Author: Billy Gao

Translation: Jiahuan, ChainCatcher

The most powerful cryptographic system ever built can’t even keep a single secret.

Perhaps the biggest irony in the crypto industry is this: we’ve built the most powerful cryptographic system in history, packed with more math than almost anything else, yet the one thing it doesn’t do by default is protect the privacy of your funds. Every position you hold, every payment you make, every dollar you move is broadcast to the world by default.

We seem to have defaulted to and accepted this as normal.

And yet, this is the single biggest reason trillions of dollars that should be on-chain aren’t yet. So let’s get back to basics: how did we get here, what’s still broken, and the one solution that is finally landing now.

Blockchain is a slow, expensive computer that nobody owns

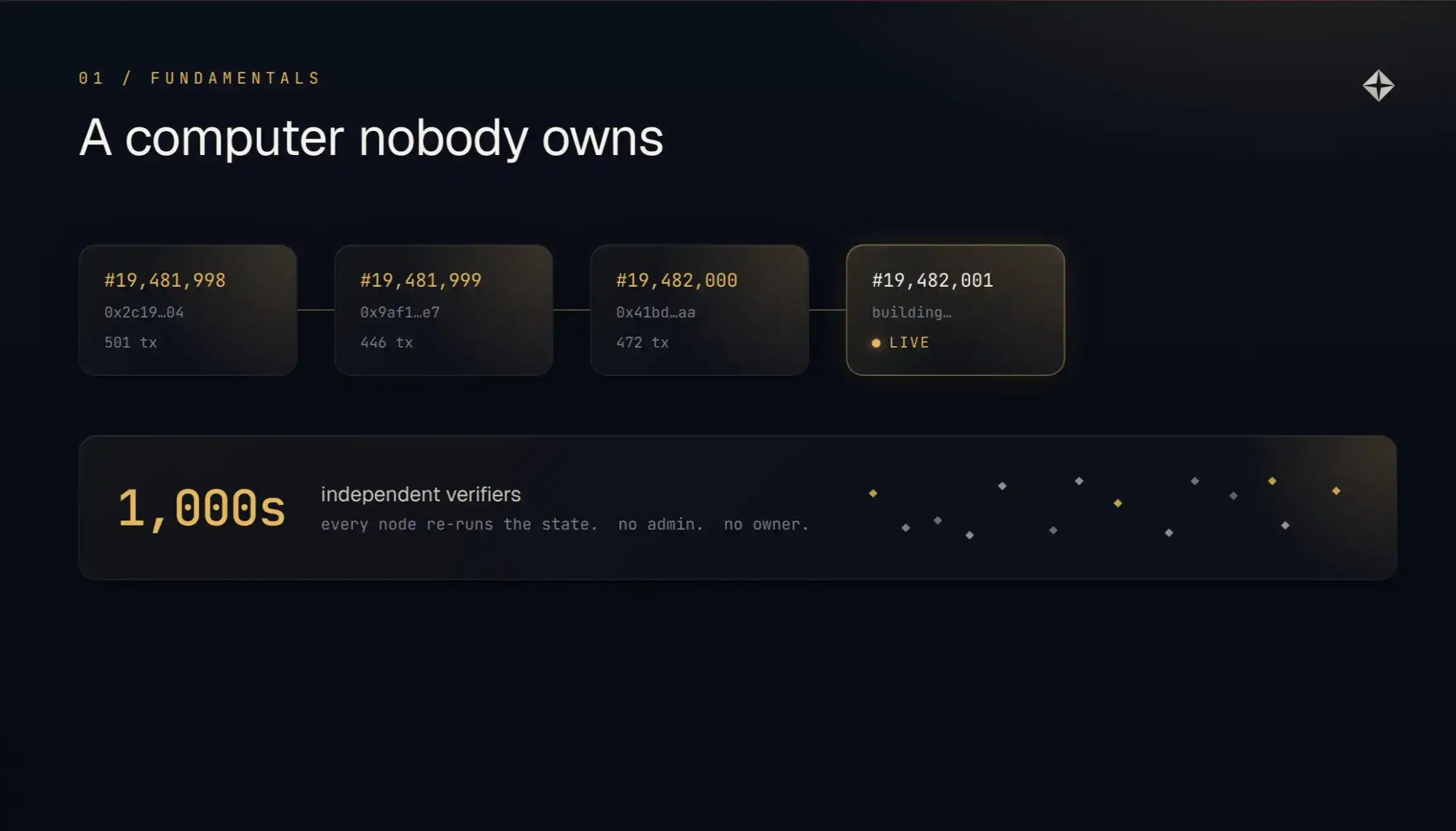

Strip away fifteen years of narrative, and a blockchain is just a shared computer, slower than the laptop you’re using to read this. That’s all it is.

