Buried in Bitmine Immersion Technologies’ latest disclosure is a number that speaks to just how deep the company has gone on Ethereum.

Of the nearly 5 million ETH it now holds, 3.33 million is actively staked through its validator platform, generating more than $200 million in annualized staking revenue.

For a company built around accumulating a single digital asset, that income stream turns what might look like a speculative bet into something closer to an operating business.

The purchase that pushed those numbers higher came during the week of April 13 to April 19. Bitmine acquired 101,627 ETH in that period, its largest single-week buy since December 2025.

The transaction was disclosed Monday through a press release and a Form 8-K filing with the US Securities and Exchange Commission.

Source: SEC

Closing In On Target

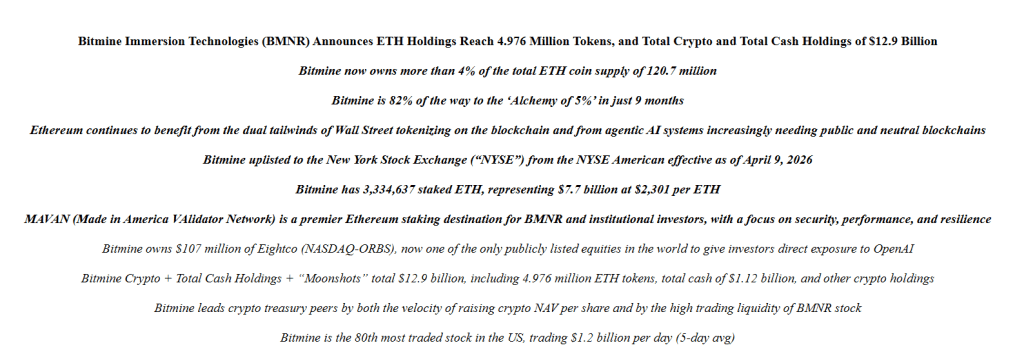

Following the purchase, Bitmine held 4,976,485 ETH — valued at roughly $11.5 billion based on a reference price of $2,301 per toke`n. That puts the company’s ownership at about 4.12% of total Ether in circulation.

Its stated target is 5%, a goal the company refers to internally as the “alchemy of 5%.” At the current pace, it is around 80% of the way there.

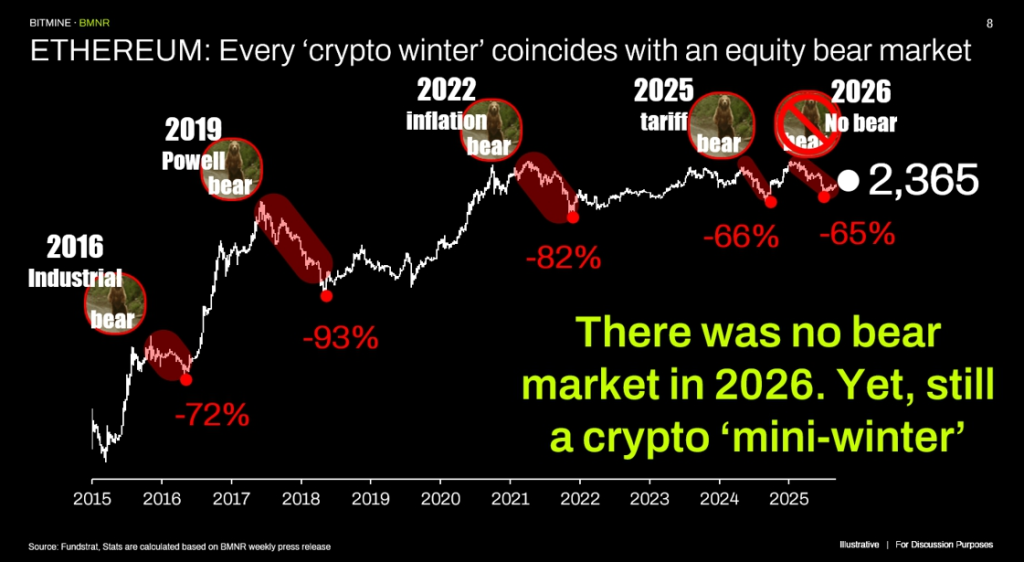

Chairman Tom Lee said the company has kept up an increased buying pace for four straight weeks. “Our base case ETH is in the final stages of the mini-crypto winter,” he said. Lee made similar remarks at Paris Blockchain Week 2026, where he predicted Ether could eventually top $60,000.

Source: Fundstrat

Beyond its ETH position, Bitmine also holds 199 Bitcoin, a $200 million stake in Beast Industries, a $107 million stake in Eightco Holdings, and $1.12 billion in cash. Total crypto and cash holdings stand at close to $13 billion.

NYSE Uplisting Came Before The Push

The buying acceleration follows a significant corporate move. Bitmine recently uplisted from the NYSE American to the New York Stock Exchange and expanded its share buyback program.

ETHUSD trading at $2,308 on the 24-hour chart: TradingView

The NYSE listing gives the company broader visibility among institutional investors at a time when crypto balance sheet strategies are spreading across public markets.

No other public company comes close to Bitmine’s total ETH exposure, according to data from CoinGecko, which tracks corporate Ethereum treasuries.

The gap between Bitmine and the next-largest holders has continued to grow with each successive purchase.

Featured image from Consensys, chart from TradingView