In 2023, early Ethereum investor Wanxiang sold tokens multiple times, at an average price of $2,047. In May 2026, Bankless founder Hoffman fully liquidated his ETH holdings, also at an average price of around $2,000.

Bankless can be considered Ethereum's external propaganda department, single-handedly amplifying the top-tier meme concept of 'ETH is Money.' During the 2021 bull market, fervor for ETH equated to a firm bullish stance on the future of blockchain.

Perhaps due to its importance, or perhaps due to eight consecutive departures from the Ethereum Foundation, Ethereum's founder and spiritual leader, Vitalik Buterin, wrote a long confessional article. He candidly stated that the EF (Ethereum Foundation) controls only 0.16% of the ETH supply and should not hold a position superior to other ecosystem nodes. He also mentioned he would gradually withdraw from operations, returning freedom to Ethereum.

Ethereum Has No Killer

ETH is Money?

Whether you believe it or not, I certainly do.

But how did all this vanish? I'm referring to the market's confidence in $ETH's price, and holders' trust in the Ethereum Foundation and Vitalik. In terms of fundamental activity, now is arguably Ethereum's strongest period of dominance. So why is there so much discontent? Is it just because of the token price?

If $BTC plunges, it's seen as a good buying opportunity. If $SOL drops sharply, its extreme rebound post-FTX has proven its value. If $HYPE falls, one can trade the waves with Arthur Hayes.

Attributing it to Vitalik personally is a convenient reason. However, there's no shortage of abstract public chain founders and foundations. Solana founder Anatoly proactively hard-pitches Perp DEX concepts within the Hyperliquid community. Multiple Ripple founders engaged in wholesale dumping of $XRP. Let alone the proliferation of L2 founders in this era, mostly ego-inflated masters of TGE, seen with the Movement clique.

Upon careful comparison, while Vitalik might be abstract and the EF might be 'inefficient,' it's hard to say they created Ethereum's current predicament. If they are not the problem themselves, then perhaps the broader environment is.