Back to the first principles of 2012, the ones that sound too simple to mention anymore. A blockchain is a list of blocks, linked by hashes. Each block contains a payload: transactions, state changes, and so on.

Each block points cryptographically to the previous one, so nobody can change history without everyone noticing. Anyone can run the verification program to check if the whole system is valid. The consensus mechanism keeps changing — from proof-of-work to proof-of-stake to whatever’s next — but its core premise hasn’t moved an inch.

It’s slower, more expensive, and clunkier than your laptop. Its only trick, the whole reason it exists, is that nobody can stop you from using it, and nobody can cheat you on the outcome. There’s no administrator, no privileged party you have to ask.

But that trick is expensive. Every node reruns your computation and stores your data permanently. So the only rational thing to put on this machine is the tiny set of things that truly need this property and are worth the cost.

Most things don’t, which is fine. For the rest of this discussion, keep this test in mind: does this thing actually need a computer that nobody owns? Because it determines almost everything that follows.

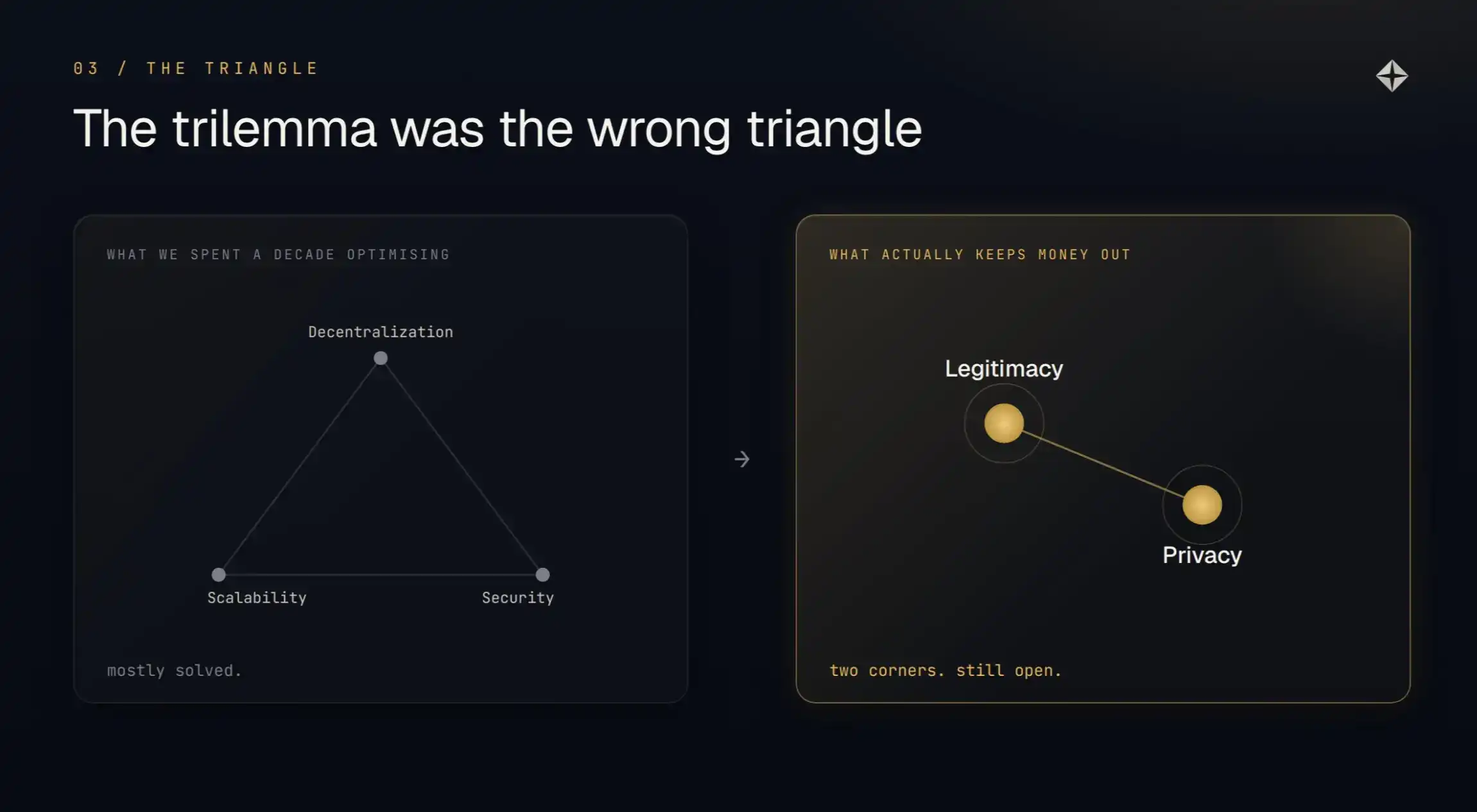

The “trilemma” is a badly drawn triangle

The whole industry spent a decade fighting over decentralization, scalability, and security. It mostly won that fight, only to find that the real constraint wasn’t in that triangle at all.

For years, all the talk was about the “trilemma”: decentralization, scalability, security — you can only have two out of three, never all three. The Ethereum era was one long argument about it. Block size, sharding, rollups, layer 2s — these topics swallowed the field for years.

Then, almost silently, we mostly solved it. Block space is cheap now, throughput is high, rollups work. The scaling problem that defined a decade is, for practical purposes, over.

Then the real core problem surfaced. Once scale stopped being the bottleneck, an uncomfortable truth became clear: the actual constraint keeping capital off this machine wasn’t in that triangle at all. We spent ten years optimizing the wrong three corners.

To find the right corners, stop asking “how does the machine perform?” and ask a more direct, honest question: who is this actually for, and who still can’t use it today?

