Author: Prathik Desai

Source: The Token Dispatch

Compiled and Edited: BitpushNews

Preface

Money has a fascinating way of narrating. Through its flow in the global markets, it silently reveals its perspective on the world.

In a confident market, money behaves like a 'talent scout.' It dares to take risks, willing to pay for a business plan, a prototype, or a future vision that seems far-fetched today. It expresses its belief by signing investment checks.

However, in an anxious market, money behaves more like a 'cautious auditor.' It gravitates towards what has already proven successful. Think of businesses with stable cash flows, large user bases, distribution channels, or strong teams.

There is a third scenario, somewhere in between. In this case, funds begin to 'recycle' existing ideas and jump between different hands. This happens when we see changes in business ownership through mergers and acquisitions (M&A), business unit restructuring, etc. In these scenarios, although funds are flowing, they are not creating new liquidity.

This is why anyone interpreting capital flows and financing data should be cautious. Large financing figures may signal fresh risk-taking, or they may merely mean that funds are 'changing hands' among existing businesses.

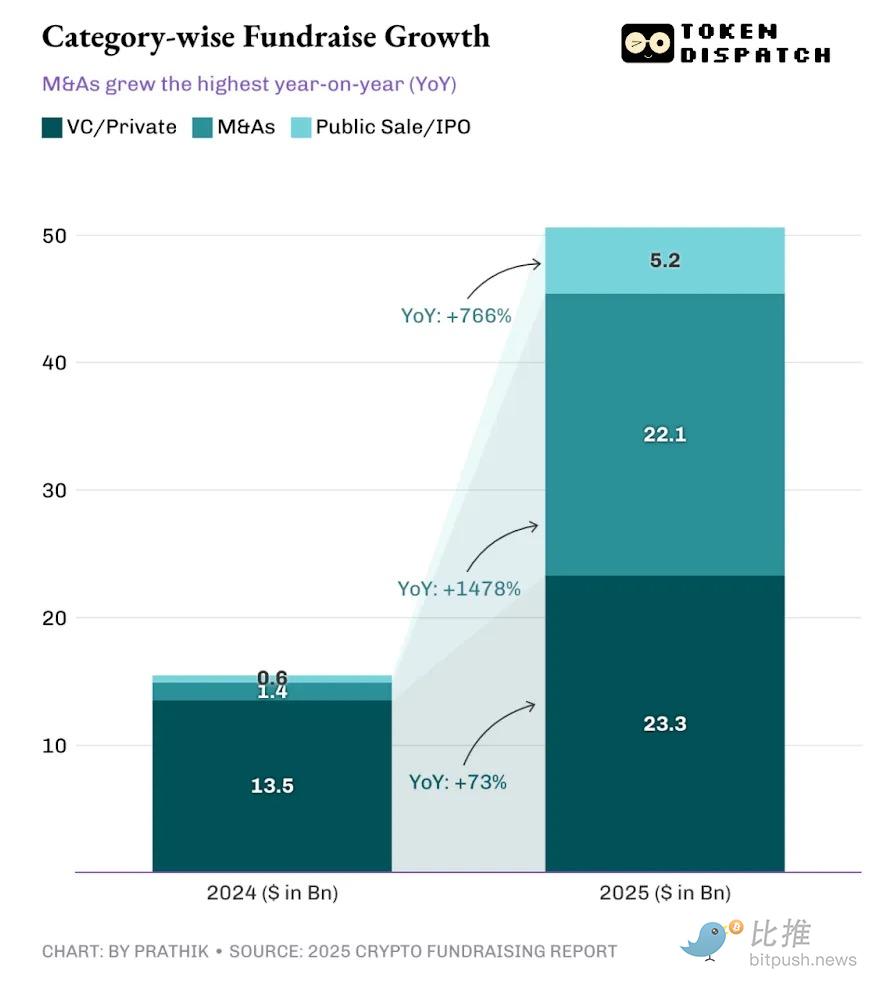

The '2025 Cryptocurrency Financing Report' disclosed such a number: In 2025, $50.6 billion was raised through 1,409 rounds of financing, an increase of over 200% compared to $15.5 billion in 2024. It sounds like a狂欢, but only by breaking down this number can we see the real picture.