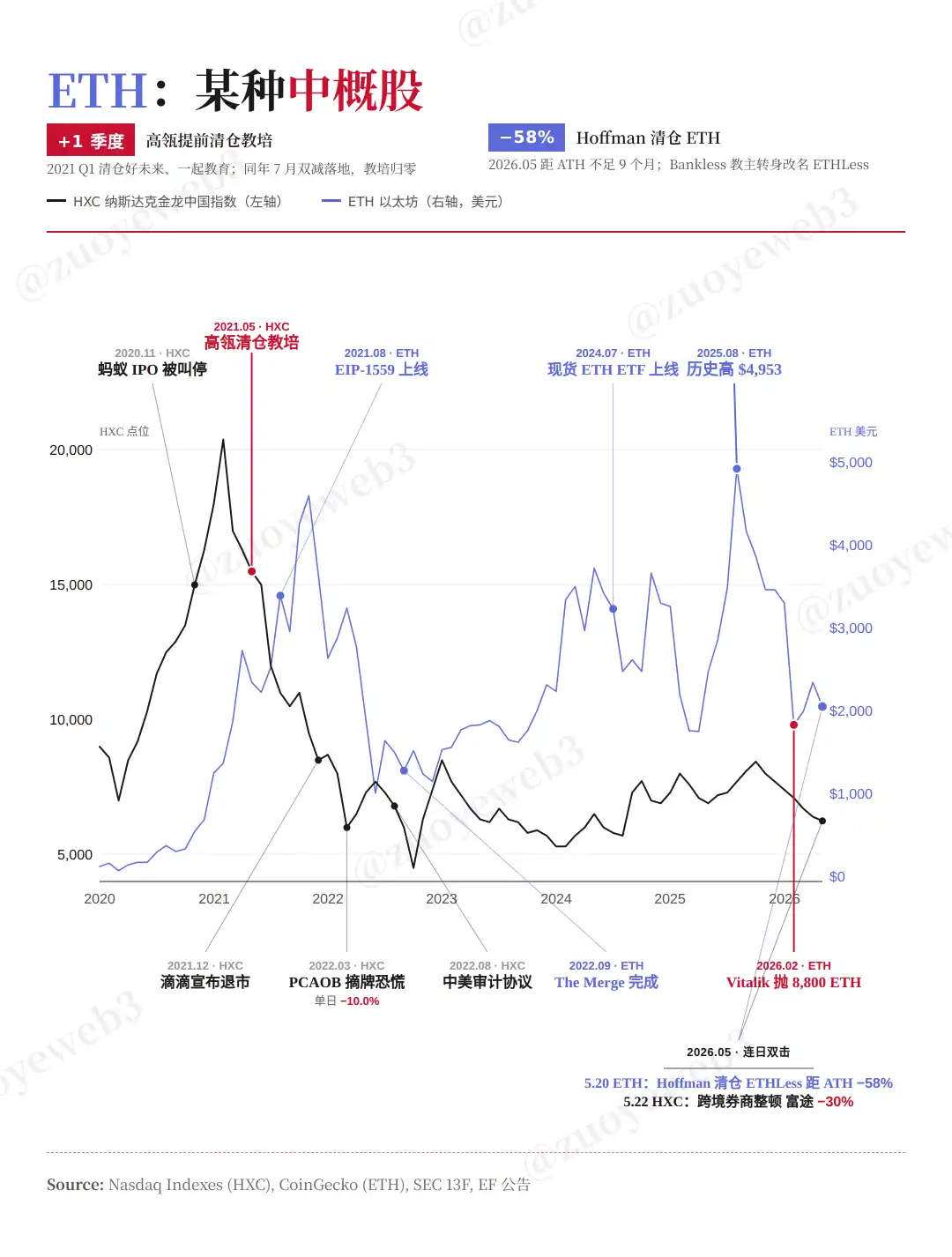

Image Caption: ETH is Money?

Image Source: @zuoyeweb3

The most typical case is Chinese concept stocks. Offshore structures + dollar funds + US IPO created a wealth myth over the past 20 years. Setting aside trial products like Brilliance Auto and China.com, the true first Chinese concept stock was Sina.com in 2000, formally initiating the wave.

The division of labor model of 'US concept + Chinese implementation' we see today is a legacy of this system. Even Ethereum itself is the last remnant of a certain type of Chinese implementation that went global.

In 2014/15, Vitalik first became a guest of Shen Bo and then received a $500,000 investment from Wanxiang, led by Xiao Feng. Unlike Bitcoin's mining model, Ethereum's IXO fundraising, PoW mining, and later PoS staking pulled three waves of passengers onto one vehicle.

In other words, ETH has been a system with relatively strong institutional involvement from the start. I don't mean to say ETH is a heavily manipulated token, and Vitalik indeed wishes for the EF to be just an ordinary node. However, within the Ethereum ecosystem, there absolutely does not exist a state of equal status uniformly distributed among all nodes. It wasn't before, isn't now, and won't be in the future.

Under these circumstances, the public chain founder and foundation actually need to take on more functions. This is unrelated to the token price. Precisely because Ethereum is fragmented with competing powers, someone must stand up and use relatively strong appeal to curb the system's disorderly entropy increase.

But Vitalik chose to first let the EF become bloated, from 'Infinite Garden' to the 'Ladder' theory. Excessive abstraction has left token holders at a loss, especially during the rsETH incident where Aave founder Stani essentially became the 'Duke Huan of Qi,' acting in the name of the king to pacify the lords.

Even the Solana Foundation set aside past grievances to actively endorse DeFi United, only to be met with the EF's routine token sales and Vitalik's personal silence.

Doing too much is centralization. But doing nothing, being overly restrained, is also an abuse of a dominant position—deliberately suppressing oneself, premised on 'the self believing it is important.'

Therefore, Vitalik's choice to make the EF smaller is a mistake. The correct approach would be for Vitalik to recede into the background as a mysterious figure and hand the foundation over to strong institutional players, more pragmatically focused on Ethereum's future.

Apart from Bitcoin, all other public chains need to face the practical demands of ecosystem development and adoption rates. On this point, the Ethereum Foundation holds no special status. The enthusiasm for DeFi and ETH is precisely a memory of past times, not pure wealth effect.

In terms of ecological prosperity and real-world adoption, Ethereum's 'killers' have never succeeded. Solana might be anxious about Hyperliquid, but Ethereum is not, just as BTC isn't anxious about Ethereum.

But this preferential treatment is fading. The crisis does not come from external forces but from within. The real distinction lies in: who is responsible for ETH's price, and who is responsible for Ethereum's direction?

Now, Vitalik is choosing to go all-in on privacy, but he should not 'prevent' others from taking responsibility for the token price.

New Narratives Await the Right Price

Commodity or Productive money?

