Written by: Protos

Compiled by: Chopper, Foresight News

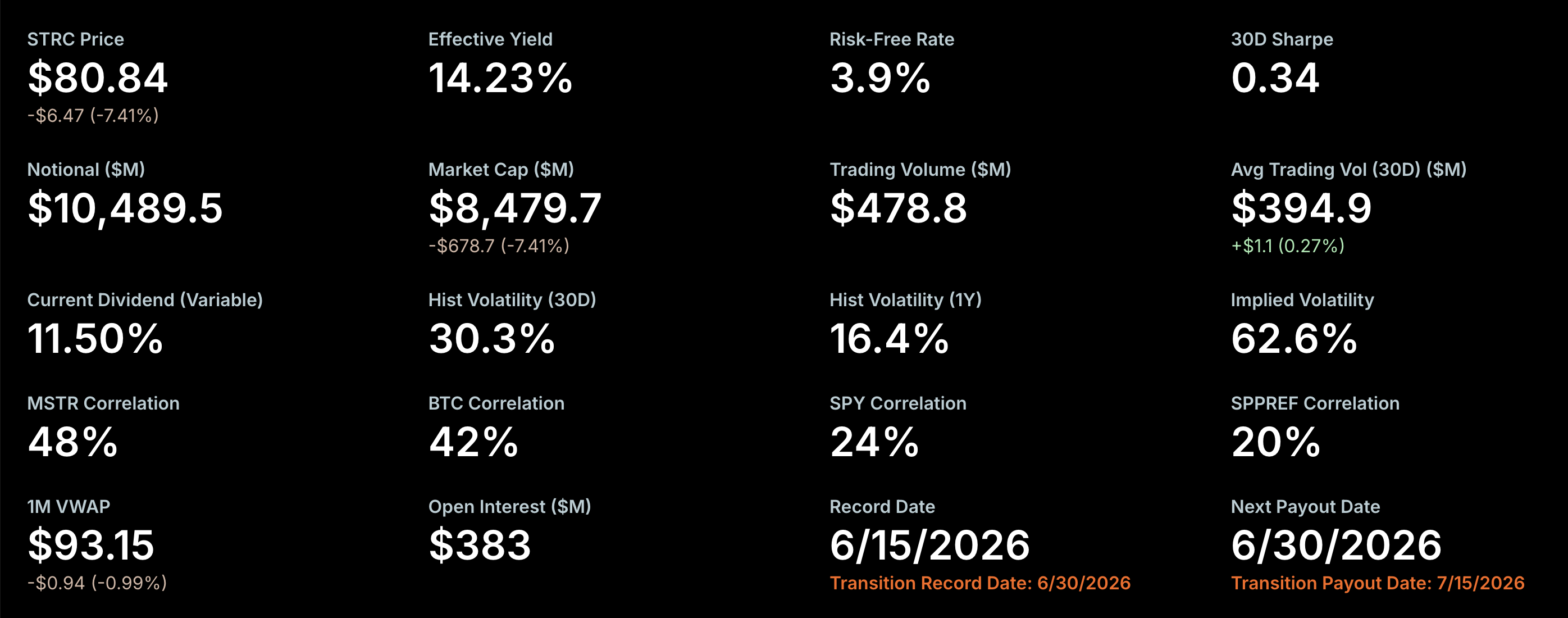

STRC is a dividend-paying stock issued by Strategy (formerly MicroStrategy), the Bitcoin reserve company led by Michael Saylor. Its latest closing price has fallen to $80.84.

That number was supposed to be $100.

STRC Price Panel, Source: Strategy Website

Saylor places great importance on STRC maintaining a trading price at its $100 par value. With just one week left until the dividend snapshot date, he hopes to pull the stock price back to the $100 mark before then.

The company's filing with the U.S. Securities and Exchange Commission (SEC) clearly states: Strategy "aims to stabilize the trading price of STRC shares near the par value of $100 per share."

But the reality is, the current stock price is at a discount of about 20% to its par value.

