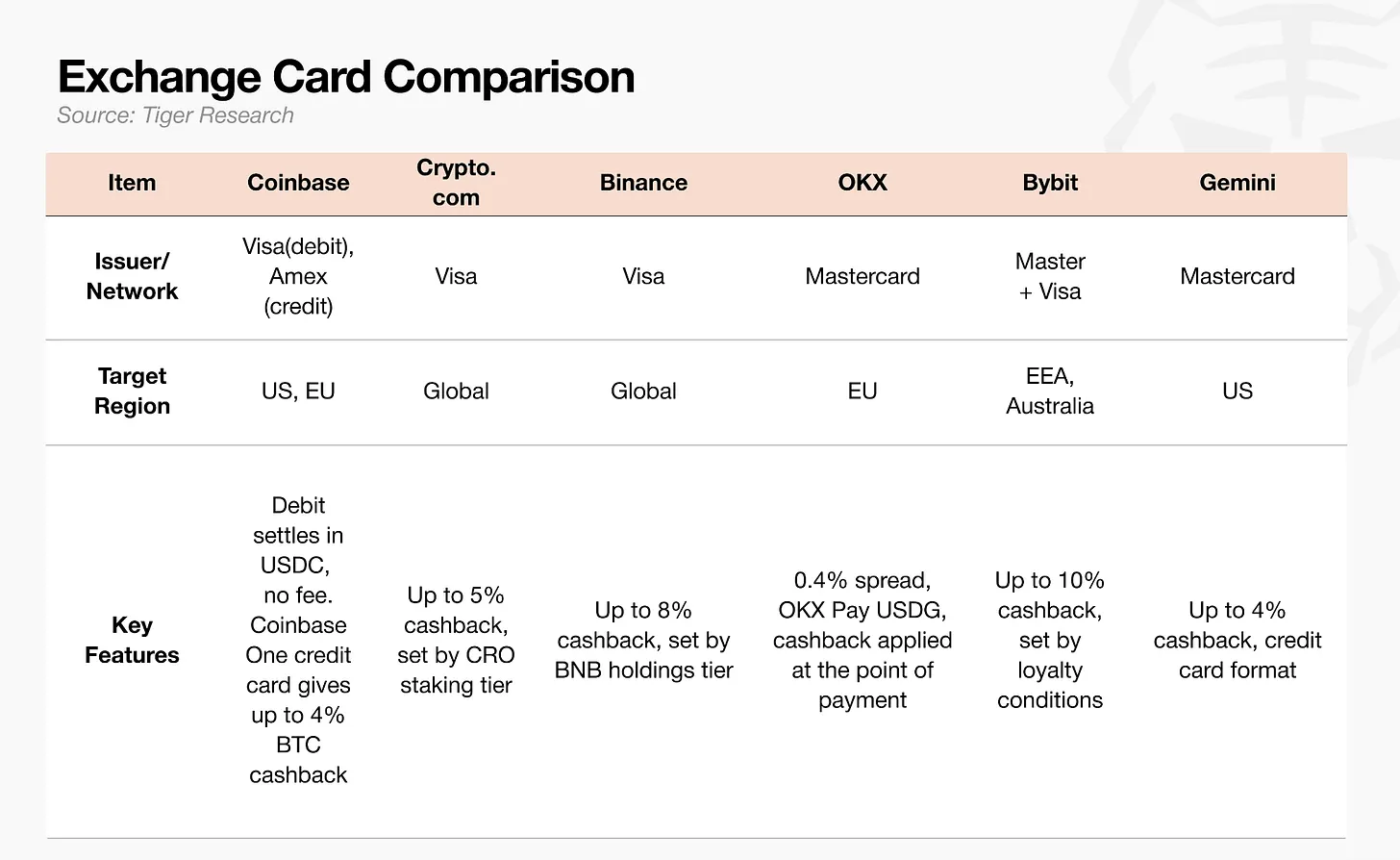

Exchange-Partnered Payment Cards

For exchanges, payment cards are not a core revenue source; their primary role is to retain existing users. By overlaying card functionality on the platform's existing users, assets, and transaction data, they prevent user流失. The platform's real profits come from trading fees, lending business, and asset custody, not from刷卡消费 itself.

