Written by: Charlie

Compiled by: Block Unicorn

Lately, our discussions have touched less and less on cryptocurrency. We end up talking about lending businesses, AI subscription models, and the payment channels that Stripe and Mastercard are fighting over. Last Friday, we discussed how the upcoming trillion-dollar IPOs of OpenAI, SpaceX, and Anthropic will affect broader financial markets. Even when a cryptocurrency project is mentioned, halfway through the discussion, you realize that no one has mentioned "token price."

This shift is also reflected in our recent reporting content. In the past two weeks, our reporting focus has shifted to stories from the fringes of the cryptocurrency space. For example, fintech companies using blockchain as infrastructure, consumer products where tokens serve as distribution mechanisms rather than the product itself, and cases of infrastructure companies with valuations unrelated to cycles being acquired. Whether Bitcoin is $100,000 or $70,000, these developments continue to advance.

This article was originally published by Hepworth Iron Capital. This week's piece builds a framework for this phenomenon. Charlie Booth argues that the era of cryptocurrency as a single Bitcoin-sensitive factor is ending, paving the way for a new cycle driven by non-cryptocurrency factors rather than cryptocurrency prices.

Historically, cryptocurrency trading has been one of the factors sensitive to Bitcoin's price. But that situation is ending.

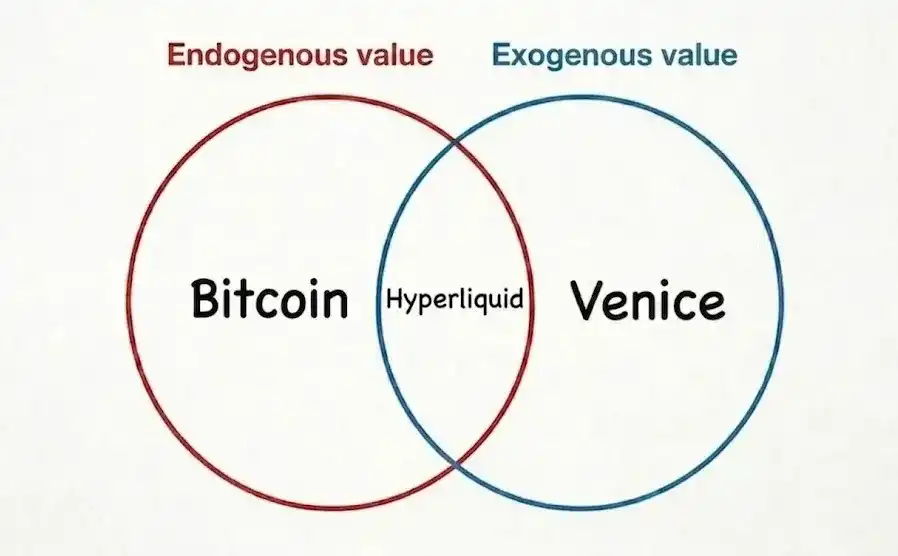

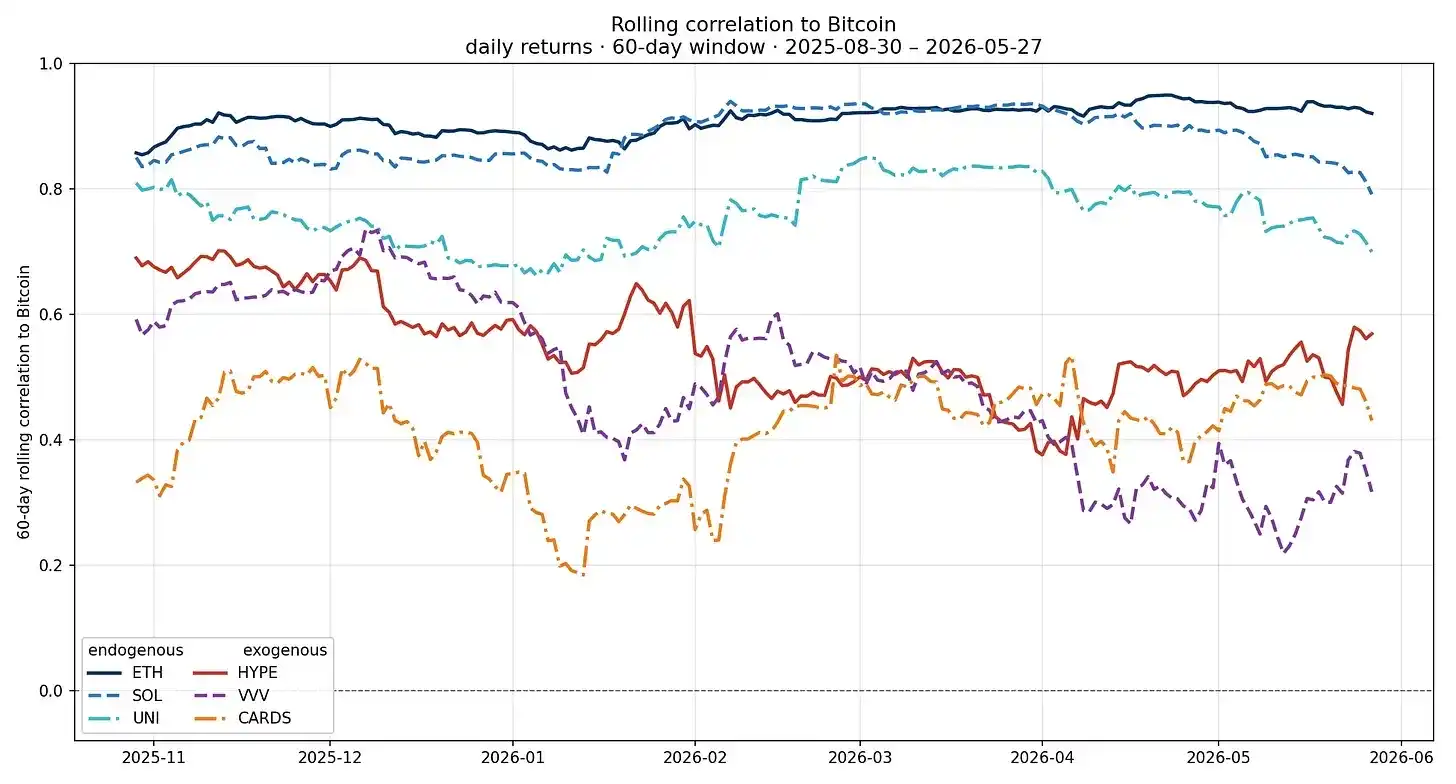

The crypto economy is bifurcating into two types: an endogenous economy and an exogenous economy.

The former is traditional cryptocurrency: the value of tokens and projects depends on the price of cryptocurrency. The latter is just cryptocurrency in name, with its value increasingly detached from cryptocurrency prices.

Bitcoin's value stems from its characteristics, which are reflected in its price. Price increases reinforce people's perception of its characteristics. At the peak of a bull market, Bitcoin is seen as an interstellar currency, the scarcest digital credential known to mankind. At the trough of a bear market, it's viewed as a digital collectible without any cash flow.

Hyper-liquidity lies between the endogenous and exogenous groups. Most of its business still relies on cryptocurrency prices, but both supply and demand are expanding. Much of the on-chain financial infrastructure resides here, with underlying assets shifting toward tokenized real-world assets.

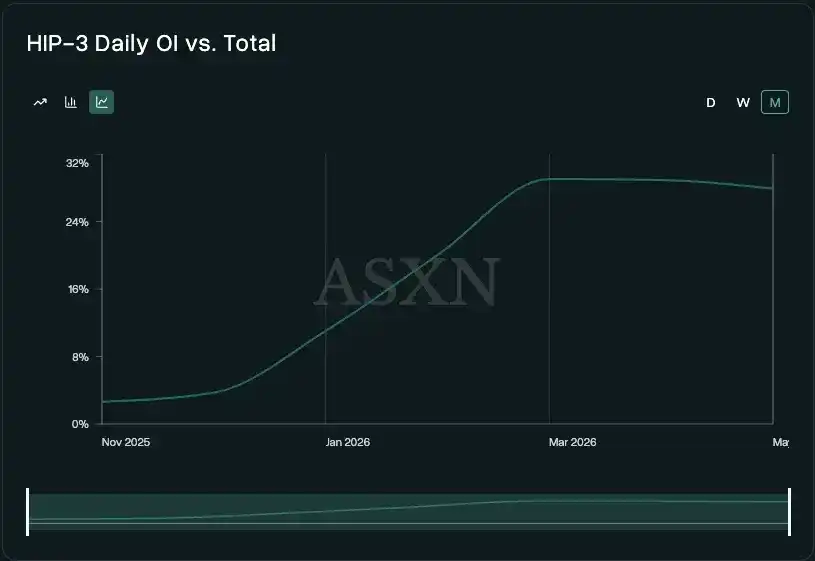

HIP-3 open interest can roughly represent non-cryptocurrency-related open interest. HIP-3 accounts for about 30% of total hyper-liquidity open interest, up from about 4% in November 2025. HIP-4 (Outcome Markets) is expected to further drive this ratio while attracting new demand (traders) and new supply (markets, assets).