This article will delve into this data and explain what last year's capital flows tell us about the direction of the crypto market.

Farewell to Storytelling: Giants Only Pay for 'Ready-Made Flywheels'

A significant portion of so-called 'fundraising' is not necessarily new money flowing into the crypto market. The financing report divides the total funds raised into several categories: venture capital (VC)/private equity, mergers and acquisitions (M&A), and public offerings/IPOs.

Last year, over 40% of the funds raised came from M&A, compared to only 9% in 2024. Although the total financing amount more than doubled from the previous year, 2025 was more a year of consolidation for the cryptocurrency industry.

The report interprets these numbers as 'moderate growth' in venture capital activity and an 'explosive growth' in M&A transactions. However, I believe there is more hidden behind these numbers.

In a relatively nascent industry like cryptocurrency, business consolidation may signify maturity and progress. But if accompanied by capital withdrawal from other channels, it may tell a completely different story.

In 2025, funds were not just shifting from funding new projects to acquiring existing ones. Although the total financing amount increased by $35 billion year-on-year, M&A and public offerings/IPOs accounted for $27 billion of this increase.

Venture capital (VC) activity still grew by over 70% year-on-year last year, although its share in the overall financing categories declined.

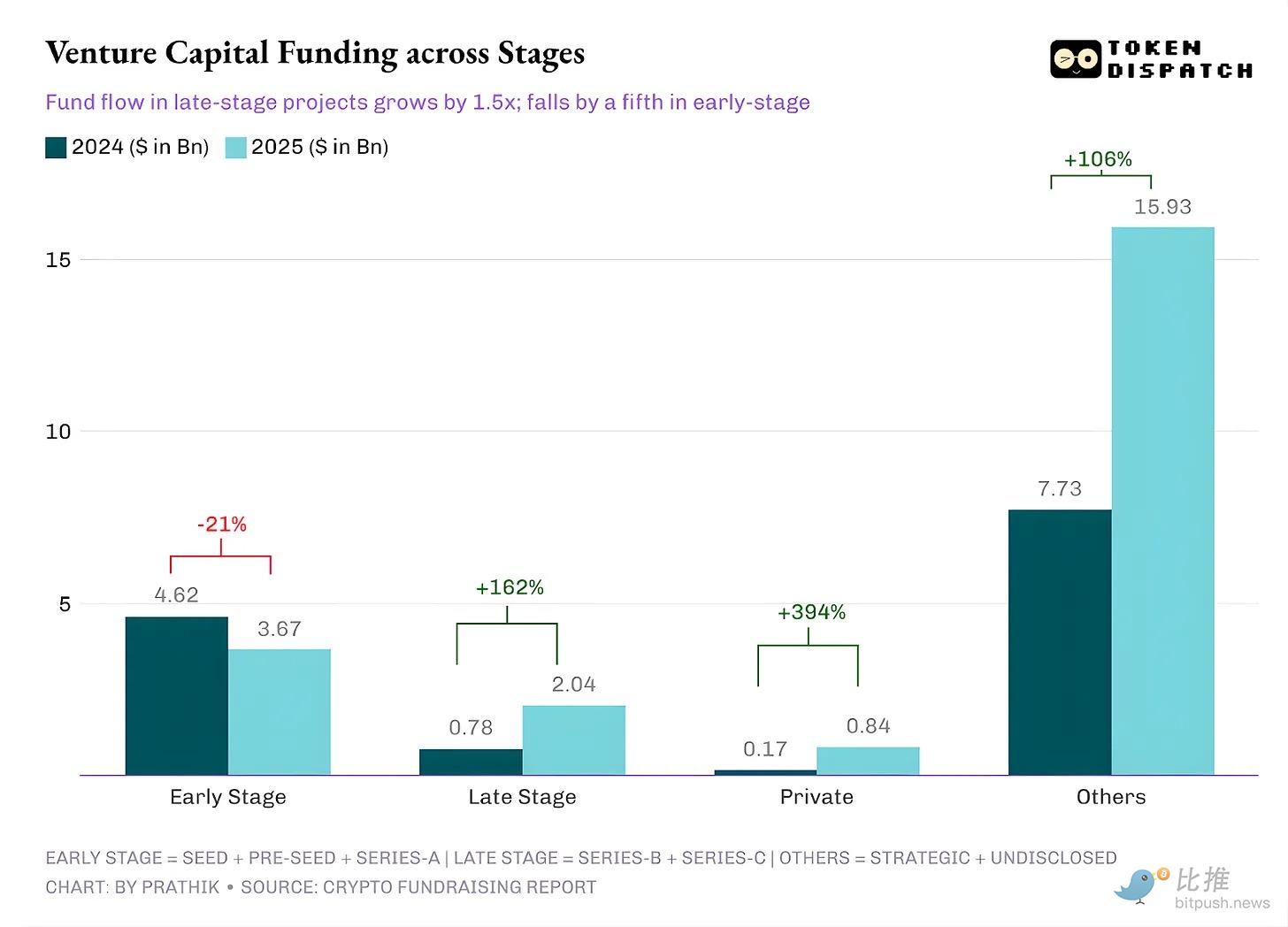

In 2024, VC accounted for over 85% of total financing, but by 2025, this proportion dropped to 46%. This, combined with how VC allocated funds to different stages of crypto projects last year, is precisely what worries the new generation of crypto developers and founders: In 2025, VCs signed far fewer checks, but for much larger amounts, aiming to fund existing projects in the later stages of their life cycle, rather than funding newer early-stage projects.

