Recently, according to The Wall Street Journal, the two leading prediction market platforms, Polymarket and Kalshi, have been in talks with potential investors for funding rounds, each with an estimated valuation of around $20 billion. In November 2025, it was reported that Polymarket was negotiating funding at a $12 billion valuation. That December, Kalshi completed a $1 billion funding round, bringing its valuation to $11 billion.

In just a few months, the valuations have nearly doubled again.

According to public market data and industry reports, as of the end of February 2026, the cumulative nominal trading volume of the global prediction market reached $127.5 billion, with Polymarket leading at $56.07 billion and Kalshi at $44.71 billion, together accounting for 79% of the market share.

While leading in cumulative trading volume, Kalshi showed more outstanding growth in 2025, not only reversing its market share from a minority position at the beginning of the year to over 60% but also driving its monthly active users (MAU) from 600,000 to over 5.1 million, demonstrating a faster pace of scale expansion. In contrast, Polymarket, leveraging its crypto-native advantages, maintained its global event coverage and cumulative trading lead, but its user growth was relatively steady, with peak MAU hovering around 700,000. The two core metrics—trading volume and MAU—clearly outline Kalshi's explosive catch-up and Polymarket's sustained深耕 (deep cultivation), forming a duopoly in the prediction market.

Specifically regarding trading volume performance, Kalshi's growth trajectory shows a leap from a low base to a high volume.

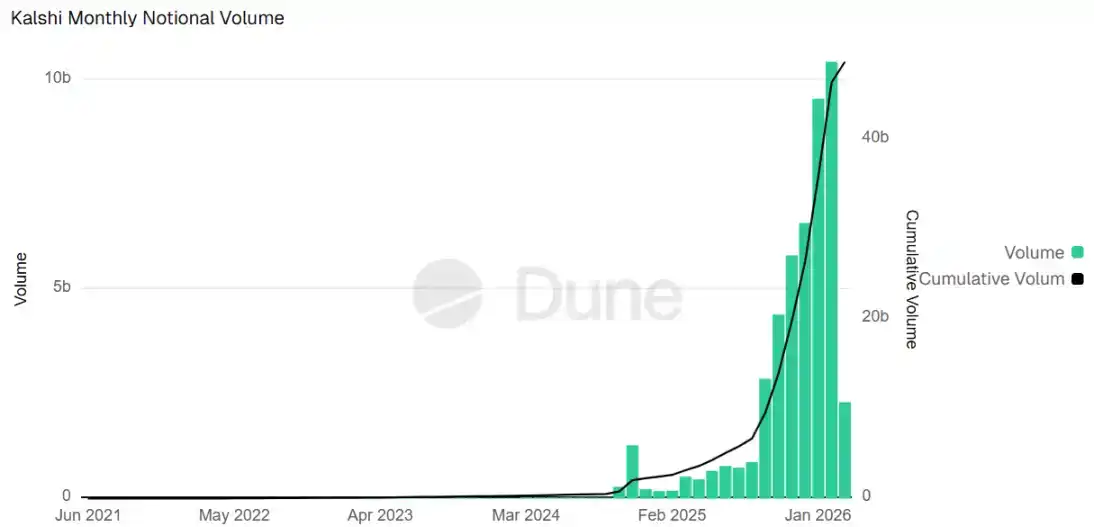

In 2024, Kalshi's annual nominal trading volume was approximately $1.9 billion, limited by early regulatory frameworks and market awareness, primarily driven by a few events. Entering 2025, this number surged to about $23.8 billion, a year-on-year increase of over 1100%. This explosion was directly reflected in monthly and weekly records: September single-month trading reached $2.86 billion, October further climbed to $4.39 billion, and December skyrocketed to $6.58 billion. The strong momentum continued into the beginning of 2026, with January's monthly trading exceeding $10.4 billion.