Why only money actually works

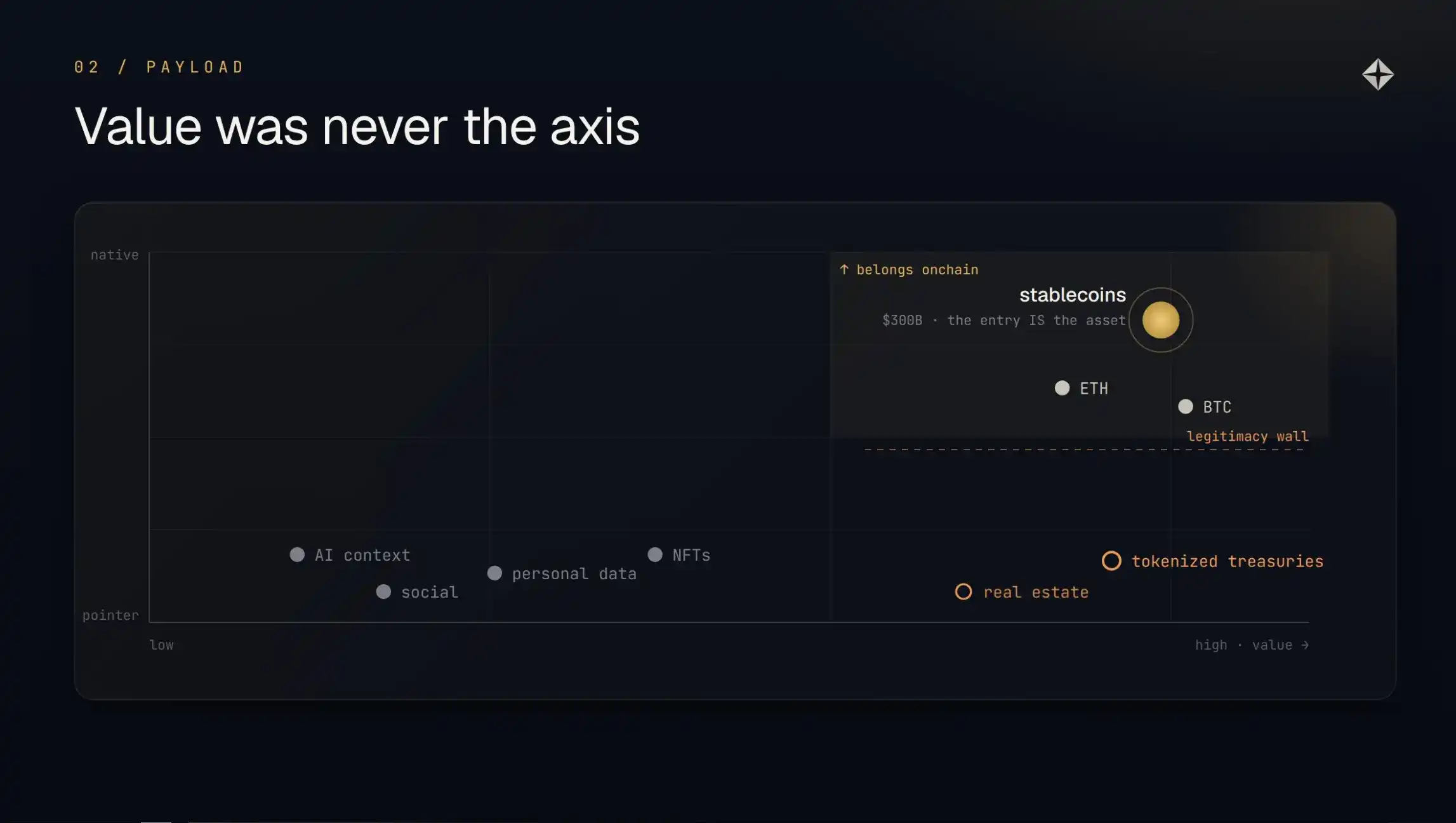

Money is the only thing where the ledger entry itself is the asset. Anything else you put on-chain is just a pointer to something else.

Follow the property downstream, and what a blockchain is actually good for almost floats out by itself.

First, access. Anyone, anywhere, can log into this shared computer and change its state. No business hours, no need to ask a privileged party (a bank, a broker, an exchange) to update the ledger for you. For money, this is enormous value. Moving value becomes as direct as editing a file.

Second, trust. Why did we give our money to those privileged parties in the first place? Because we trusted it would be safe there. Blockchain answers the same question with a different mechanism: trust not a party, but numbers — numbers in both senses, math and quantity. With enough honest participants economically aligned, and the math to verify the whole system. Now your money is as safe as the network itself, not as safe as a party.

But there’s a third, almost never mentioned. Money is the only thing where the ledger entry itself is the asset. A dollar on-chain is just a number, and that number is the dollar. That’s it.

This is why finance stuck here and almost everything else failed. This pure ledger-native asset is exactly the kind of thing the ledger was built for. The market has proven it: stablecoins are now a $300 billion industry, settling ~$33 trillion per year, and that growth is no longer driven by retail speculation.

What should go on-chain, and what shouldn’t

Crypto found its killer app, then only served a very narrow slice of the market. Too risky for the top, pointless for the bottom. It serves the “comfortably off,” and almost nobody else.

Since money is the natural payload, the next question is: what money-adjacent things actually clear the “needs a computer nobody owns” bar. The failures at both ends bracket the answer.

The bottom is the cheap stuff. You can argue everything has value, and therefore is “financial.” But you’re always weighing two things: what something is worth, and the cost of running it on the most expensive computer ever built.

Social media, personal data, AI context tokens. These things Web2 already does incredibly well, and basically for free. Putting them on-chain adds only cost, removes nothing. The unit value is too low to justify the machine. Most of what people tried to force on-chain last cycle died on this test, and the next cycle will be the same.

The top is the capital that can’t come on-chain. This is the real tragedy. Look honestly at who actively uses crypto today, and the demographic is shockingly narrow. Let’s call them the “comfortably off.” Enough money not to worry about survival daily, but not so much that you’re managing institutional-scale capital. Beyond a few crypto-native funds, that’s basically it.

The capital that should be here (family offices, sovereign funds, large institutions, corporate treasuries) looks at this machine and walks away. Not because they don’t get it, but because the way it works doesn’t make sense to them.

Their objection list is long, and honestly most of it holds: legal and regulatory uncertainty, custody risk, constant hacks, smart contract risk, MEV, inability to self-custody safely at scale, counterparty risk at every step. Stack it all up against the marginal yield, and the math often says it’s not worth it.

To many, crypto looks like a high-volatility, zero-sum arena where everyone is fighting over the same pool of dollars. Honestly, they’re often right.

So crypto is stuck in a narrow band: too weird for capital above, too pointless for applications below.

But look at that objection list again. Most are operational problems, and operational problems are solved by brute force: audits, insurance, regulated custodians, time. Strip those away, and two points remain that can’t be patched. Because they aren’t implementation flaws, they’re design properties.

Public chains are permissionless, which puts them in a legal gray zone. And public chains are transparent, which leaves you exposed.

Legitimacy and privacy. That’s the real triangle the old one missed, and it only has two corners. Whether you can cross these two corners is the whole game, and it comes down to these two flaws.

Flaw one: Legitimacy

For a decade, the most honest answer to “is this thing even legal?” has been “kinda.” For anyone managing real money, that’s a non-starter. And now, for the first time, that answer is starting to change.

The first flaw flows directly from the feature that makes it valuable. Anyone can do anything. That’s what makes the machine valuable, and that’s what makes it a regulatory minefield.

Permissionless is a double-edged sword: the same property that lets you move funds without asking anyone also lets others do things that get the whole industry labeled a fraud haven. For a serious allocator, that’s a deal-breaker regardless of the underlying tech.

This flaw isn’t fixed with better cryptography; it’s fixed with policy. In July 2025, the GENIUS Act became law, providing the first true federal framework for stablecoins as the core financial payload. Market structure legislation followed closely. It’s not law yet, but the direction is unambiguous, and the environment for builders and allocators is far friendlier than two years ago.

The old three-headed puzzle of governance, decentralization, and legal risk has receded to the point where running a compliant on-chain business is now just a regular business decision.

So that corner is closing, more or less on its own. And the other flaw is where the whole industry got it backwards for a decade.

Flaw two: Transparency is a tax

On-chain transparency isn’t a feature; it’s a tax. Every position you hold is public, and the network charges you for being seen, via MEV, via front-running.

This is the part everyone has gotten used to but absolutely shouldn’t. On public chains, your entire financial life is being broadcast. Every position, every trade, every transfer, visible in real time to anyone with a block explorer. “It’s transparency, it’s a feature,” we’ve heard it so long we’ve stopped noticing it’s actually a leak.

And it’s a quantifiable, ongoing tax. The second your order hits the public mempool, anyone can see it and trade against it, front-run it, sandwich it, or watch to liquidate you.

This isn’t hypothetical. By mid-2025, over ~$1.8 billion in cumulative MEV had been extracted on Ethereum alone. That value was siphoned directly from regular users’ trades, simply because those trades were visible before they settled.

Look at who’s already paying to avoid it. Sophisticated trading desks and funds long ago stopped broadcasting to the public mempool. They use private relays and order flow auctions, specifically to hide their moves until they’re done.

Smart money is buying privacy piece by piece because smart money knows transparency costs them money. Everyone else defaults to paying the tax.

For the average retail user, it’s worse: every time a normal trader on some venue opens a position the whole world can see, their edge is being bled away.

Transparency was sold as a “level playing field.” In practice, it’s the opposite.

Now pull the lens back to the capital we actually want. No family office, sovereign fund, or large institution is going to put its balance sheet on a machine its competitors can read in real time.

Of course they won’t. Broadcasting your treasury operations to the world in real time makes no sense. They need a private space of their own inside this shared computer.

Honestly, everyone does. You wouldn’t accept your bank statement being posted online; there’s no reason to accept it here.

This is why payments and serious trading haven’t fully moved on-chain, and why equating privacy with “anonymous trading” is slightly ridiculous.