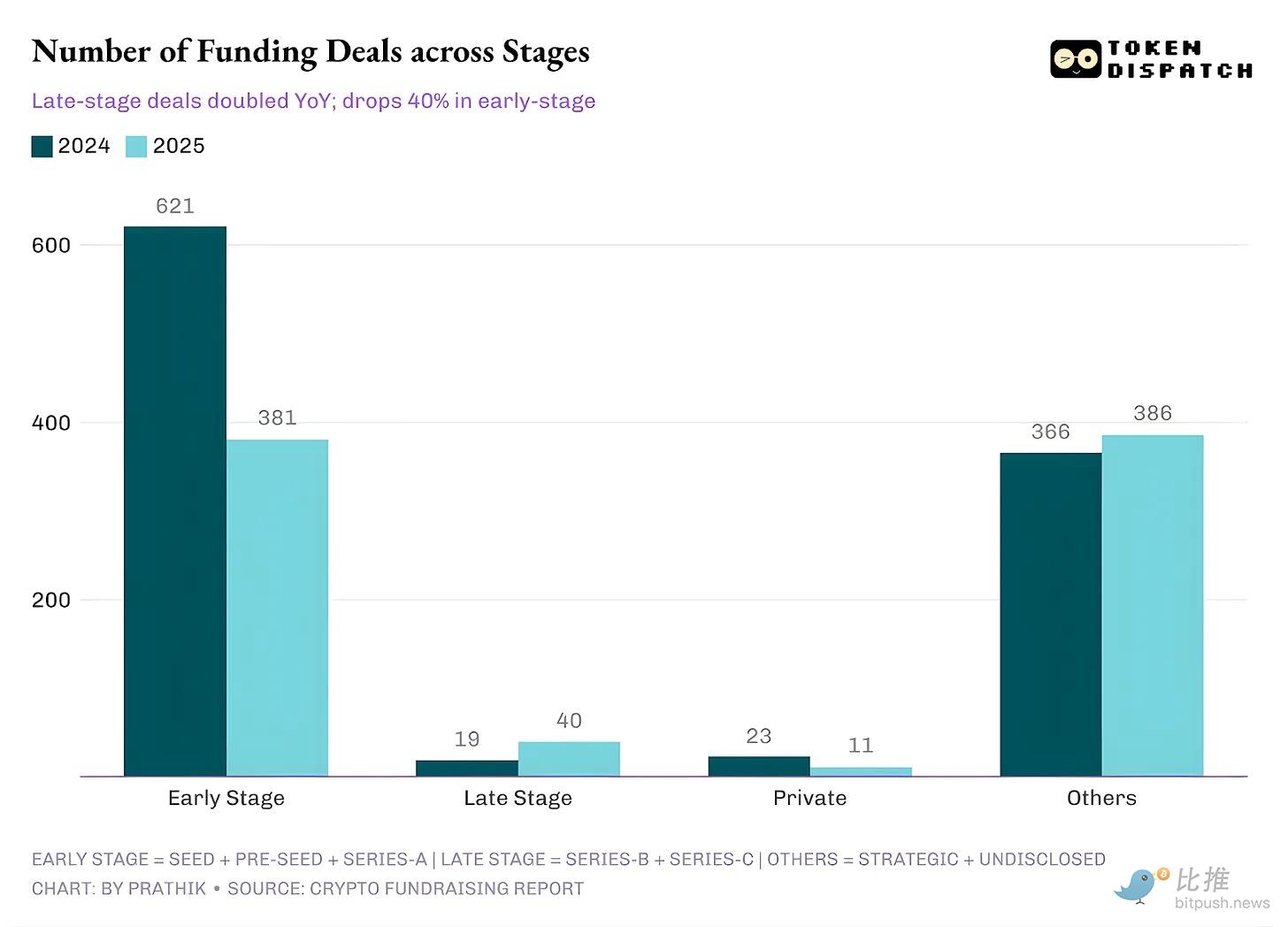

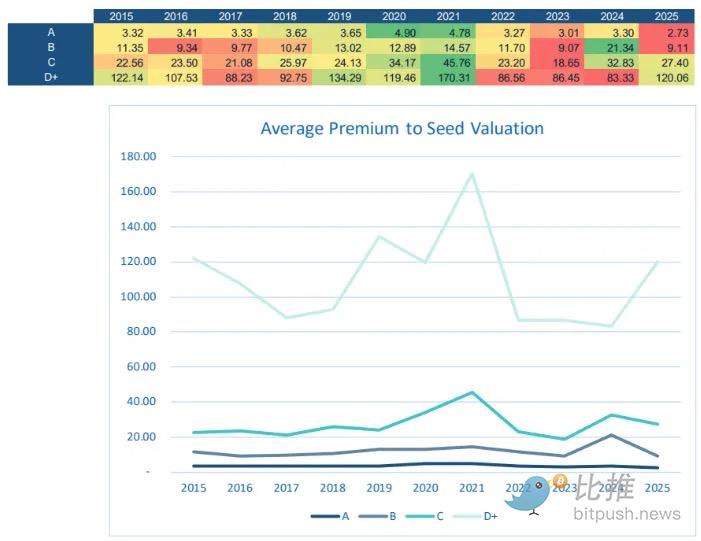

The data shows that Pre-Seed, Seed, and Series A financing decreased year-on-year, while Series B and Series C financing more than doubled in 2025. This behavior is also confirmed when looking at the number of checks signed across all financing stages.

The two charts above together tell us: "Yes, capital has increased. But it has increased in places with lower