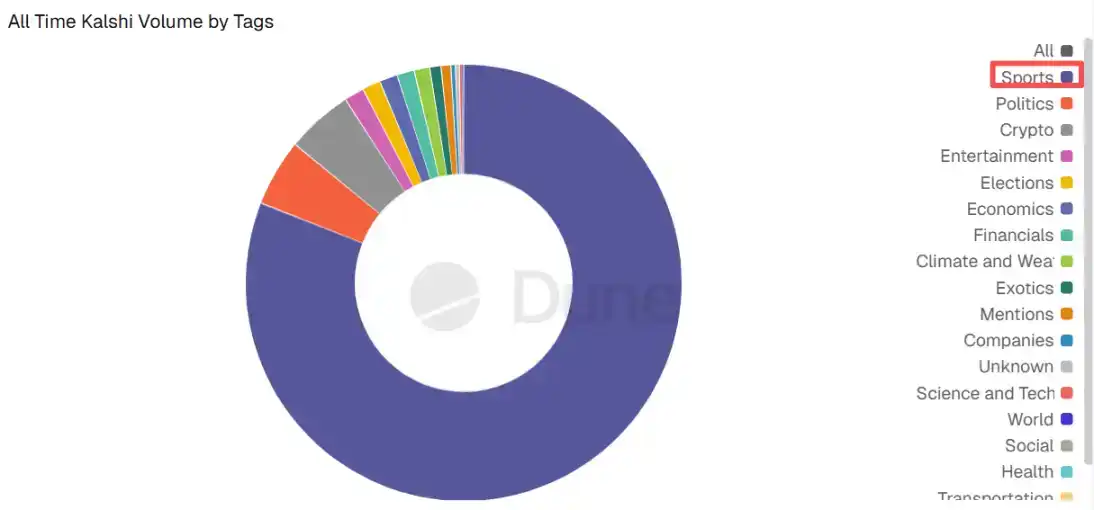

Sports event contracts contributed about 81% of this trading volume.

As of March 9, Kalshi's cumulative total trading volume exceeded $48.6 billion. Currently, its open interest hovers around $500 million.

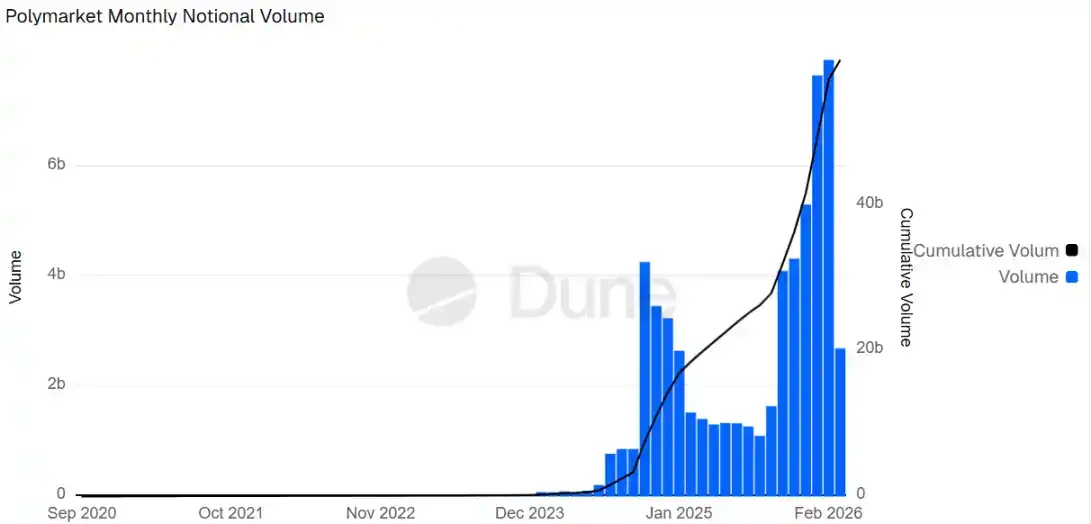

Polymarket's trading volume reflects its earlier accumulation advantage and later steady maintenance. Dune Analytics data shows that in 2024, Polymarket's monthly nominal trading volume experienced explosive growth, reaching a historical high of $4.266 billion in October 2024, bringing its cumulative trading volume to $7.6 billion.

Subsequently, although its monthly trading volume slowly declined, it remained at a high level. The turning point occurred in September 2025, when Polymarket began its pulse-like surge in trading volume.

October single-month trading broke $4.1 billion, November broke $4.3 billion.

By 2026, in January alone, its trading volume broke $7.658 billion, and February broke $7.9 billion. As of March 9, its cumulative trading volume exceeded $59.9 billion.