Exchanges view payment cards as a traffic入口 for building a financial super app. However, the native token cashback model carries risks: token price volatility directly leads to unstable actual cashback ratios.

Alternative industry solutions include stable币返现 and balance interest, but the US "GENIUS Stablecoin Act" prohibits interest-bearing business, creating an obstacle for market expansion.

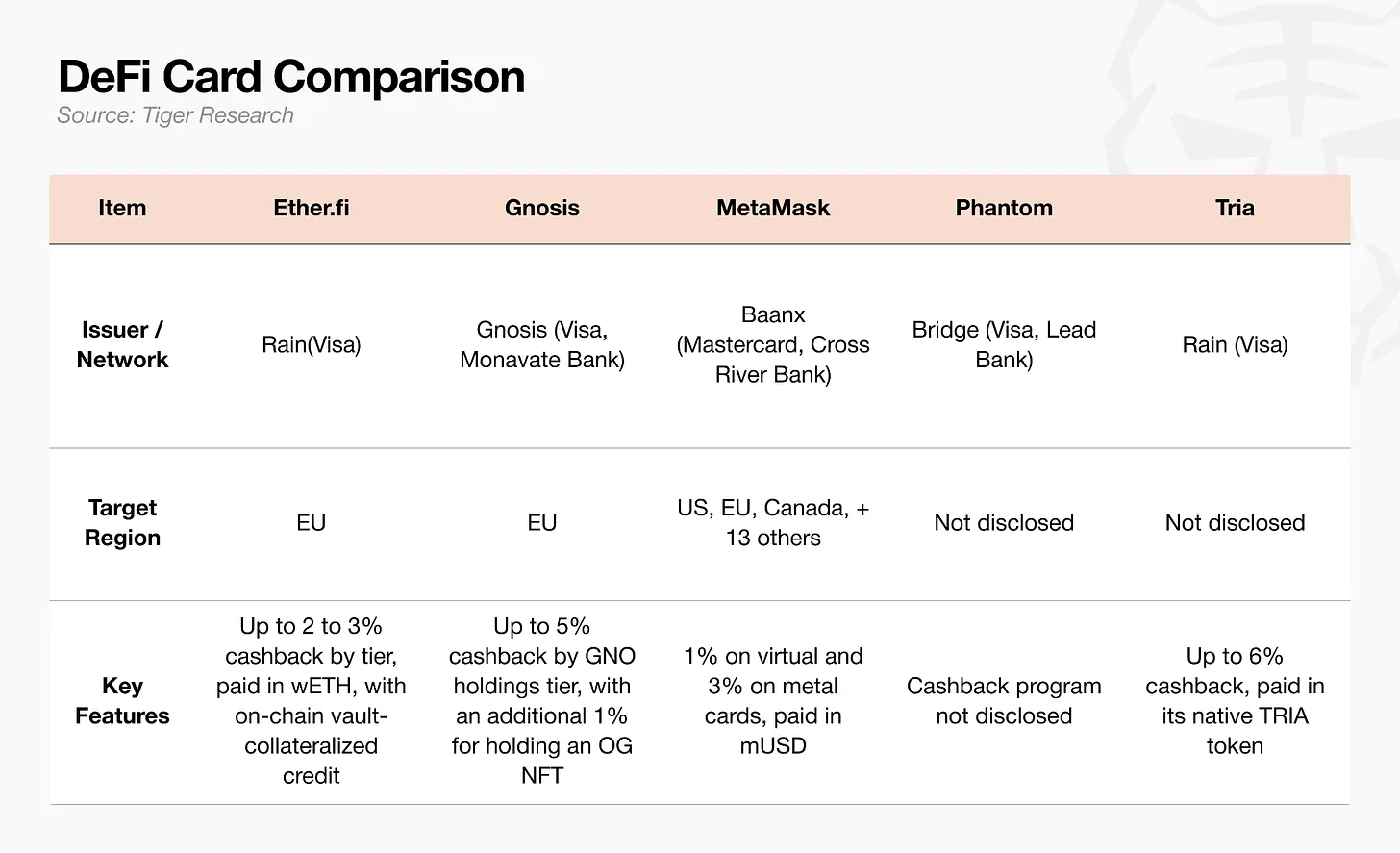

Decentralized Wallet / DeFi

The core logic of this model is that the wallet itself is the user's account, with assets self-custodied on-chain,无需交由 a centralized exchange. Card spending directly settles from on-chain assets. It also provides credit lines, where assets can be pledged as collateral.

However, users need to set up vaults, manage collateral, and monitor liquidation risks themselves, resulting in a high operational门槛. This limits the potential user base for this model.

During payment, the system converts on-chain assets to fiat currency in real-time for settlement, incurring on-chain Gas fees per transaction; when公链 throughput is insufficient or the network is congested, these fees can exceed the purchase amount, and transaction authorization delays occur frequently.

Therefore, MetaMask Card uses its own Layer 2 network, Linea, reducing single transaction Gas fees to about $0.01, alleviating the pain points of high fees and delays for small payments. Tria employs a gas-free top-up solution, where the platform covers the Gas fees incurred during topping up, sparing users the operational cost of choosing公链 and calculating fees.

But until the交互体验 balancing asset self-custody and刷卡便捷度 is polished to the level of traditional debit cards, this model's users will remain confined to native crypto users.

