Author: Artemis Analytics

Compiled by: Deep Tide TechFlow

Deep Tide Introduction: Robinhood Chain has surged to the third spot in DEX trading volume just one month after its launch, but its wallets are filled with animal-themed coins and shitcoins. A longtime shareholder who invested in Robinhood back in 2019 is sounding the alarm: Don't repeat the mistakes of the 2021 meme stock frenzy. Tokenized stocks are the right path to break $10 billion in revenue by 2030 and serve 100 million global users.

Dear Vlad and Johann:

Robinhood Chain has had a fast start in "democratizing finance for all" less than a month after launch:

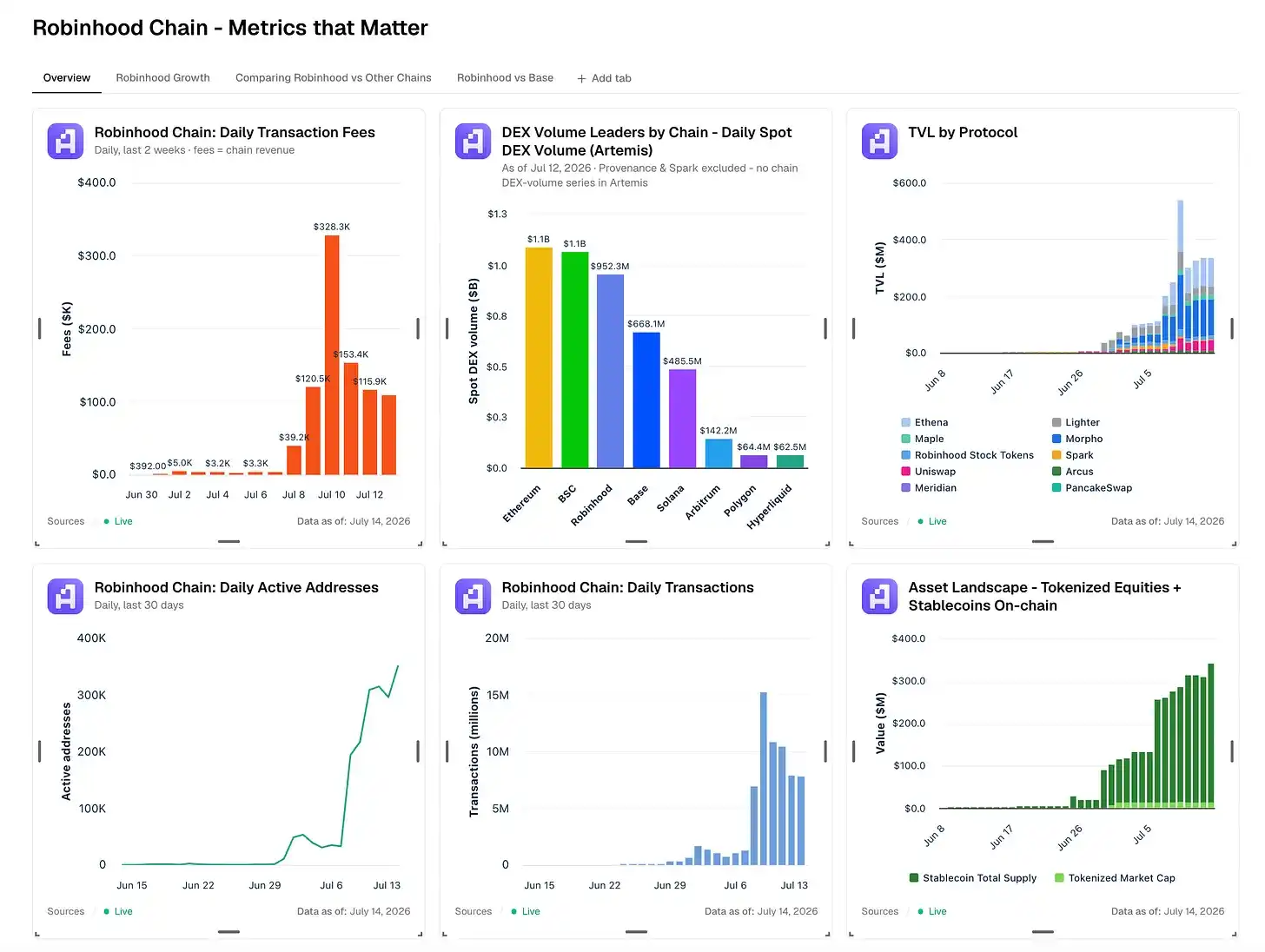

- Over 300,000 daily active addresses

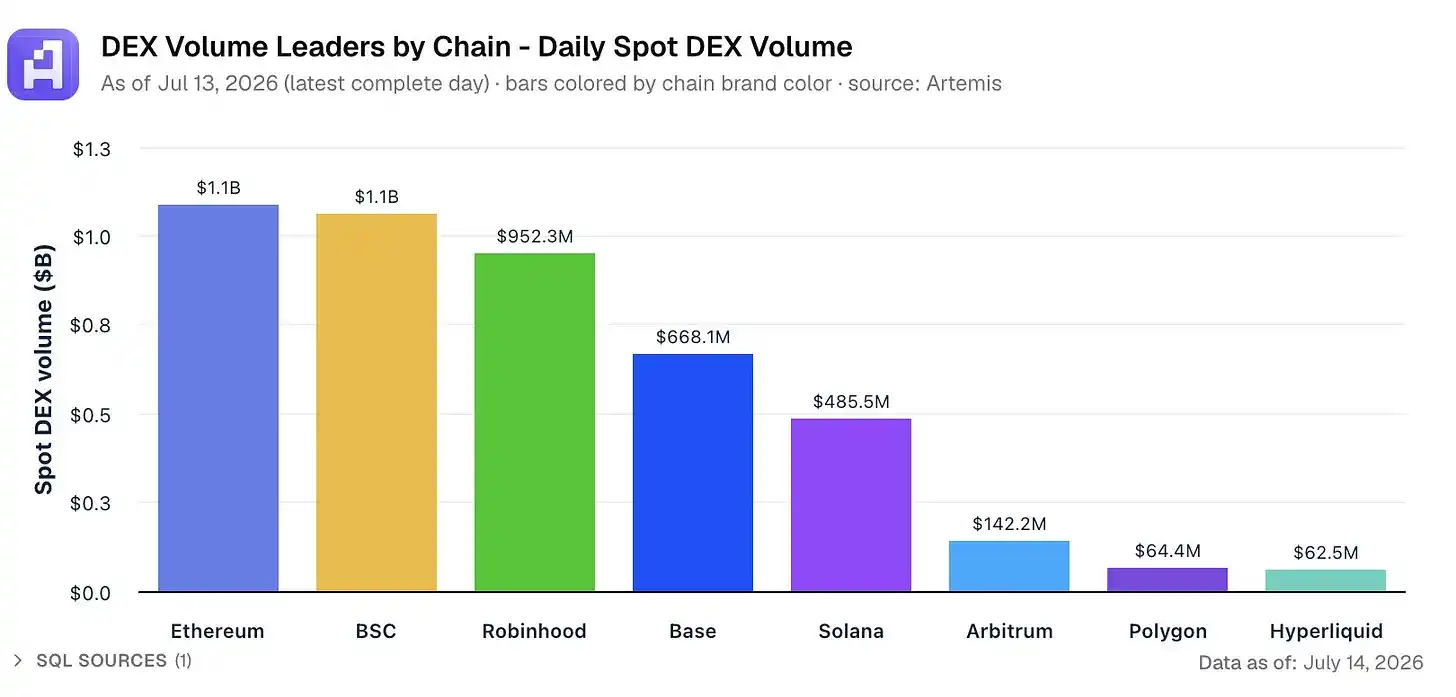

- Spot DEX daily trading volume exceeding $1 billion (ranked #3 on-chain)

- Stablecoin supply exceeding $300 million

- On-chain daily fees annualized at over $40 million

- TVL exceeding $3 billion, contributed by protocols like Morpho, Ethena, and Uniswap

I invested in Robinhood's pre-IPO round back in 2019 while at Whale Rock hedge fund and also covered Coinbase's IPO roadshow in 2020. I founded Artemis to focus people's attention on assets in crypto and stock markets with enduring value, not on trading memecoins.