After the $rsETH incident and the approval of staking ETFs, players like BitMine are rapidly building their own Staking services. Meanwhile, LST players like Lido are increasingly focusing on the 'productive ETH' narrative, with protocols like Spark only recognizing Lido's $wstETH product.

Everything is being reassessed. Lido is not as comfortable as it claims. With ETH prices lingering around $2,000, the marginal effect of continuing to scale diminishes, while the pressure to maintain APR returns increases, casting a shadow over the productivity narrative as well.

This highlights the importance of price—or rather, who is responsible for ETH's price. Currently, the situation is that the EF is not responsible, Lido cannot be responsible, and the entire Ethereum PoS system operates in this awkward environment.

Drawing another parallel to Chinese concept stocks: after US stock markets effectively ceased to be viable exit channels, ChangXin Memory Storage latched onto the AI concept, DeepSeek transformed with state capital taking the lead, and aerospace/robotics concepts oscillate between A-shares and H-shares. Whether you like it or not, this is the new narrative framework.

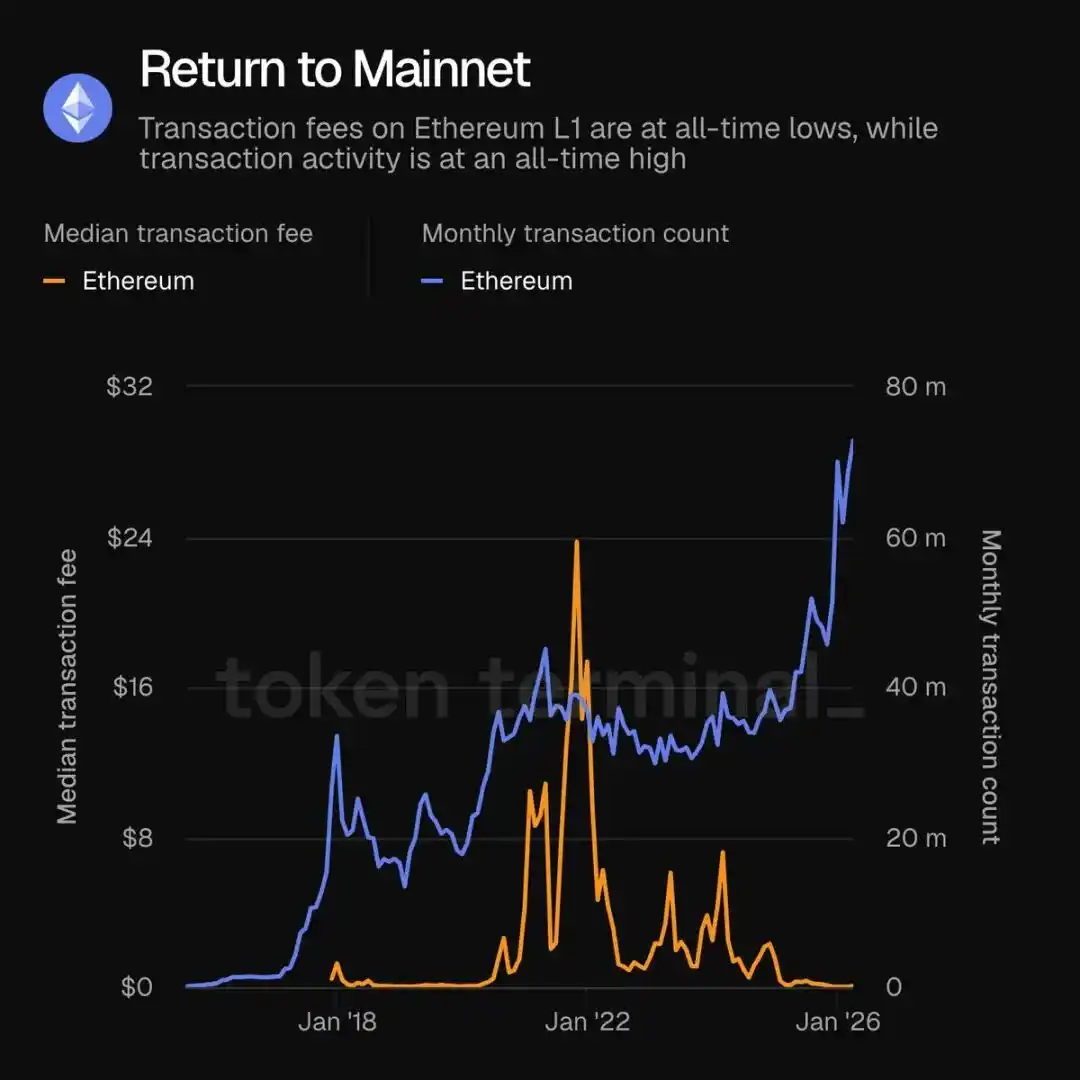

Image Caption: Return to Mainnet.