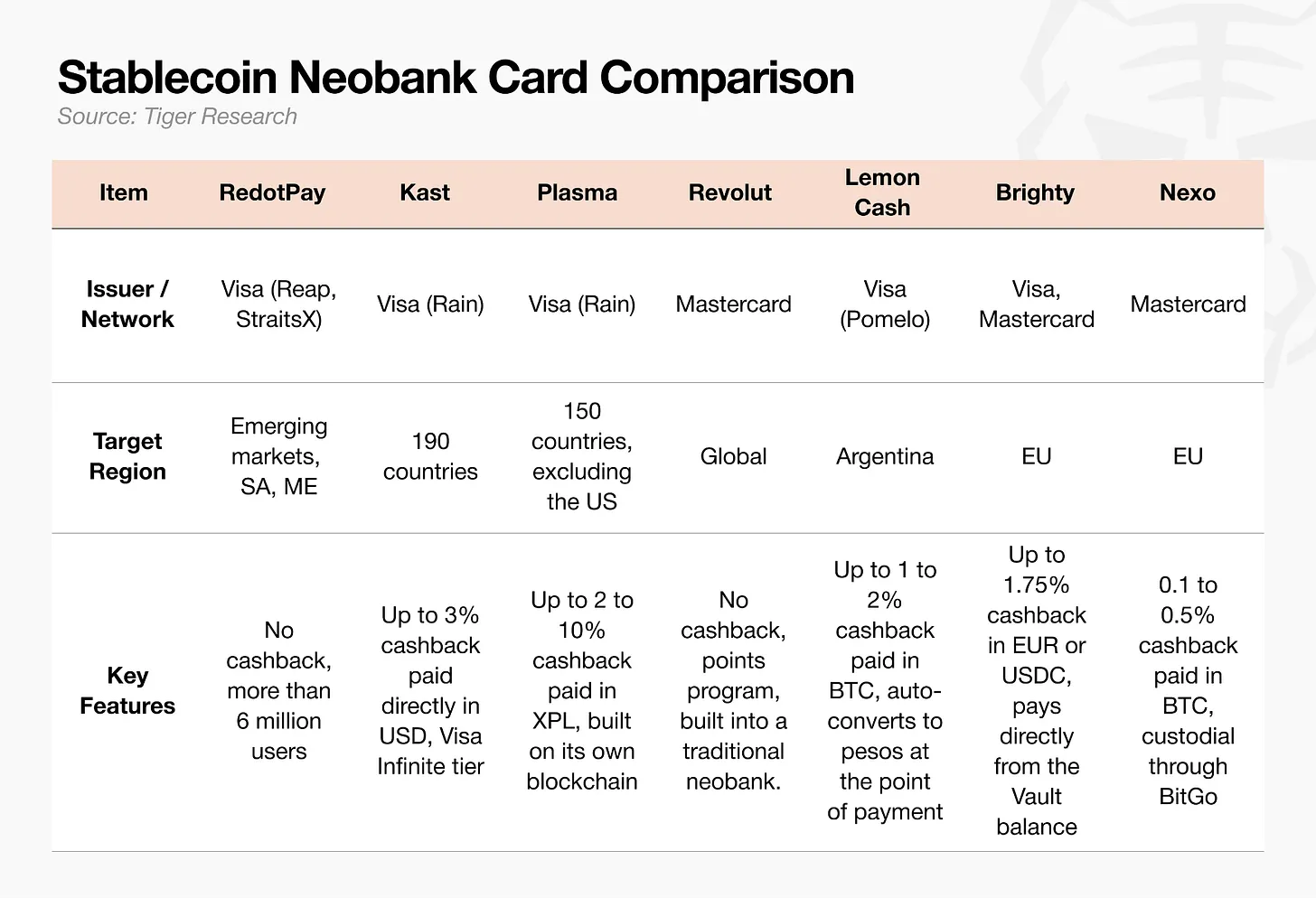

Stablecoin Digital Bank

This is the赛道 with the highest share of current market transaction volume. Its focus is on account functionality rather than the card itself. The stablecoin balance integrates foreign exchange, cross-border remittances, and wealth management features, with the payment card merely serving as the上层消费载体. In emerging markets with high local currency volatility, costly cross-border汇款, and difficult美元获取, this model possesses strong competitiveness.

To achieve sustained growth, this赛道 must move beyond the单一形态 of a "prepaid card," i.e., the model where users自行购买 stablecoins to top up their balance.

Cashback strategies have diverged according to market positioning. Industry leader RedotPay and established fintech player Revolut do not offer cashback promotions at all, while later entrants like Kast and Plasma One vigorously promote US dollar or platform token cashback to attract流量.

However, relying solely on福利补贴 cannot drive crypto payment cards to truly integrate into users' daily spending.

Single Payment Functionality Cannot Support Long-term Development

The history of traditional bank cards and digital banks proves that纯支付业务 has an extremely low profit ceiling. These businesses only became profitable after incorporating the concept of a primary account and structures like deposit and loan profits into their models. The crypto payment card industry has now reached the same developmental临界点. However, global regulatory rules like the US GENIUS Act and the EU's MiCA限制 stablecoin interest-bearing and asset management business development, making the path to突破 difficult.

Under these macro监管约束, players in the industry must抓住 three core strategies for long-term survival:

- Directly control the fund flow pipeline;

- Defend the unique application scenarios in emerging markets;

- Build their own user account system that cannot be replaced by underlying infrastructure providers.

Once industry standards mature, companies failing to achieve the above三点 will gradually fall behind.

Looking back at the development history of debit cards, those who最终占据 market dominance were not the ones issuing the most cards, but those who first controlled users' primary bank accounts. The crypto payment card industry now faces the exact same proposition.

Cryptocurrency card operators need to directly control the fund flow upstream of the Visa payment process, gain a foothold in细分市场, and, akin to the rise of bank accounts in traditional finance,掌控 consumer infrastructure. This means establishing a global standard with no precedent to follow.

Crypto payment cards that fail to achieve the above will never become a刚需工具 integrated into daily life. They will remain merely prepaid cards used by niche groups for small cashback benefits.