The biggest irony in cryptography

Encrypted communication has been mainstream for thirty years. Encrypted money still isn’t. On a system built entirely from cryptography, that should be slightly embarrassing.

Step back and the absurdity is hard to miss. Blockchains are built from cryptographic primitives. Hashes, signatures, commitments — it’s cryptography all the way down.

And the one thing it doesn’t do is encrypt the user’s actual activity. We built an entire cathedral of cryptography and left the front door — your financial privacy — wide open.

We solved this problem for communication decades ago. Nobody thinks encrypted communication is weird or suspicious; it’s the default, and the world works fine.

The foundational pieces to do the same for money have been there all along; the cryptographic primitives have been quietly improving for ten years.

What’s been missing is performance: how to make it fast enough, cheap enough, for production. That’s a math problem and a hardware problem. The hardware has caught up. Dedicated acceleration hardware has pushed the cost of these proofs down to where they can run at real throughput.

The question was never “is this possible?” It was “is it worth the cost?” And now, for the first time, the answer is “yes.”

A response to the strongest objection

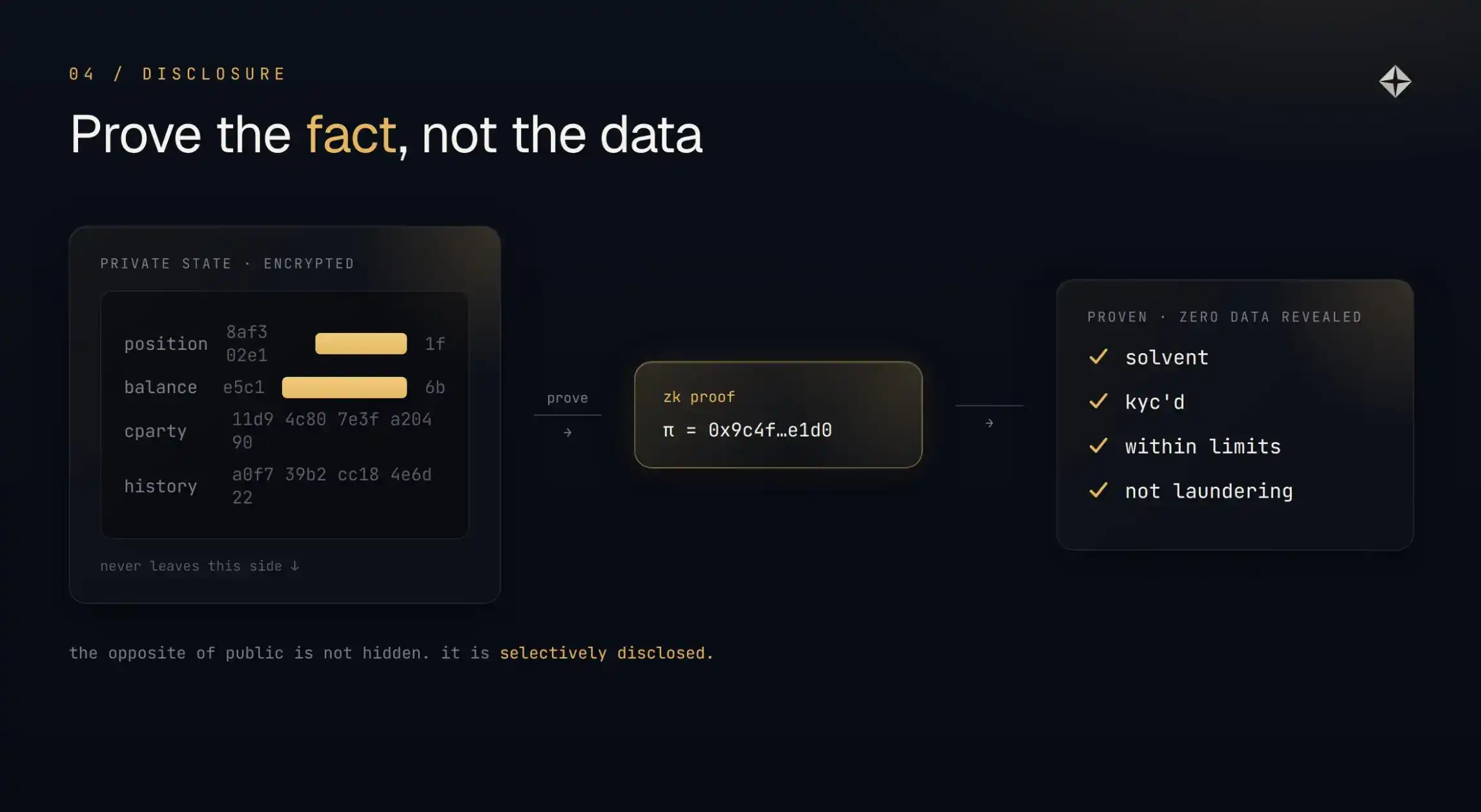

“But isn’t transparency the whole point? Proof of reserves, no hidden leverage, verifiable solvency.” That holds if privacy means hiding everything. But it doesn’t have to.

The strongest argument against on-chain privacy deserves a real answer. Transparency is load-bearing. It’s how you verify a stablecoin is actually backed, how you confirm a protocol is solvent, how you spot hidden leverage before it blows up.

It’s also how law enforcement tracks stolen funds, and regulators fight money laundering. Make everything opaque and you lose half the value of auditability and hand criminals a convenient tool.

It’s a serious objection, but it quietly assumes a false choice: as if you only have “fully public” or “fully hidden.”

Privacy and compliance have never been enemies

You can prove solvency, KYC, staying within limits, without revealing a single position. Prove the fact, not spread the data.

Here’s the real argument, laid bare: the opposite of public is not hidden. Modern cryptography lets you prove a statement is true without revealing the underlying data that makes it true.

You can prove reserves exceed liabilities without publishing the reserves. Prove an address is KYC’d without exposing who it is. Prove a position is within risk limits without revealing the position. Prove a transaction is clean, not money laundering, without broadcasting the sender’s entire history.

