Author: Zhou, ChainCatcher

Since the end of last year, listed mining companies have set off a wave of collective sell-offs.

Cango sold 4,451 bitcoins in February, about 60% of its holdings; Bitdeer liquidated its entire bitcoin inventory in January; Riot Platforms sold multiple times in December and sold 3,778 BTC in the first quarter; Core Scientific also previously planned to sell about 2,500 bitcoins in the first quarter.

Recently, the leading mining company MARA disclosed in an announcement that in just three weeks from March 4 to 25, the company sold 15,133 bitcoins, cashing out over $1 billion. Simultaneously, the company announced a reduction of approximately 15% of its workforce as part of its strategic transformation into an energy and digital infrastructure company.

In fact, miners selling bitcoin is not new. In the bear markets of 2018 and 2022, mining companies also experienced large-scale liquidation and capitulation, and those that remained were the more efficient players. But this time, the trigger for the sell-off is not just the falling coin price; they also have a new destination—AI data centers.

I. The Triple Motives Behind the Sell-Off

On the surface, it appears to be a collective sell-off by mining companies, but upon closer inspection, their underlying motives are not uniform and can be roughly divided into three distinct types of selling logic.

Mining Itself Has Fallen into Loss

The first, and most direct, motive: cost pressure.

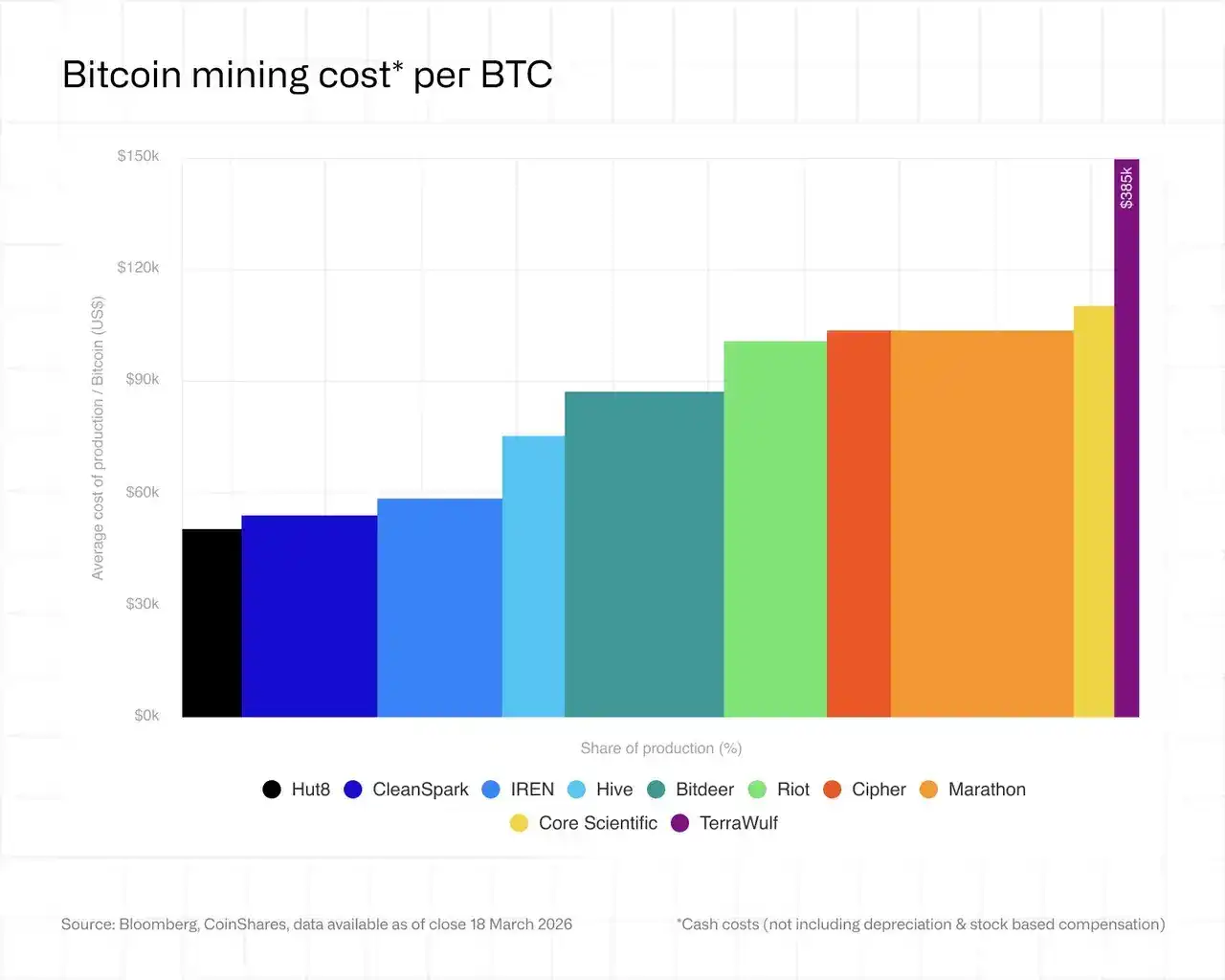

The latest mining report from CoinShares shows that the weighted average cash cost for listed mining companies to mine one BTC is currently about $79,995, while the BTC market price hovers between $68,000 and $70,000, resulting in an average loss of nearly $19,000 per coin, putting the industry in a state of approximately 21% loss overall.

This is no longer just a matter of narrowing profit margins, but a question of whether cash flow can sustain continued mining.

The report also shows that the hash price fell to a historical post-halving low of $28 to $30/PH/day in early March. At this level, most active mining rigs need electricity prices to be压到 below $0.05/kWh to maintain cash profitability. Currently, about 15% to 20% of the network's mining rigs are on the edge of breakeven.

Meanwhile, tensions in the Middle East are pushing up energy prices, putting continuous pressure on electricity costs, an external variable that mining companies themselves have little control over.

QCP Group pointed out in a report that with the bitcoin price significantly below the average mining cost, mining companies are under obvious pressure, and liquidity priority has surpassed the HODL strategy.

Against this background, for some mining companies, selling bitcoin is a practical necessity to maintain operations.

AI Offers a More Stable Revenue Logic

The second motive is more strategic and the most值得深究 part of this sell-off.

Bloomberg analysis pointed out that unlike previous sell-offs to cover costs, the funds from this round are being reallocated to the artificial intelligence sector.