uncertainty. Founders' fundraising pitches are no longer about 'the future of money,' but about 'here are some ready-made metrics worth betting on.'"

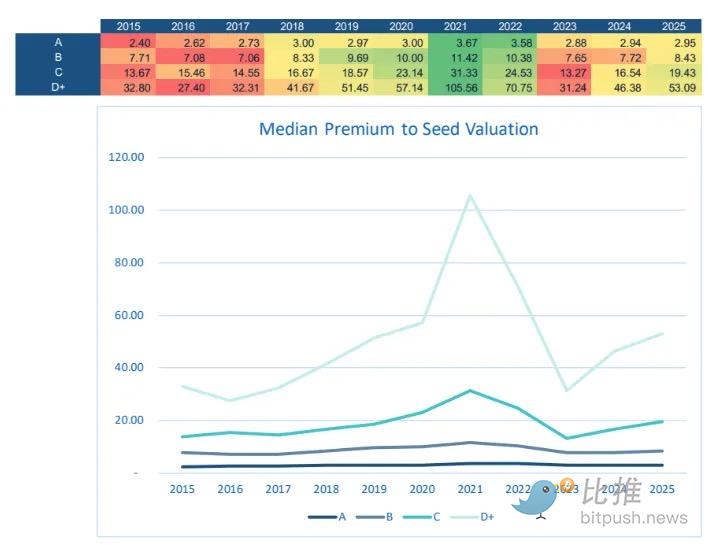

According to Equal Ventures' 'State of the Venture Economy Report,' while this portends fierce competition for early-stage founders, it may signal a value investment opportunity for investors seeking to inject funds into Series A and Series B projects.