This dissolves the objection directly. The auditor still gets his assurance. The regulator still gets its compliance check. Law enforcement still has a legitimate disclosure path. What disappears is broadcasting everyone’s financial life, and every predator in it, to the world in real time. You keep every benefit transparency was supposed to provide, and delete the tax.

Privacy and compliance have never been opposites. They only looked that way because the privacy tools we had were blunt — like mixers that hid from everyone, including the police.

Compliant privacy with provable disclosure is the synthesis this whole debate has been missing. It lets regulated institutions and private individuals use the exact same chain, each revealing only what they must, not a bit more.

A pure upgrade

Today’s public chains are essentially a Google Sheet: charging you rent while exposing everything to strangers to read. The version that keeps your secrets is a pure upgrade, and it’s what finally brings the next trillion on-chain.

Let’s be honest about what most crypto products actually provide today. Strip away the consensus mechanism, and a public chain is a shared Google Sheet of everyone’s transactions, except slower, more expensive, and readable by every competitor and predator on earth.

The only additional value over an actual Google Sheet is decentralized consensus: the guarantee that nobody can secretly change a row. That guarantee is real and valuable. But today, it’s the only value add.

Every exchange, every DeFi protocol built on a major public chain is, at bottom, renting out this one property.

Add provable compliant privacy, and it’s no longer a worse spreadsheet. It becomes something that has no analog in the old world: a shared machine that can confirm a transaction is real without leaking what the transaction is.

We accept this pattern elsewhere: an encrypted email can prove it was delivered without broadcasting the contents to the street. Money has no reason to be the only exception.

On almost every dimension serious capital cares about, “privacy by default + provable compliance” is a pure upgrade over the status quo. Same consensus, same settlement, just without the leak.

The common rebuttal here is that the current crypto crowd doesn’t seem to want this; they trade just fine, the current products clearly work for them.

Exactly, that’s the point. Early adopters will only be the people the current version already serves. They’re not the missing market. The missing market — those institutions, those treasuries, the normal people who would never publish their bank statements — sits on the other side of these two flaws.

Close these two flaws, and you get the bridge that finally crosses the chasm, flipping a multi-trillion-dollar financial system onto the rails it was secretly built for all along.

The most powerful cryptographic system ever built is finally learning how to keep a secret. That changes everything.