The business logic behind this is clear: mining revenue is highly dependent on coin price, hash rate difficulty, and electricity price, making it extremely volatile. In contrast, AI infrastructure is closer to long-term leases, with CoinShares' report指出其利润率可达 80% to 90%, and revenue is predictably long-term.

More crucially, mining companies already hold ready-made resources—cheap power contracts, built data centers,完善的散热系统, and mature operations teams.

Some analysts point out that the construction cost of Bitcoin mining infrastructure is about $700,000 to $1 million per megawatt, while AI infrastructure costs as much as $8 million to $15 million per megawatt. This huge cost gap is being monetized on a large scale by mining companies.

Notably, behind this transformation stands a group of unexpected drivers—tech giants and traditional financial institutions.

Previously, Google provided credit support for the lease obligations of the AI cloud platform Fluidstack, with disclosed credit support累计 exceeding $5 billion,先后为 TeraWulf, Cipher Mining, Hut 8 and other mining companies' AI transformation提供担保并换取相应股权; Microsoft signed a five-year, $9.7 billion AI cloud services contract with mining company IREN; Morgan Stanley provided a $500 million loan to Core Scientific, with a potential total credit line of $1 billion.

Their entry provides far more solid capital endorsement for this transformation than imagined.

Meanwhile, mining companies like Core Scientific, TeraWulf, Hut 8, and Cipher have successively signed large AI/HPC contracts, with cumulative amounts exceeding $70 billion. The CoinShares report mentioned that mining companies with AI/HPC contracts have valuation multiples approximately twice those of pure mining companies, and the market is rewarding those who complete the transformation first with valuation premiums.

Even the most financially sound mining companies with the lowest leverage, like HIVE, have actively scaled back mining operations and turned to expanding AI data centers. This indicates that the pressure to transform is no longer exclusive to highly indebted mining companies but is a directional choice facing the entire industry.

Actively Using BTC as a Financial Tool

The third logic is relatively精明 and the most proactive.

Some mining companies choose to sell BTC not due to operational pressure but to use it as a tool to optimize their balance sheets, like MARA. The specific operation is: use the proceeds from the sale to repurchase previously issued convertible bonds at a discount below par value, thereby compressing the scale of liabilities and reducing potential equity dilution risks.

For these mining companies, the role of BTC on the balance sheet has quietly changed from a long-term holding象征信仰 to a strategic asset that can be flexibly allocated.

Additionally, a relatively rare type of seller has emerged in this round of sell-offs: sovereign nations.

On-chain data shows that the BTC holdings of the Royal Government of Bhutan have decreased by about 66% from the peak at the end of 2024, with the single transfer size in March rising to $35 million to $45 million, and the pace of selling持续加快.