This is because the competition to raise funds at the Seed and Pre-Seed stages has driven up valuation premiums. High valuation premiums mean investors are paying growth-stage valuation multiples for seed-stage risk profiles.

This shift prompts rational capital allocators to reallocate funds to lower-risk opportunities, such as Series A and B projects, which demand lower valuation premiums than Seed, Pre-Seed, Series C, and D+ rounds.

This, combined with the explosive growth in M&A transactions, shows how risk appetite has shifted across stages. On one hand, M&A accounted for over 40% of all 'funds raised,' which is inherently different from new funds injected through VC rounds. On the other hand, later-stage financing is favored because it appears easier to underwrite risk, offering greater certainty and higher potential return on investment (ROI).

When capital converges on specific tracks, two things naturally happen.

First, decision-making logic tends to focus. Entrepreneurs begin preparing for a more precise audience—a group focuses on similar metrics, shares industry insights with each other, and gradually forms a common evaluation language.

Second, the definition of a 'quality project' begins to converge. In the crypto field, this may mean extensive distribution networks, compliance resilience, enterprise-grade product readiness, and a business model that can operate independently without relying on bull or bear narratives.

This is why I am skeptical of the data in the '2025 Crypto Financing Report.' Although the amount of funds has increased, it is crucial to understand the drivers behind the explosive growth in M&A. Although cryptocurrency is a relatively new market, the technology stack has become very crowded, making it difficult to expand distribution channels.

In such times, it becomes a matter of course for existing giants to choose to buy and expand mature products rather than persuade users to adopt a new one. This was evident in last year's deals.

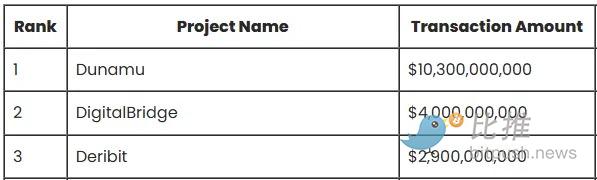

Take the top three M&A transactions listed in the report as examples: Dunamu, DigitalBridge, and Deribit. Their total value reached $17.2 billion, accounting for about 81% of the report's total M&A value.

Coinbase's acquisition of Deribit was not a bet on innovation or experimentation. This move was to leverage the flywheel Deribit had already built. Deribit provides a platform with ready-made liquidity, user habits, and options and derivatives products. Once the market matures, it can become the default trading venue for seasoned traders.Coinbase spotted the signal and prepared in advance.

South Korean internet giant Naver had a similar strategy when it decided to acquire Dunamu (operator of South Korea's largest cryptocurrency exchange Upbit) in an all-stock transaction worth $1.03 billion.This deal combines a massive consumer-grade distribution platform (an internet finance giant) with a regulated high-frequency financial product (an exchange).

What Does This Mean for 2026?

I expect the phenomenon of capital concentration to continue until we see clear exit paths. My only reservation regarding the report's 'consolidation' viewpoint is: Maturity does not necessarily have to mean the end of innovation. If too much capital is invested in rearranging ownership or doubling down on existing ideas, it could lead to stagnation and reduce breakthrough innovation.

If we fail to see successful IPOs and the reopening of large liquidity listing channels, expect later-stage investors to continue acting like strict underwriters, while early-stage founders will face a scarcity of attention.

But I don't think crypto seed rounds are dead.

2025 provided valuable lessons and clarity for early-stage founders. In 2026, they need to streamline their storytelling pitch decks and focus on the metrics the market values most. For example: how to have a distribution wedge, how to deliver products quickly while maintaining regulatory compliance, and how the product can survive robustly without the support of a bull market.

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Discussion Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush