Bitwise CIO Matt Hougan says the crypto market is anchored to the wrong mental model. Speaking on the Empire podcast recorded 5 December and released on 8 December, he argued that the traditional “four-year Bitcoin cycle” has lost its explanatory power – and that 2026, which many expect to be a brutal post-halving down year, is far more likely to be an “up year” driven by institutional flows and regulatory tailwinds.

“2026 will not be a bad year, Jason,” Hougan told host Jason Yanowitz. “I think 2026 will be a good year [...] I just don’t understand the logical reason why [the four-year cycle] would repeat again. It’s not like built into a mechanical clock. It was driven by specific factors and those factors no longer exist, so it won’t keep happening.”

He acknowledged that recent price action has unnerved investors, with Bitcoin giving back a “Vanguard pump” and selling off into a weekend on no obvious news. But he framed that as positioning and microstructure, not the start of a structural unwind.

“People in crypto over the last two months have learned to be nervous on weekends,” he said, pointing to thin weekend liquidity and Friday macro headlines. He noted that sentiment is depressed even though “the market is flat for the year,” adding: “We’re freaking out about a market that is flat for the year.”

Why The 4-Year Crypto Cycle Is Dead

Hougan broke down the four main explanations traditionally used to justify the Bitcoin cycle and argued each is now materially weaker.

First is the halving itself. “The halving cycle is just not that important,” he said. “It’s half as important as it was four years ago [...] a fraction of, you know, a quarter as important as it was eight years ago, a sixteenth, etc. There’s just not that much supply being removed.” As issuance becomes a smaller fraction of total supply and ETF and derivatives flows grow, the mechanical supply shock carries less weight.

Second is the rate cycle. Prior “down years” such as 2018 and 2022 coincided with aggressive rate hikes. “Interest rates are going down,” he said. “So that thesis is just completely invalidated, right? It’s completely different.”

Third is the “blow-up” pattern – Mt. Gox, ICOs, FTX – that historically capped euphoric phases. Hougan allowed that balance-sheet stress in parts of the market is “the strongest case for the four-year cycle repeating,” but he does not expect forced liquidations on the scale of prior collapses. In his view, potential problem entities are more likely to “just not buy as much in the future” rather than being compelled sellers.

Fourth is simple randomness: three similar cycles do not make a law of nature. “Across those four, they’re all much weaker than they were in the past,” he summarised.

Why 2026 Is Poised To Be Better Than 2025

Against that, Hougan set what he sees as a once-in-a-generation shift in regulation and institutional behaviour. “You have a once-in-a-generation regulatory change from severe regulatory headwinds to strong regulatory tailwinds,” he said, and “more importantly, you have this institutional adoption narrative that’s going to overwhelm everything.”

In the last six months, he noted, major US wirehouses have “green-lit crypto exposure.” He singled out Bank of America: “They have $3.5 trillion in assets. One percent is $35 billion. Four percent is like $140 billion. That’s more than the total flows into Bitcoin ETFs so far.” He stressed it is not just one bank: “There are four wirehouses. They’re basically all on now [...] the biggest advisory groups all managing many trillions of dollars.”

The catch is timing. Institutional allocations are slow and process-driven. “The average Bitwise client, I think, invests after eight meetings with us,” he said, and some of those are quarterly. That “eight-meeting” lag means the ETF era is still in its early innings; the full impact of platforms being switched on is more likely to manifest through 2026 than in a single explosive quarter.

Hougan also emphasised that advisers optimise for client retention, not absolute performance. “The one thing a financial adviser doesn’t want to do is have a meeting with their client where something is down 50% and their client fires them,” he said. That is why reduced volatility, cleaner regulation and mainstream narratives like “Bitcoin as digital gold” and “stablecoins and tokenization as new financial rails” matter so much.

On supply dynamics, he pushed back on two recurring fears: “OG whales dumping” and MicroStrategy as a forced seller. He argued that much of the apparent “selling” by long-term holders is actually upside being sold via covered calls. Whales come to Bitwise and similar firms, he said, saying: “I have a hundred million of Bitcoin [...] can you write covered calls against this?” That “effectively introduces new supply into the market” without coins moving on-chain.

On MicroStrategy, he was categorical: “From a data perspective [it is] just strictly untrue that it will be forced to sell its Bitcoin.” The company has meaningful cash to service interest, no principal due until 2027, and manageable maturities relative to its Bitcoin holdings. He agreed with Jeff Dorman’s framing that MicroStrategy is no longer a major marginal buyer but also “not a forced seller.”

Too much pessimism on the timeline.

Brought on @Matt_Hougan to tell us why 2026 will be FAR better than 2025.

Tons of good nuggets in here related to institutions, financial advisors, cycles, and more.

Enjoy the optimism!pic.twitter.com/WZJb55yENF

— Yano 🟪 (@JasonYanowitz) December 8, 2025

Looking ahead, Hougan expects investors to eventually reframe the current period not as a failed bull cycle but as a behavioural transition through a key level. “We might look back at 2025 at some point and say, ‘Huh, you know what? $100,000 was like a big behavioral cliff we had to get over. Took us like a year,’” he said.

For 2026 specifically, his message is clear: the old four-year pattern “won’t keep happening,” and the combination of regulatory clarity and institutional inflows sets up what he calls an “extraordinarily strong” backdrop rather than a programmed bust.

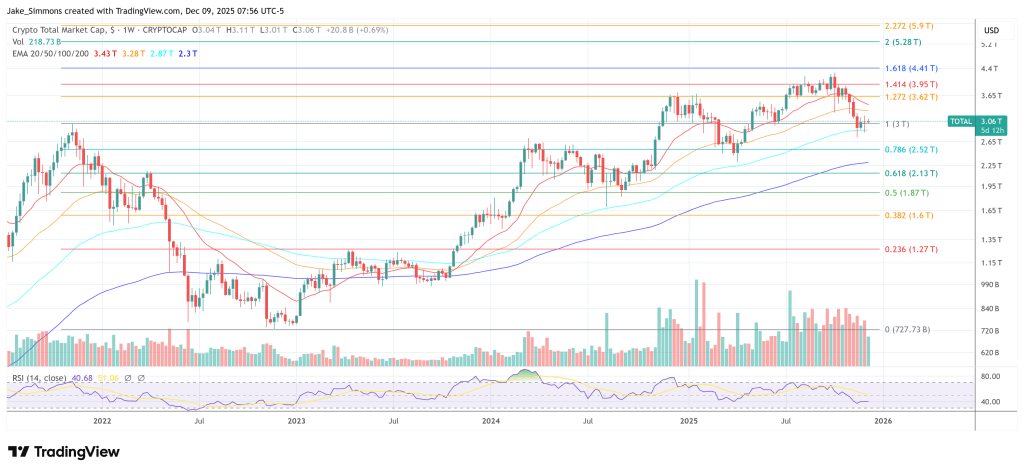

At press time, the total crypto market cap stood at $3.06 trillion.

Featured image from YouTube, chart from TradingView.com