By|Azuma(@azuma_eth)

Last week, Odaily Planet Daily published an article titled "The First Prediction Market Stock Appears!", which primarily mentioned that Robinhood is intercepting orders that previously needed to be executed via Kalshi by building its own prediction market, Rothera. This move aims to reduce revenue sharing with Kalshi and retain profits within its own ecosystem.

Although it was anticipated that Rothera would not face the typical cold start problems of other competitors, its data performance over the past week has still far exceeded our previous expectations. After all, it's hard to imagine that a platform, just launched half a month ago, could directly parachute into third place in the highly competitive prediction market track, trailing only the two giants, Kalshi and Polymarket.

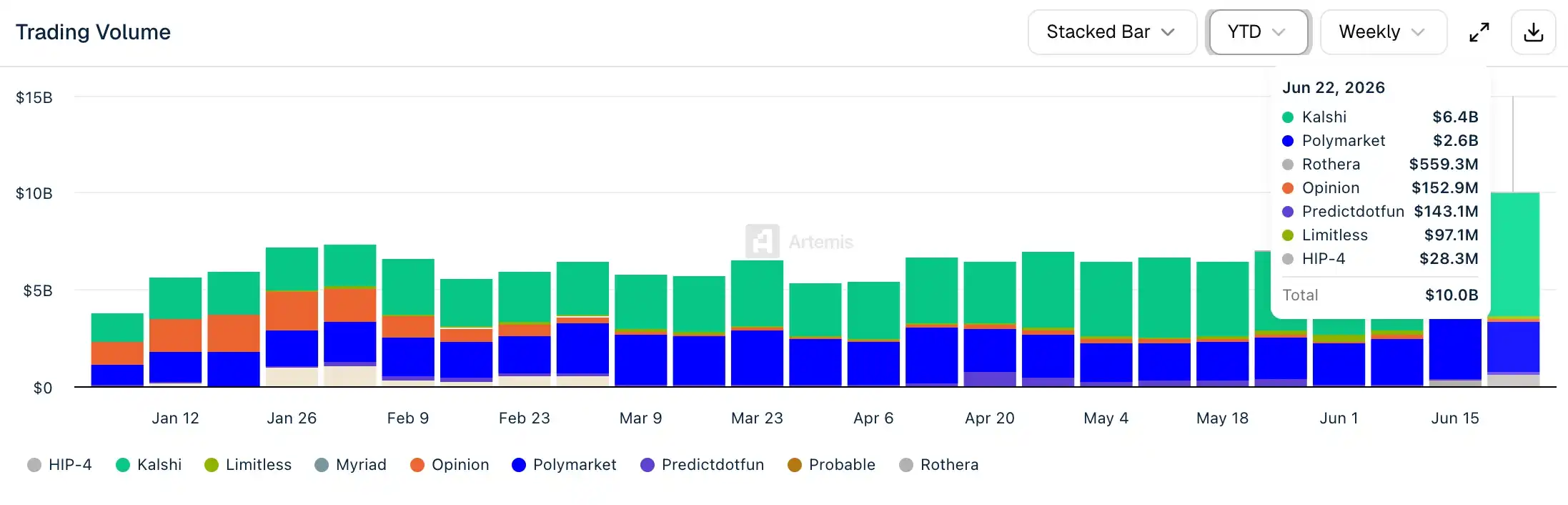

Data from Artemis shows that for the week ending June 8th, as a new platform, Rothera's weekly trading volume was only $21.9 million, still showing a significant gap compared to second-tier platforms like Opinion, Predict, and Limitless. However, for the week ending June 15th, Rothera's weekly trading volume directly jumped to industry third place, reaching $276 million. In the latest week ending June 22nd, Rothera's weekly trading volume has increased to $559 million, almost one-fifth of Polymarket's.

Atypical Growth Case (Can skip if you've read the previous article)

It's important to clarify that Rothera's rise is essentially not due to creating incremental users (though some users may have entered due to the World Cup), but rather a migration of existing orders, not the creation of new users.

Over the past year or so, Robinhood has been one of Kalshi's most important distribution channels. Leveraging tens of millions of retail users and mature access to stock, options, and cryptocurrency trading, Robinhood has funneled a large volume of orders to Kalshi. Piper Sandler analysts estimated that trades completed through the Robinhood channel accounted for about 25%-35% of Kalshi's total trading volume.

The problem is that while these orders came from Robinhood users, they didn't belong to Robinhood itself. Under the previous cooperation model, Robinhood acted more like a front-end traffic portal, while Kalshi was the true infrastructure provider responsible for matching, clearing, and settlement. Revenue generated from each transaction needed to be shared between the two parties.

Rothera is the weapon Robinhood is using to break this profit-sharing model. Since early this month, Robinhood has begun migrating some World Cup-related event contracts to be executed internally on Rothera. This means a large volume of orders that might have previously gone to Kalshi are now retained within Robinhood's own system.

Therefore, in a sense, the surge in Rothera's trading volume is less of a threat to other prediction markets like Polymarket, Predict, or Limitless, and more akin to directly "draining blood" from Kalshi.