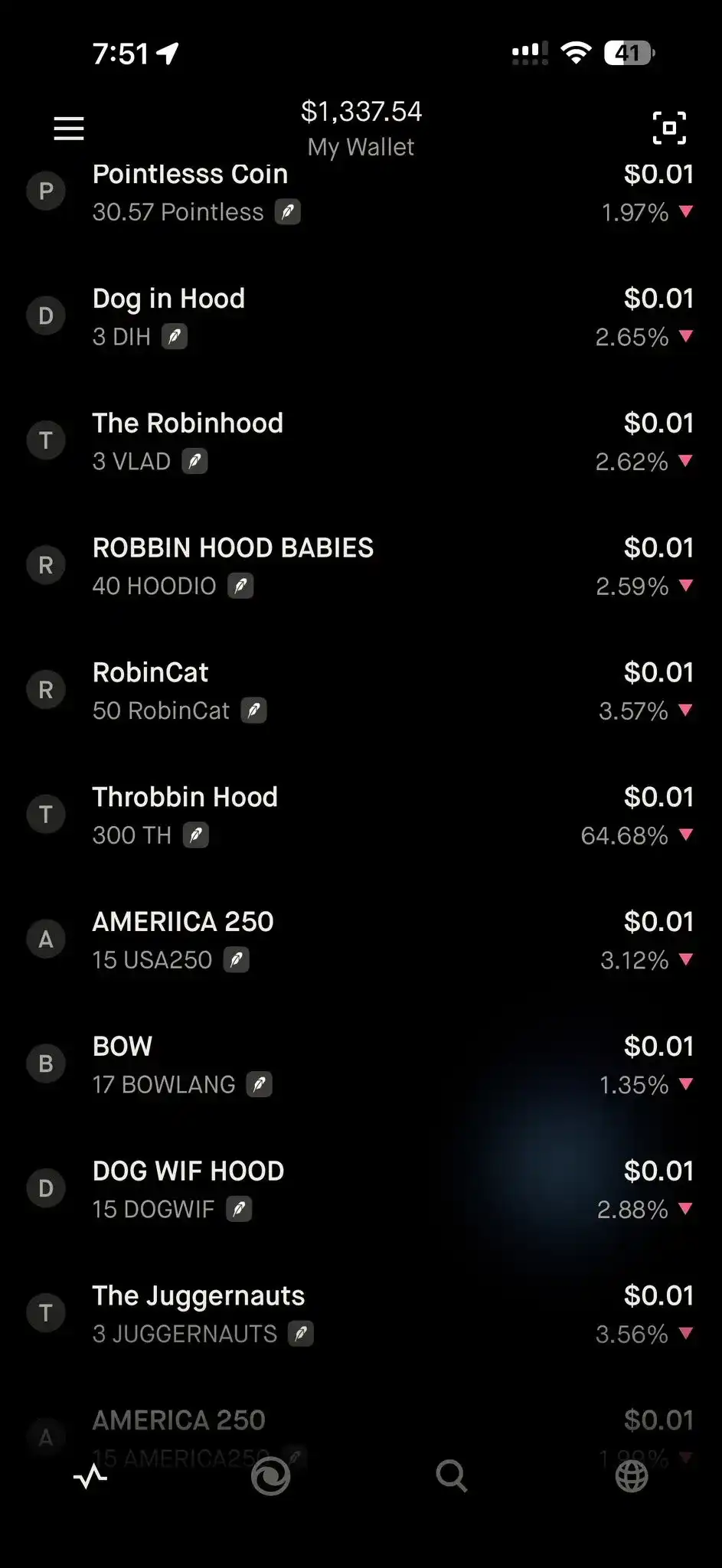

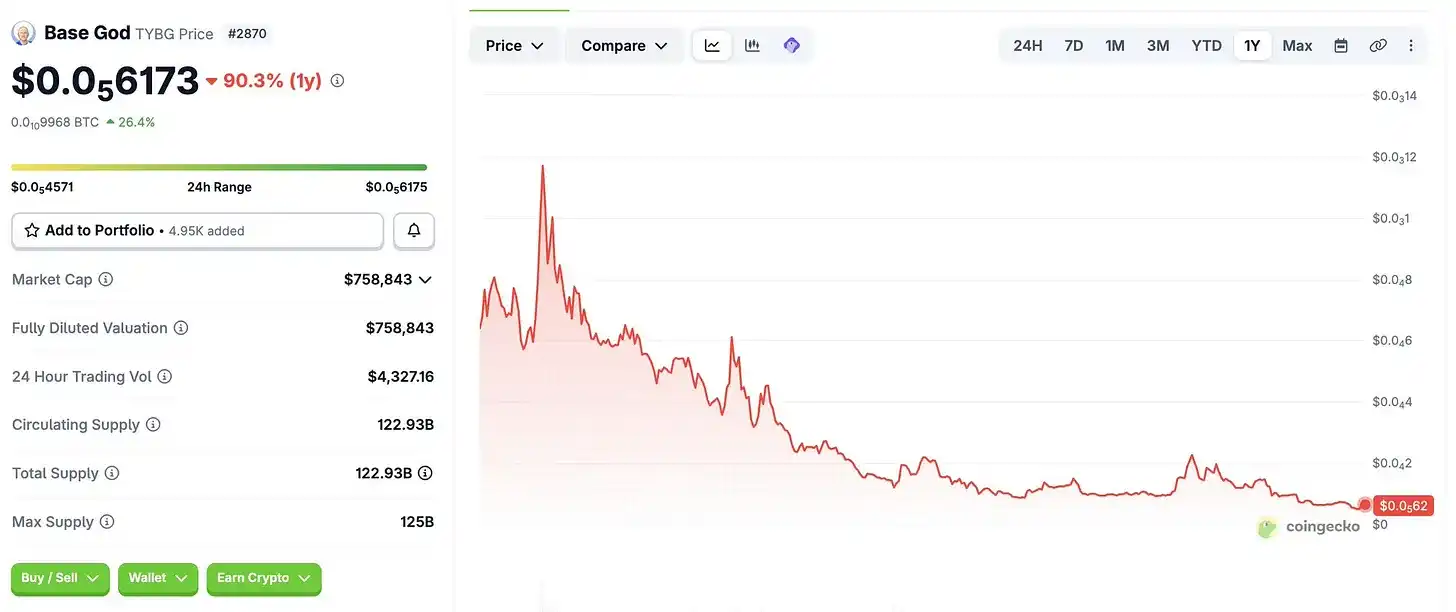

Last week, I was both shocked and saddened when I opened my Robinhood wallet—it essentially only allows trading of Memecoins. After buying some $CASCHAT just three days ago, I was airdropped a bunch of meaningless tokens, one of which was even called "Pointless Coin."

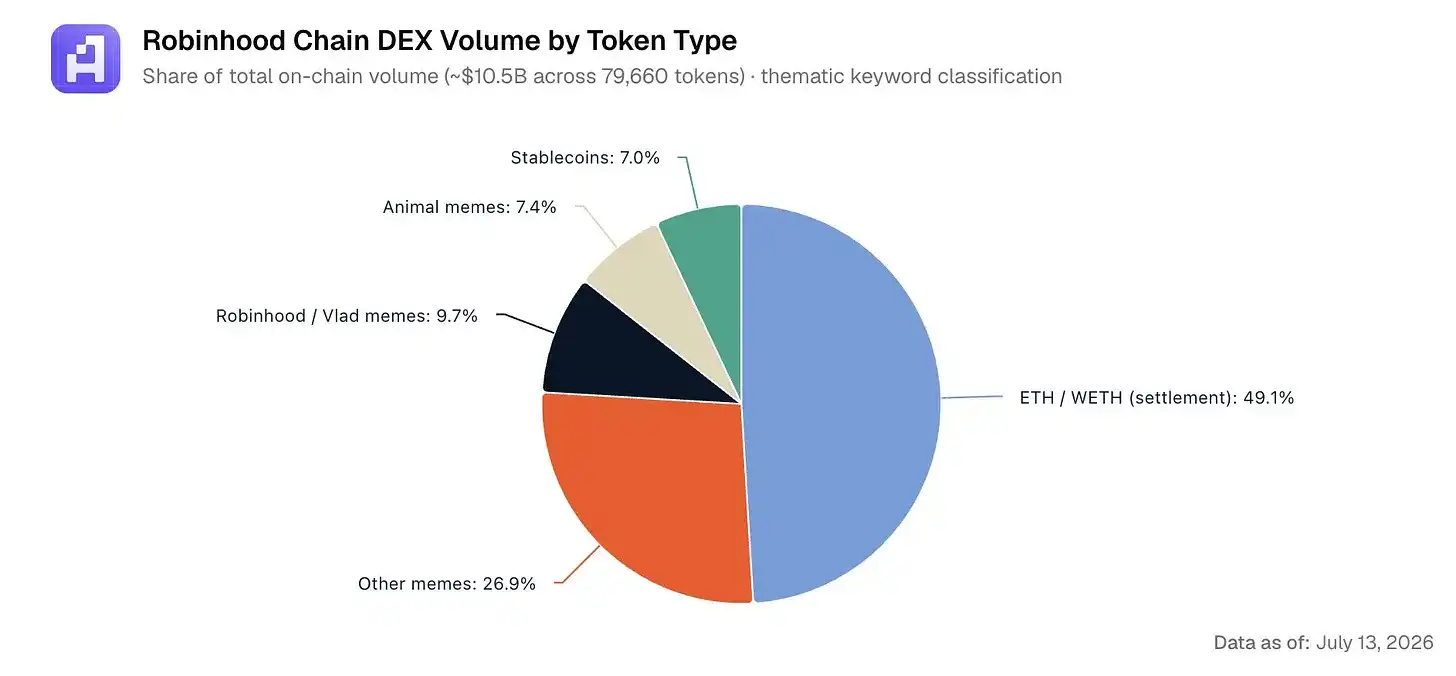

Yes, Robinhood is now the #3 spot DEX by trading volume.

But the bulk of DEX volume is still Memecoins (animal coins, Vlad and Robinhood-themed coins, or other various memes). So please, Robinhood, don't become a memecoin chain.

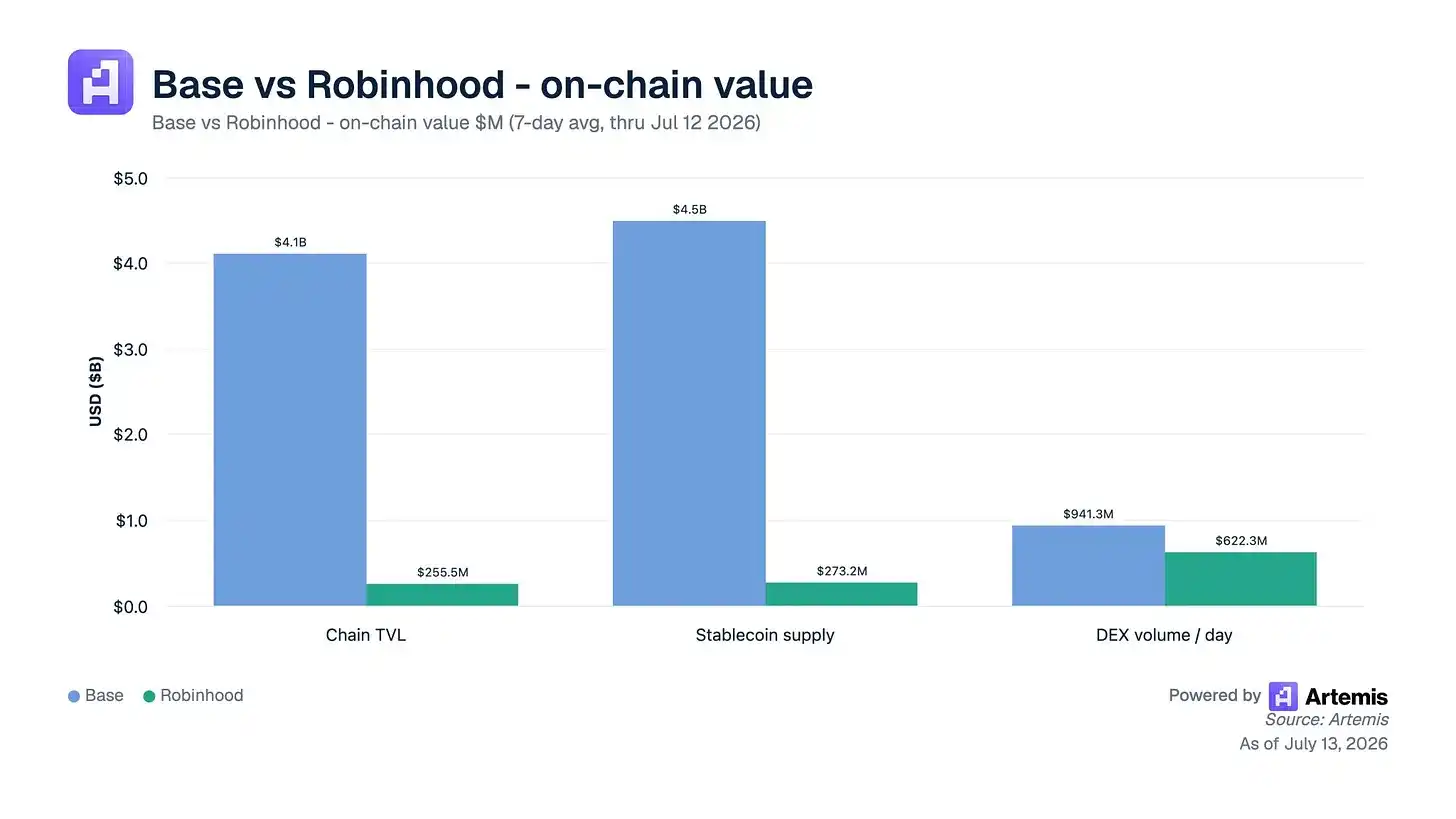

Robinhood Crypto can learn a lot from Coinbase's Base chain—Base is still a much larger chain today.