Image Source: @tokenterminal

With Ethereum's shift back to focusing on L1, mainnet activity exploded. Yet, you don't feel the Ethereum ecosystem is genuinely improving, let alone the token price rising. Something is clearly wrong, but people can't define the problem.

So, what about the current Ethereum technical narratives?

- Privacy: Everything can be ZK, the last bastion of decentralization ideals.

- AI: Teams like dAI are migrating centralized architectures on-chain, focusing on small model on-device deployment and Agent invocation.

- L1: Complete abandonment of the L2-centric model, with all competition over speed and revenue returning to L1.

Compared to the 'world computer' and smart contract technical synergy, Ethereum now needs to forge more connections with reality. Beyond the three above, there are stablecoins, RWA, and many other narratives. But these are not how Ethereum views the world; rather, it's Ethereum's place *within* the world.

The subject and object are inverted, or rather, its position in the new world is unclear. The grand ambition of 'everything can go on-chain' and 'blockchain fights for the future' is gone. Yet, there's always a feeling blockchain can do more. This contradiction, entanglement, and repetition form the threefold chorus of current market sentiment. People hope to see a better Ethereum, but seeing a good Ethereum seems unlikely.

After over a decade of striving, Ethereum did not become the world computer, but it is truly an open computer. Any activity or idea can be experimented with and run on it. While Bankless promoted 'ETH is Money,' Vitalik insisted 'ETH is a Commodity,' a digital product carrying specific functions.

On this point, no one can accuse Vitalik of lying. When Vitalik sold 8,800 tokens in February 2026, he did so slowly via CowSwap. He didn't follow Curve's founder by staking $CRV for stablecoins, nor did he emulate Justin Sun's tactics with $USDD to fleece retail investors.

But as in the Chiang Mai dialogue in January 2026, when asked if given a chance to turn back time ten years, would one choose blockchain or AI, Vitalik didn't give a firm answer. Yet, the reality is set: more and more crypto project teams are pivoting to AI, skillfully applying Go-To-Market methodologies.

- Hermes Agent broke into the mainstream AI developer circle, with the founding team from Nous Research.

- xBubble is developed by DappOS, combining AI + intent execution frameworks.

- OpenRouter founder Alex Atallah is from OpenSea.

You'll find crypto project teams' marketing capabilities aren't limited to on-chain activities. Even in the globally watched AI trend, they can repeatedly keep pace. Even the transit hub model intertwines with stablecoins, traffic distribution, and operations.

But all this has a weak connection to Ethereum. Although dAI and virtuals jointly proposed ERC-8183, attempting to define an autonomous Agent economic activity framework, it's not that the team isn't working. It feels more like active adaptation rather than a leading posture.

If we consider the present a moment for narrative bottom-fishing, the core question is: what value does a public chain hold in the AI era?

Claude repeatedly attacks SaaS, security, and external Agent frameworks. Imagine an absurd scenario: if Claude created its own chain, what would happen to Ethereum?

Under the PoS mechanism, asset migration costs are low enough. But in terms of compliance costs, Claude would still be bound by human legal constraints. An unrestricted free financial testing ground might be Ethereum's most unique value proposition.

Just as when Mythos hammered Palantir's stock, QiAnXin would surge against the trend because hitting the opponent triggers an arms race among counterparts across the ocean, creating an infinite loop.

In other words, in a world of increasing polarization, the demand for connecting the globe will persist long-term. Canton belongs to Wall Street, but Ethereum belongs to all humanity. Just as people in the Sahara have no shoes, pessimists exit, and optimists rejoice.

However, the golden age of $ETH will not return. Wanxiang, the EF, and other institutions will continue to sell. But ETH at $2,000 is at least ten times $200. We stand at a new starting point; we just need a course to sail.

Conclusion

Destined to be alike, ETH truly shares a fate similar to Chinese concept stocks. Both are assets from Country A, invested in by Country B's capital, and exited on Country B's secondary markets. Country A only bears market and channel value.

This is the best of times. Under such fragmentation, new markets will be born. Following Country B's dynamics, similar assets in Country A will experience analogous cycles. Amidst the fragmentation, both A and B still need new connection points. Ethereum remains the best choice.