More critically, the company's data panel reveals another severe crisis: As of yesterday's Nasdaq close, STRC's June monthly Volume-Weighted Average Price (VWAP) was $94.09, falling below the company's set red line of $95. According to internal rules, once this threshold is triggered, the dividend increase must be at least double the regular standard.

Based on the internal dividend mechanism, if the final June monthly VWAP closes below $95, the next STRC dividend increase cannot be lower than 0.5%. Under normal circumstances, since its listing, STRC's dividend increase per dividend registration cycle has been only 0.25%.

This means if secondary market funds do not actively enter to boost the stock price, the current 11.5% annualized dividend yield will most likely be raised to 12% in the next dividend registration cycle in mid-July. If Strategy's board wants to adopt a more aggressive strategy, their rules allow them to grant a higher increase at their discretion.

Can a 12% High Dividend Pull the Stock Price Back to $100?

Even if a 12% ultra-high dividend has the potential to attract buying interest, the current stock price of around $80 still has a huge gap to reach $100.

First, investors need to hold the stock for an entire year to receive this expected 12% dividend, and the dividend will be split into 24 bi-monthly capital return payments, each distributing only 0.5%. Second, the board can lower the dividend standard at any time during the year.

Furthermore, the STRC stock price itself still carries the risk of continued decline.

Ultimately, investing in STRC relies entirely on market expectations, with no guaranteed returns. The company's board can modify or suspend the dividend policy at any time, and this so-called "standardized dividend mechanism" has no legal binding force. The company's public disclosure documents repeatedly caution: cash dividends are not promised and there is a possibility of sudden reductions or direct suspension; meanwhile, the company provides no guarantee for the secondary market price of STRC, and the stock's current performance remains persistently weak.

Four Other Feasible Means to Boost the Stock Price

Apart from significantly raising the dividend, Strategy has four other tools to restore market confidence, but their implementation is relatively unlikely and their effectiveness limited.

First, the company could directly repurchase STRC shares in the secondary market.

Rules allow the company to buy back its own shares on the Nasdaq exchange, but it has never conducted repurchase operations, nor has it indicated any intention to do so. On the contrary, the original purpose of Strategy issuing STRC was to sell shares to raise funds and increase Bitcoin holdings, not to support the stock price through buybacks.

Second, Strategy might announce a suspension of issuing STRC at prices above $100.

Strategy's supplemental filing from last November shows plans to continuously issue new STRC in the range of $99 to $101, with the actual issuance price basically locked at $100.01. Continuous issuance dilutes the float, essentially placing a natural ceiling on the stock price, as speculative buying interest weakens significantly when the price approaches $100. If the company suddenly announced a halt to dilutive issuances around $100.01, this unexpected move might temporarily boost market sentiment.

Third, the company could signal long-term stable dividend-paying capability to the market by selling ordinary shares and continuously accumulating US dollar cash.

In recent weeks, Strategy has already used this method, selling MSTR ordinary shares and adding hundreds of millions of dollars to its cash buffer, but with little effect. Currently, the company's dollar reserves are only $1.4 billion, a scale insufficient to reassure STRC shareholders to hold on.

Fourth, Strategy might announce a benefit that surprises STRC shareholders.

A public company's board has the authority to distribute one-time special dividends or shareholder perks, creating positive surprises. For example, company CEO Phong Le purchased $1 million worth of STRC this week. Although the amount is negligible compared to his annual compensation, it still counts as a small positive signal. If the board introduced more creative shareholder benefits, it might reverse the current bearish market sentiment.

Historically, STRC has also rebounded against the trend and stabilized above $100. According to a Protos report last October, at that time, the company fully delivered dividends, raised the dividend to 10.25%, and suspended selling STRC through the ATM issuance channel since July. Multiple positive factors resonated, pushing the stock price back to $100 for the first time. Before that dividend registration date, many investors were willing to enter at $100.

Judging from its historical performance, STRC has the full potential to return to $100. The only question is: How much cost is Strategy willing to bear to attract funds to buy in?