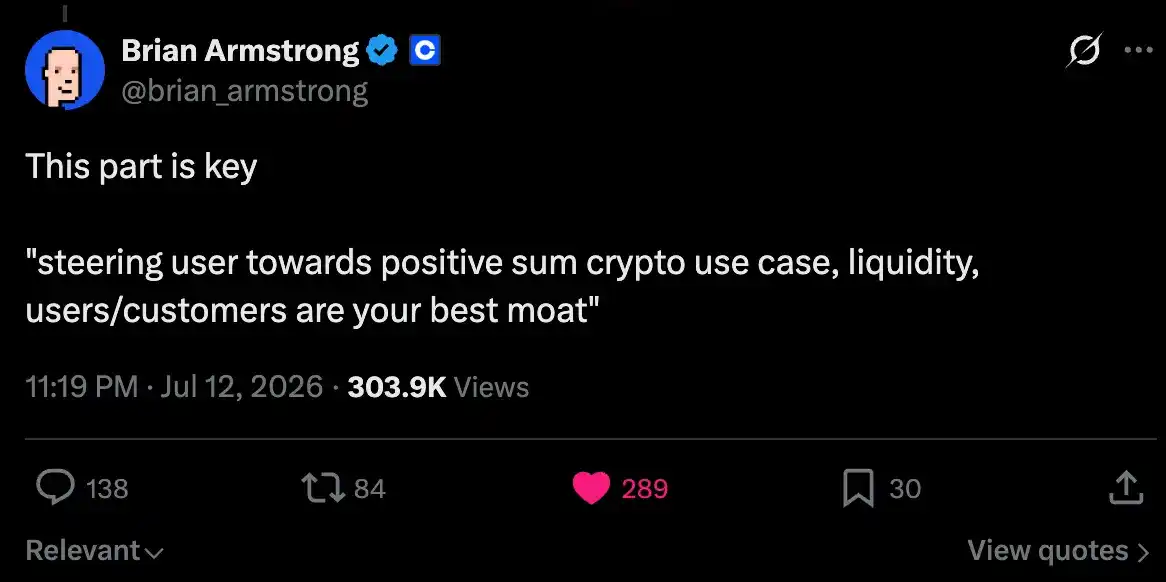

Brian Armstrong even doubled down in his reply, emphasizing the need to guide people towards truly lasting use cases.

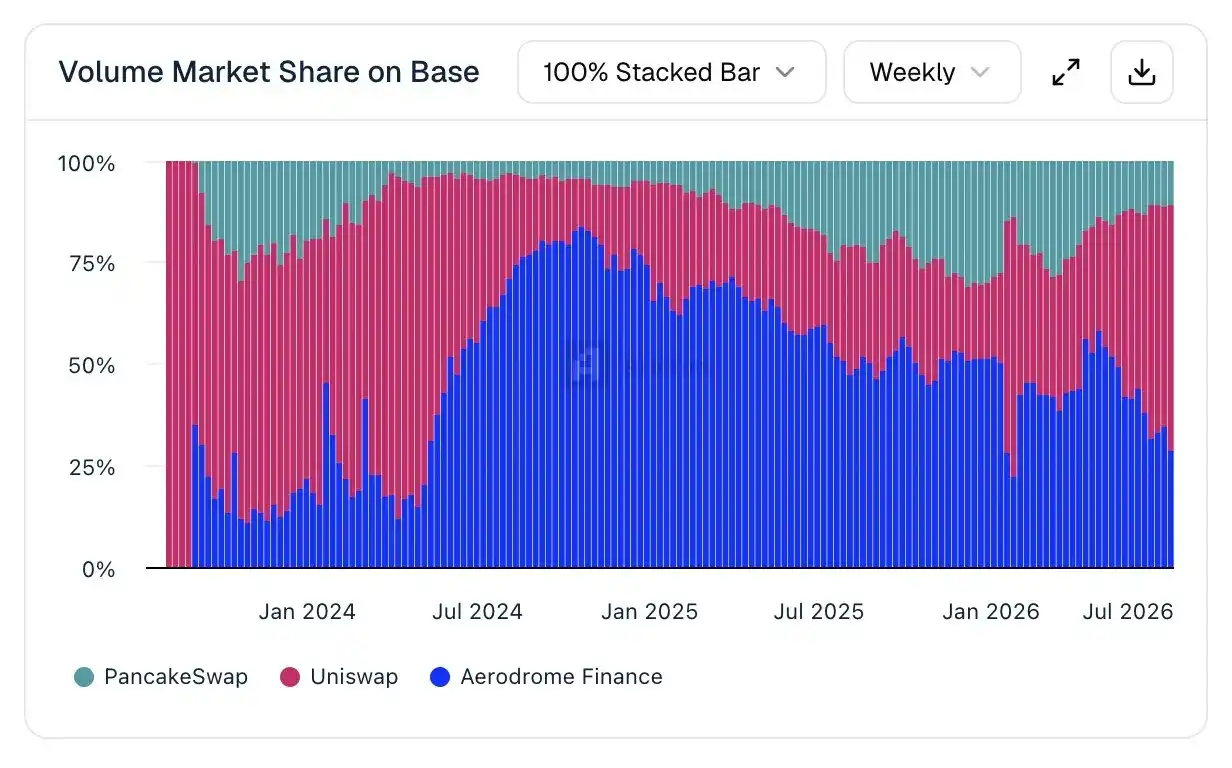

I understand the temptation—Memecoins are indeed a great way to attract early users and draw partners with liquidity and volume (come for the meme, stay for the real apps). Large independent projects like Aerodrome can thrive on Base, dominate volume, and build real business models.

But memecoins cause people to lose money and destroy trust.

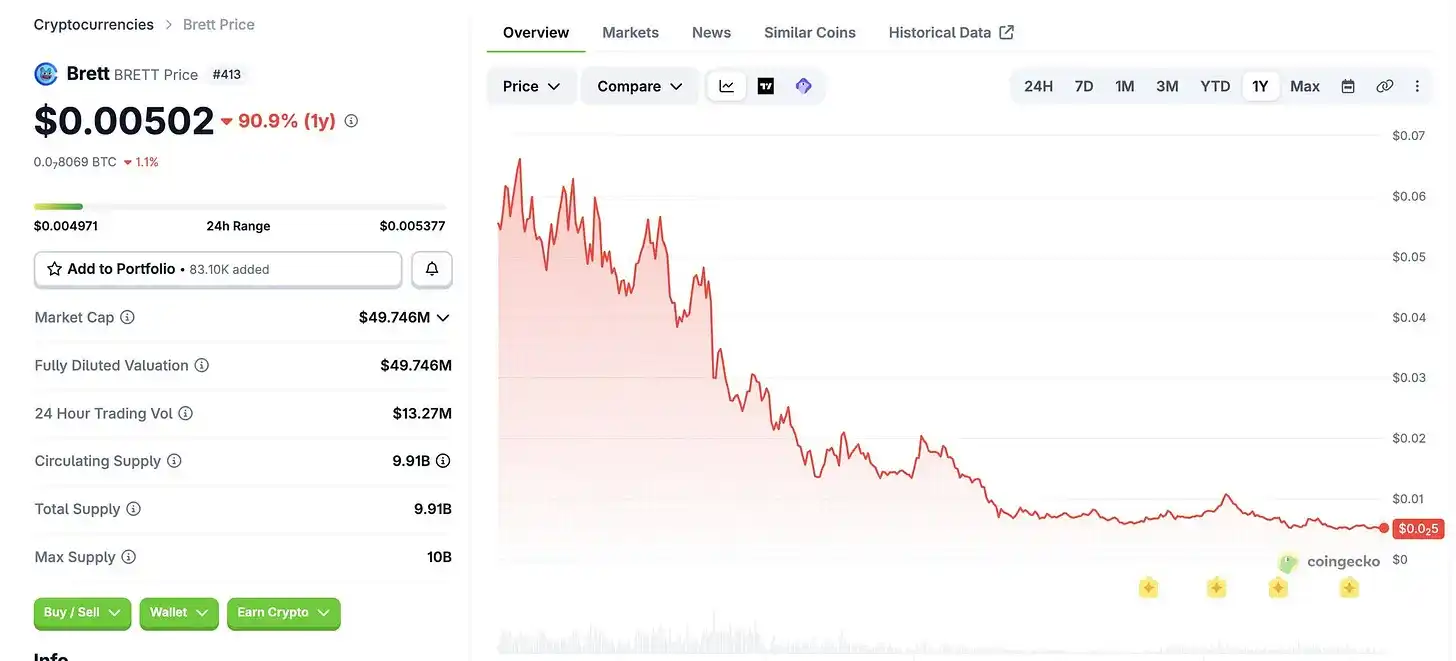

Look at the memecoins launched on Base in early 2024—they're down another 90% this year, 99% from their 2024 peaks.

Memecoins are not durable, they hurt customers, and they push retail further away from blockchain.

Moreover, memecoins on Robinhood Chain would reinforce Wall Street's and hedge funds' stereotypes—that Robinhood is that trading app deeply entangled in the GME/meme stock frenzy of early 2021.

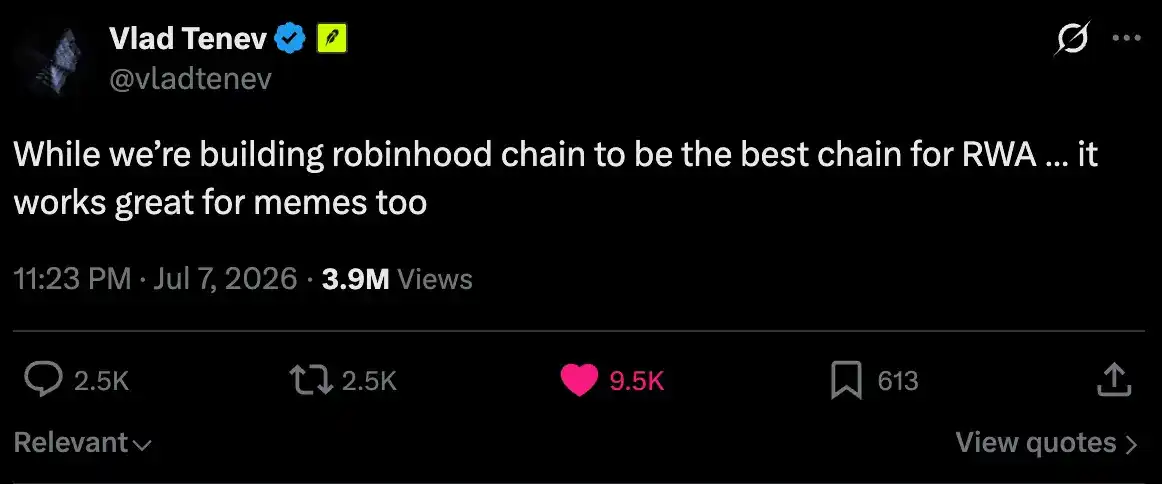

Tweets like this don't help:

Wall Street already struggles to understand Robinhood. Don't double down on the brand damage from 2021.

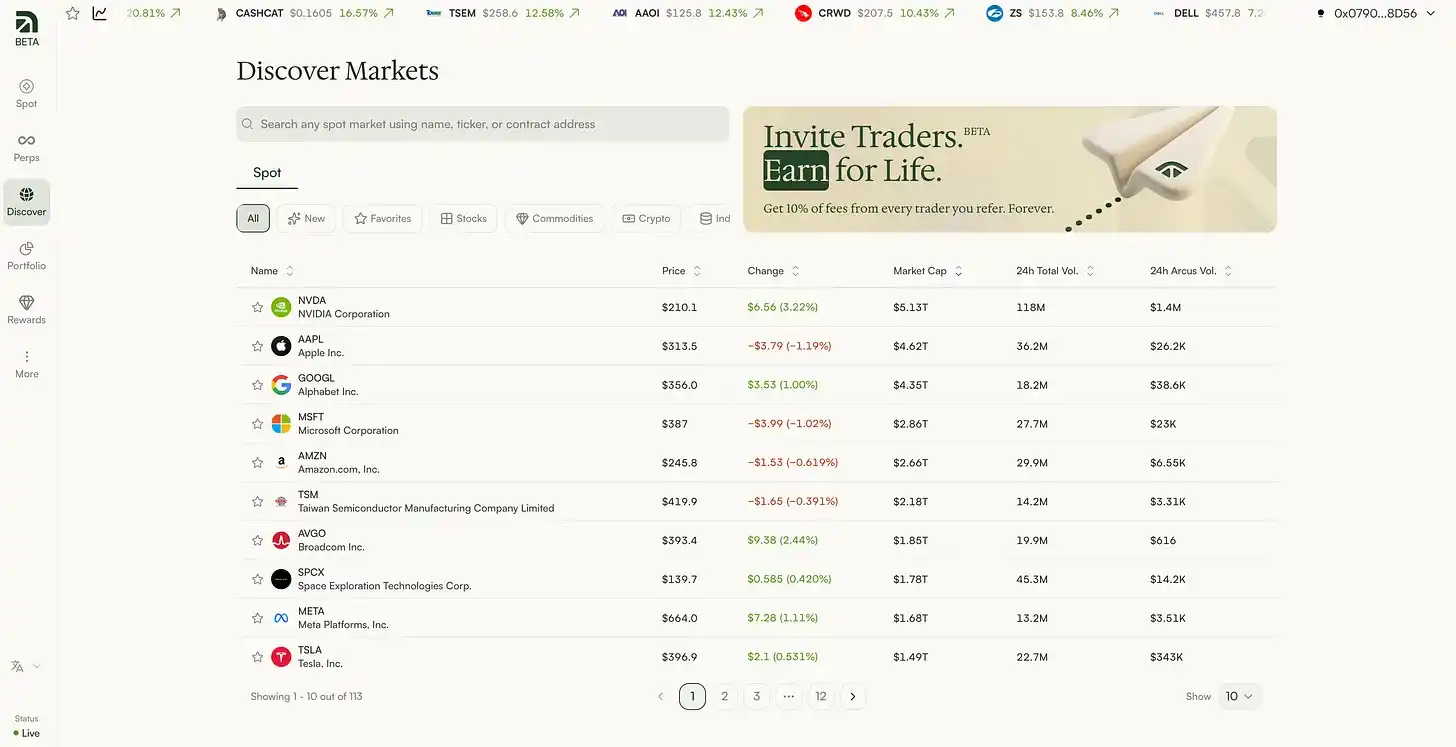

Instead, focus liquidity and attention on the Robinhood wallet and ecosystem, concentrating on Arcus (the former dYdX team, an early leading perpetual DEX) and tokenized stocks. I appreciate that Arcus today allows anyone globally to trade spot tokenized stocks.

These stocks have only gone up over the past decade.

Please genuinely make RWA the focus of the Robinhood chain, enabling more investors to trade stocks and pre-IPO companies and expanding financial access. Teams like RWA.xyz and Artemis are happy to help highlight these use cases.

