Crypto activity in Brazil expanded sharply in 2025, with total transaction volume climbing 43% year over year as average investment per user crossed the $1,000 mark, according to a new report from crypto platform Mercado Bitcoin.

The report, titled “Raio-X do Investidor em Ativos Digitais 2025,” claimed that the Brazilian crypto market is no longer driven purely by speculation but increasingly shaped by structured investing and portfolio planning. The data was based on activity across Mercado Bitcoin’s platform, the largest digital asset exchange in Latin America.

Per the report, the average amount invested per person reached roughly 5,700 Brazilian reais, equivalent to more than $1,000. At the same time, 18% of investors allocated funds across more than one crypto asset, indicating a gradual shift toward diversification rather than single-asset bets.

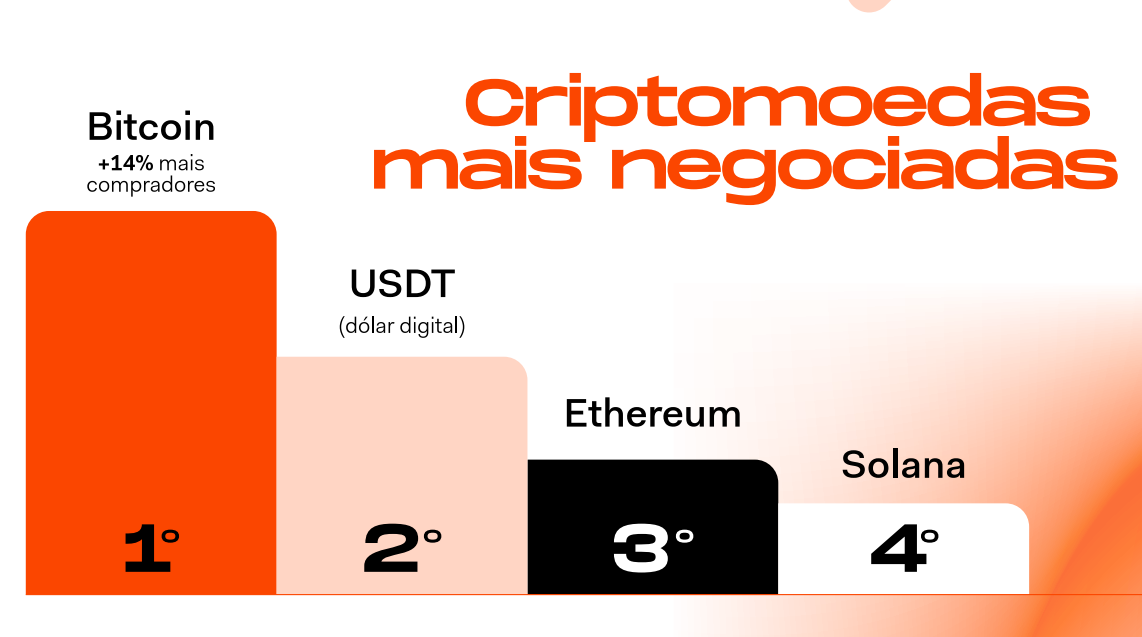

Bitcoin (BTC) remained the most traded asset, followed by the US dollar-pegged stablecoin USDt (USDT), Ether (ETH) and Solana (SOL), the report showed. Stablecoins also stood out as a key on-ramp for new and existing investors, accounting for roughly three times more transactions than in the prior year, as users sought lower volatility amid uncertain macro conditions.

Related: Brazilian stock exchange to launch tokenization platform and stablecoin

Brazil’s low-risk crypto products see 108% growth

The report revealed that lower-risk crypto products gained momentum in 2025. Digital fixed-income offerings, known locally as Renda Fixa Digital (RFD), recorded a 108% increase in investment volume, with Mercado Bitcoin distributing about $325 million to investors in 2025.

Demographics also shifted. Investors aged 24 and under posted a 56% increase year over year. However, Mercado Bitcoin noted that demand expanded across all age groups, including high-net-worth and institutional profiles.

Regionally, Brazil’s Southeast and South remained dominant by transaction volume, led by São Paulo and Rio de Janeiro, while states in the Central-West and Northeast gained visibility as crypto participation spread geographically.

Related: Solana enters Brazil’s main exchange as Valour expands regulated crypto access

Itaú Asset advises 1%–3% Bitcoin allocation

As Cointelegraph reported, Itaú Asset Management has recommended that investors allocate between 1% and 3% of their portfolios to Bitcoin, citing rising geopolitical risks, shifting monetary policy and ongoing currency volatility.

In a research note, strategist Renato Eid described Bitcoin as a distinct asset with its own return profile and a potential hedging role due to its global and decentralized nature, despite sharp price swings throughout 2025.

Magazine: 2026 is the year of pragmatic privacy in crypto — Canton, Zcash and more