Robinhood's Value Capture

The rapid growth of Rothera most directly strengthens Robinhood's ability to capture value from prediction market-related orders on this platform.

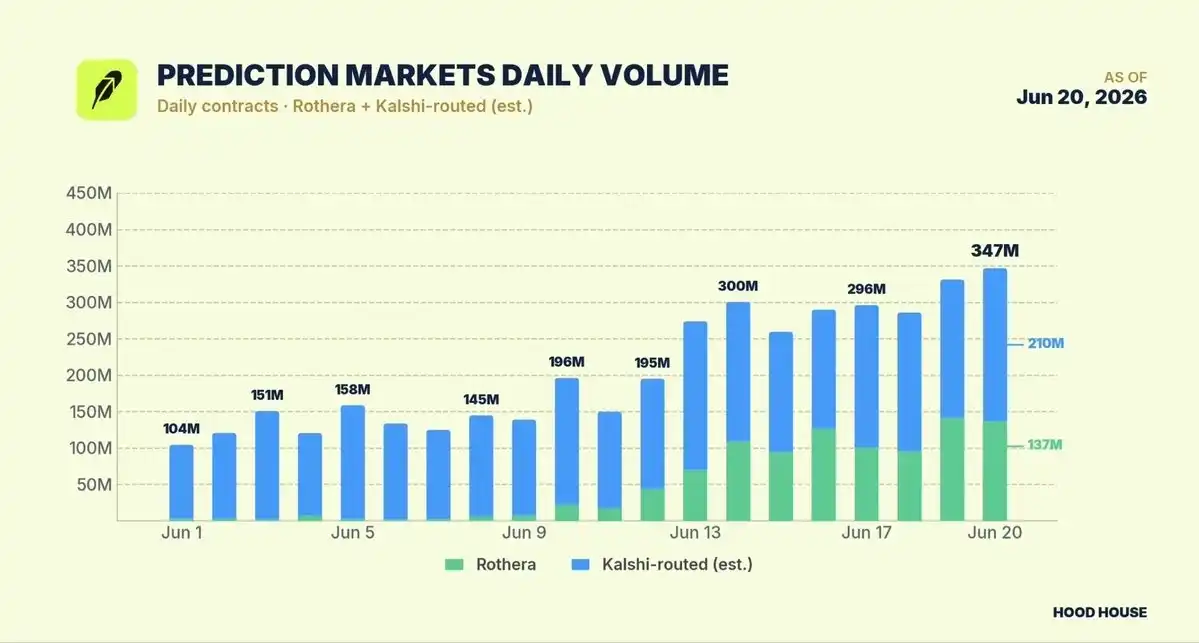

Hood House, an investment research media outlet long tracking Robinhood, combined public data to state that as of June 20th, Robinhood's prediction market business traded a total of 34,700 contracts daily, corresponding to daily revenue of approximately $4.9 million.

Hood House then disclosed its calculation logic:

- Rothera (primarily hosting World Cup-related markets) daily trading volume had reached 137 million contracts, corresponding to a trading value of approximately $47 million;

- For comparison, Kalshi's total daily trading volume was about 1.5 billion contracts, corresponding to a trading value of about $416 million; excluding World Cup-related markets, Kalshi's trading volume was about 1 billion contracts, corresponding to a trading value of about $260 million;

- Considering that Robinhood users still contribute about 20% (a conservative estimate) of Kalshi's non-World Cup market trading volume, this means that about 210 million contracts and $52 million in trading value from Kalshi's non-World Cup related event contracts were completed via Robinhood.

Hood House further made an aggressive estimate based on this, stating that if this growth rate continues, Robinhood's prediction market business has the opportunity to achieve revenue on the scale of billions of dollars this year. This figure even surpasses the historical peak of Robinhood's cryptocurrency-related revenue, which was approximately $900 million achieved in 2025.

Kalshi's Countermeasure: Finding New Channels

Faced with Rothera's rapid rise, Kalshi is clearly aware of the problem.

For Kalshi, Robinhood was both a partner and one of the most important traffic sources in the past. However, as Robinhood begins migrating more and more orders to its own platform, the relationship between the two has become one of direct competition.

A recent piece of news disclosed by The Information may reveal Kalshi's response strategy. Informed sources revealed that Kalshi has begun early, informal discussions with several investment banks regarding a potential future IPO. More notably, Kalshi has presented a clear requirement in its communications with these banks — to be considered for underwriting qualifications in the future IPO, these institutions need to prioritize completing technical integration of their systems with Kalshi. This would allow their institutional clients to directly participate in trading event contracts on the Kalshi platform.

In other words, Kalshi is leveraging the IPO opportunity to find new distribution channels, integrating prediction markets into the client networks of banks, brokerages, and other financial institutions. This also represents a subtle change occurring in the competitive landscape of the prediction market industry. In the past, the focus was on who could offer more contracts or design better products. Now, as prediction markets gradually move into the mainstream financial system, the competitive focus is shifting to another dimension — whoever controls the user access points can more effectively control value.

The rise of Rothera has already demonstrated the significance of distribution capability. Parachuting into third place in the track seems effortless. Challenging Kalshi and Polymarket in the future may not seem like an impossible task either.