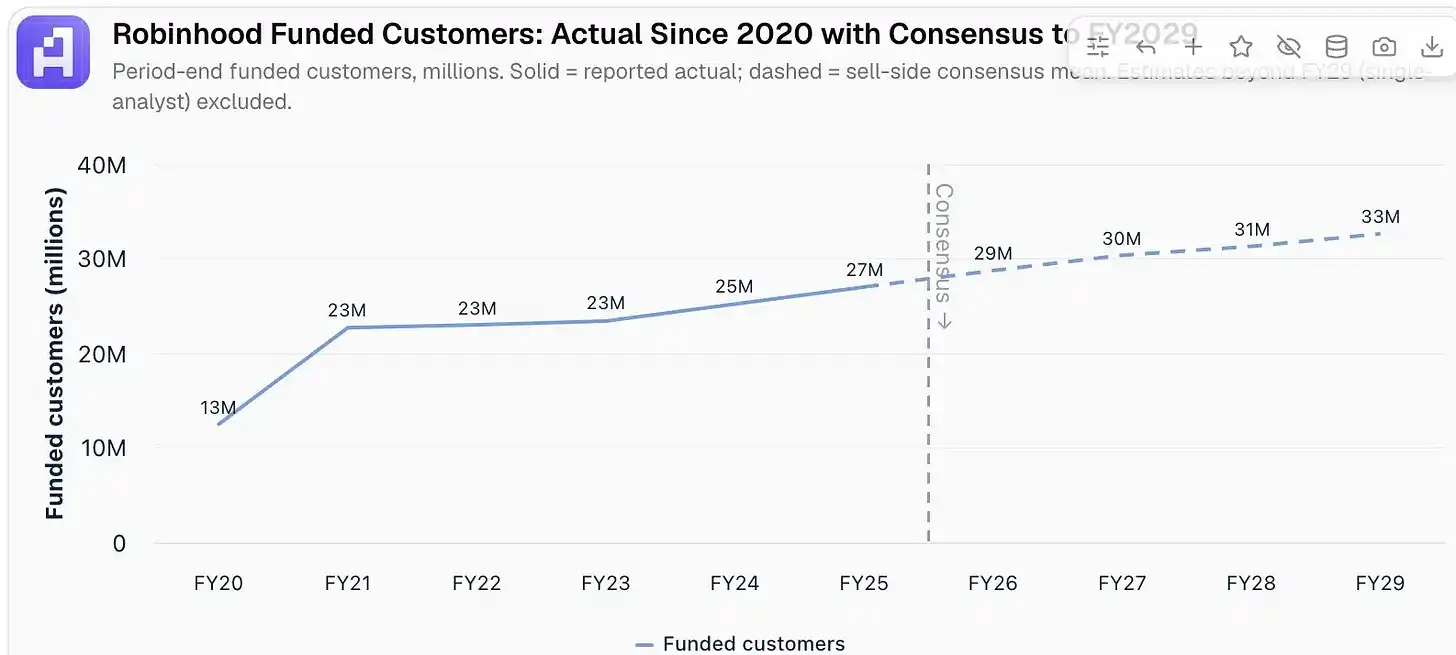

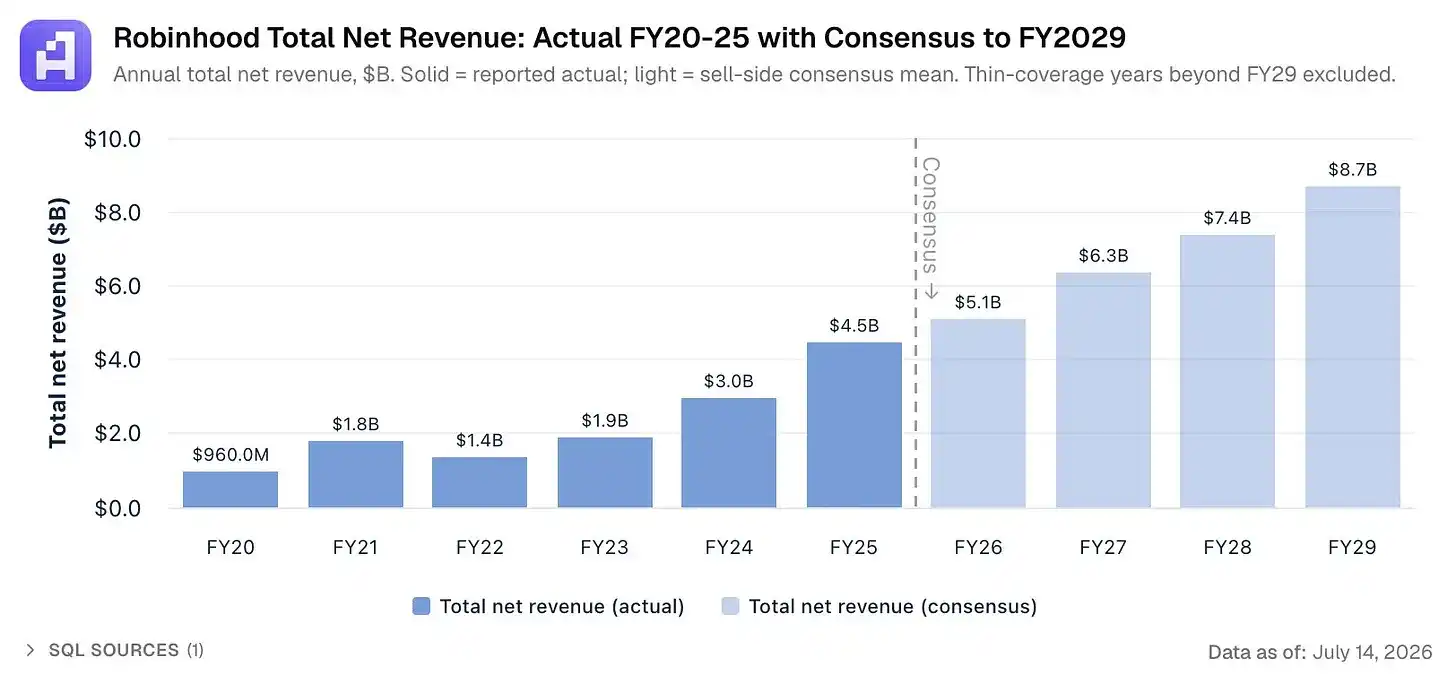

The biggest bear case for Robinhood is that it's saturated the US market—27 million funded accounts, with Wall Street predicting only 31-32 million by FY2028, not explosive enough growth.

My bull case for Robinhood is: Reaching over 100 million international investors via Robinhood Chain, who can now invest in RWAs, prediction markets, stablecoins, public companies, and pre-IPO stocks, serving as an early top-of-funnel for the Robinhood App.

There is real demand for 24/7/365 tokenized stock trading—look at Trade.xyz on Hyperliquid, where people are mainly trading real businesses like SK Hynix with $68 billion in annual revenue.

If Robinhood grows to 100 million monthly active users via Robinhood Chain by 2030, with a current ARPU of $171, assuming a lower ARPU for international users (as they pay on-chain fees instead of trading through the higher-fee Robinhood App), let's say $100 ARPU, then consumer revenue alone could reach $10 billion by 2030, surpassing Wall Street's FY2029 projection of $8.78 billion.

Vlad and Johann, you have the opportunity to realize crypto's promise through asset tokenization—enabling anyone to participate in finance.

Please don't screw it up by turning Robinhood into a memecoin chain.

Wall Street, your customers, and the world will thank you.

A Robinhood User Since 2017