Unlike most countries that accumulate BTC through market purchases, Bhutan's holdings come from its domestic hydroelectric mining operations. This large-scale reduction may be related to the funding needs of its national development projects. This is also one of the largest government bitcoin reduction actions on record.

The叠加 of three logics—mining losses, AI transformation, debt optimization—plus selling pressure at the sovereign level—means the market is承受 structural supply pressure from multiple directions and of varying nature. The Bitcoin faith of mining companies is being reshaped by more realistic business logic.

II. After Leaving, Each Goes Its Own Way

Of course, selling off does not mean completely liquidating positions. The remaining holdings and subsequent strategies of various mining companies are showing截然不同的分化.

Three Paths, Three Choices

The first path:坚守挖矿.

Represented by CleanSpark and HIVE. They do not chase the AI transformation narrative, do not叠加 debt, and rely on a combination of low electricity prices, new-generation矿机, and low leverage to seek victory in the industry's liquidation process. Their logic is that as high-cost capacity gradually withdraws, the per-unit hash rate收益 for remaining mining companies will increase accordingly.

CleanSpark has publicly stated that继续大规模投入比特币挖矿"在经济上已不太合理" at the current hash price level, but the company still chooses to stick to its main business, betting that the cycle will eventually reverse.

Well-known crypto KOL蓝狐 pointed out that historically, almost every halving has been followed by miner capitulation, and those who remain are often the more efficient players, securing a larger share in the next rebound.

For these companies,坚守挖矿 is not stubbornness but trust in the laws of the cycle.

The second path:两条腿走路.

Represented by MARA, IREN, and Riot. They retain a considerable规模 of BTC holdings while simultaneously布局 AI/HPC, using the relatively stable income from AI business to hedge against the cyclical fluctuations of mining income.

These companies are essentially solving an asset allocation problem. The answers vary by company, but the core logic is that the two business lines support each other,分散单一风险.

The third path:全面转向 AI.

Represented by Core Scientific, TeraWulf, and Cipher. BTC holdings have exited the position of core assets, and mining is gradually becoming an附属部分 of the data center business.

CoinShares predicts that by the end of 2026, the AI revenue share of some mining companies could be as high as 70%, while the mining revenue share may drop from about 85% in early 2025 to less than 20%. These companies are nominally still mining companies, but in essence, they are becoming AI infrastructure operators that started with mining.

The potential risk of this path is that a heavy-asset transformation意味着巨额债务负担. Once AI demand cools down, both businesses will be under pressure.

也有观点指出, the credit guarantee structure provided by Google through Fluidstack actually creates highly concentrated counterparty risk—the entire cash flow chain relies on Fluidstack as an intermediary. Once the AI lease market experiences major changes, this structure could become a single point of failure.

BTC Price Determines Their Fate

No matter which path is chosen, it ultimately points to the same variable: the direction of the BTC price.

CoinShares gives three scenarios:

● If BTC recovers to $100,000 by the end of 2026, the hash price will rebound to about $37/PH/day, mining profits will be repaired, and overall industry pressure will ease;

● If it remains below $80,000, high-cost miners will accelerate their exit, and the traditional model of mining and HODLing等待牛市 will become increasingly difficult to sustain;

● If it breaks through the historical high, the hash price could soar to $59/PH/day, and the industry will enter a new expansion cycle.

Conclusion

Overall, mining companies face two ultimate outcomes: either the coin price recovers, they return to their main business, and everything now is just a cyclical historical footnote; or the price remains low for an extended period, more and more mining companies complete their transformation into AI data centers, and the company model of mining and HODLing等待牛市 becomes increasingly rare in this industry.

However, there is another question worth asking beyond the business logic of this transformation. Mining companies are not ordinary listed companies; the continuous investment in hash rate is itself the security budget of the Bitcoin network.

Sazmining CEO Kent Halliburton once直言, these companies "hold power contracts, land, and infrastructure, yet hand these resources over to Microsoft and Google in exchange for rent checks, transforming from protecting the Bitcoin network to保管机架空间 for hyperscale cloud providers."

When mining no longer generates sufficient economic returns, the rational business decision is naturally to转移资源; but if this trend continues to spread, who will bear the long-term cost of maintaining the security of the Bitcoin network will become a problem that cannot be ignored.

History may have given an answer to this question.

The Bitcoin network has experienced several large-scale miner liquidations, and each time之后, it has operated with higher efficiency.

But this time, the miners who are leaving are not just turning off their machines.

The times have changed.