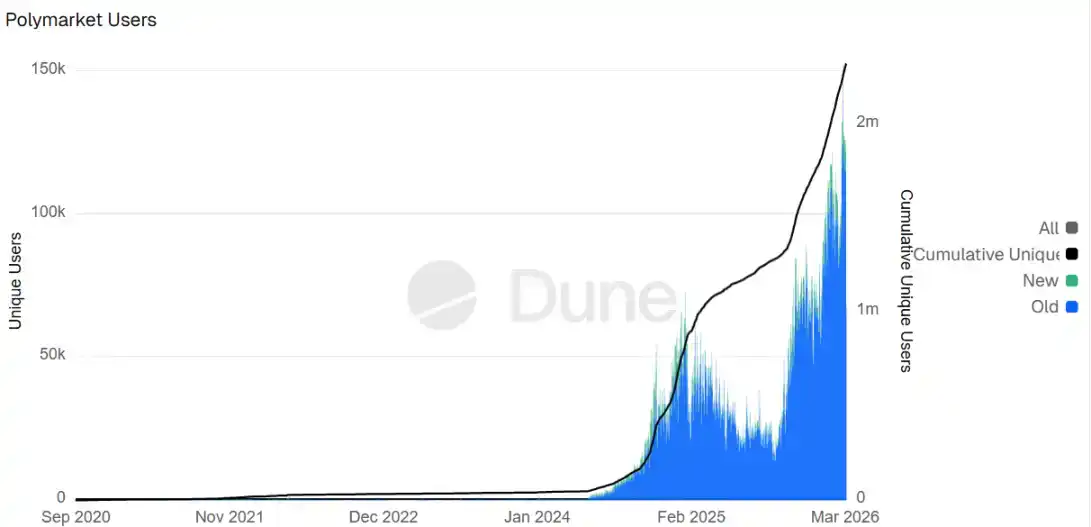

According to Dune data statistics, its total number of users has skyrocketed from 40,000 in 2024 to 2.31 million today.

It is worth noting that Polymarket still holds an advantage in liquidity depth for political and crypto events, with some weekly transaction counts accounting for up to 57%, but its overall market share dropped from 95% to 35-40% in mid-2025 before gradually stabilizing.

The divergence in trading volume data between the two platforms essentially stems from differences in business focus and user access models. Kalshi, as a CFTC-regulated entity, focuses on compliant trading in USD, covering over 42 US states. Kalshi gains the upper hand in sports dominance, while Polymarket maintains a lead in political and crypto domains, jointly pushing the entire market's weekly nominal trading volume to stably remain in the tens of billions of dollars.

In terms of ecosystem partnerships, the two major prediction markets are also frequently active, deeply integrating with mainstream institutions, media, and sports IPs. Both are not only opening offline pop-up shops but also expanding疯狂 (frantically) online.

Kalshi focuses on leveraging its compliance advantages, forming a strategic partnership with Tradeweb and receiving a minority equity investment, embedding real-time probability data into its institutional trading platform; Robinhood became its largest traffic source, contributing over 50% of trading volume in the second half of 2025; simultaneously, it secured exclusive media partnerships with CNBC and CNN, with data directly integrated into programs and reports.

Polymarket, on the other hand, emphasizes Wall Street data output and entertainment penetration. In June last year, Polymarket partnered with X, becoming its official prediction partner. It secured a strategic investment of up to $2 billion from ICE, which incorporates the data into financial product streams. In November, Polymarket reached a multi-year exclusive agreement with TKO Group, becoming the official prediction market partner for UFC and Zuffa Boxing, with data integrated into broadcasts and live events.

In January 2026, Polymarket entered an exclusive partnership with Dow Jones-owned media, providing prediction market data to media outlets including Barron's and The Wall Street Journal.

Interestingly, both are official NHL prediction market partners. Additionally, Google has integrated data from both into its search and finance platforms.

Overall, judging from the trading volume and MAU data over the past two years, both are jointly driving the evolution of prediction markets from niche tools into mainstream information and risk management platforms. This trend is not only reshaping the valuation logic of the crypto industry but also providing real-time signal references for traditional finance. If subsequent funding rounds materialize, coupled with热门 (hot) geopolitical events (US-Iran conflict), World Cup tournaments, and the eve of the US election, various data points for both platforms in 2026 are expected to break historical records.