Looking at purely exogenous factors, the drivers behind projects like Venice are completely independent of the cryptocurrency market. While user profiles overlap, their business model resembles consumer-facing AI more than Uniswap. Uniswap still primarily relies on users trading assets with endogenous value, making its business closely tied to the price of those assets. Venice, on the other hand, packages private multimodal reasoning into a "use + subscribe" model.

Venice's only connection to cryptocurrency is its choice of tokens as a tool to measure business value, and the fact that some of its derivatives suppliers happen to have a cryptocurrency label. Perhaps, this is also influenced by the deep understanding of cryptocurrency held by Venice's manager, Erik Voorhees, who believes that if applied properly, tokens can be excellent marketing tools.

Figure 1 is a simple example from the listed equity space: a fintech lender using its self-developed blockchain to reduce home equity loan approval time to under five minutes. Blockchain technology is incidental; the business model is key.

The large-scale emergence and growth of the exogenous category in both listed equity and token markets are significant. Historically, purely bottom-up investing has been difficult to achieve because most business models were highly sensitive to cryptocurrency prices. Cryptocurrency has never been devoid of exogenous narratives; every "blockchain, not Bitcoin" cycle promised such narratives. But in most cases, these narratives eventually reverted to the cryptocurrency beta category because demand never truly materialized, revenue didn't materialize (and if it did, it wasn't absorbed by tokens), and once token prices stopped rising, there was nothing left behind.

What's different this time is that you can answer who is paying and why, demand is measurable in many cases and is less reflexive, and the performance of tokens as a tool is gradually improving (more on this later). Venice's registration revenue is real money users pay for inference. When cryptocurrency prices fall, there's no obvious reason for it to reverse because it was never a function of price. You now have two things previous cycles lacked: sustained usage, and buyers investing based on fundamentals rather than just narrative.

Take the stablecoin sector in private markets as an example. In March 2026, Mastercard agreed to acquire BVNK for up to $1.8 billion, just 15 months after BVNK completed its Series B funding with a valuation of $750 million. According to Stripe's annual letter, Bridge (acquired by Stripe for $1.1 billion in February 2025) grew fourfold annually within Stripe. This growth is unrelated to cryptocurrency cycles.

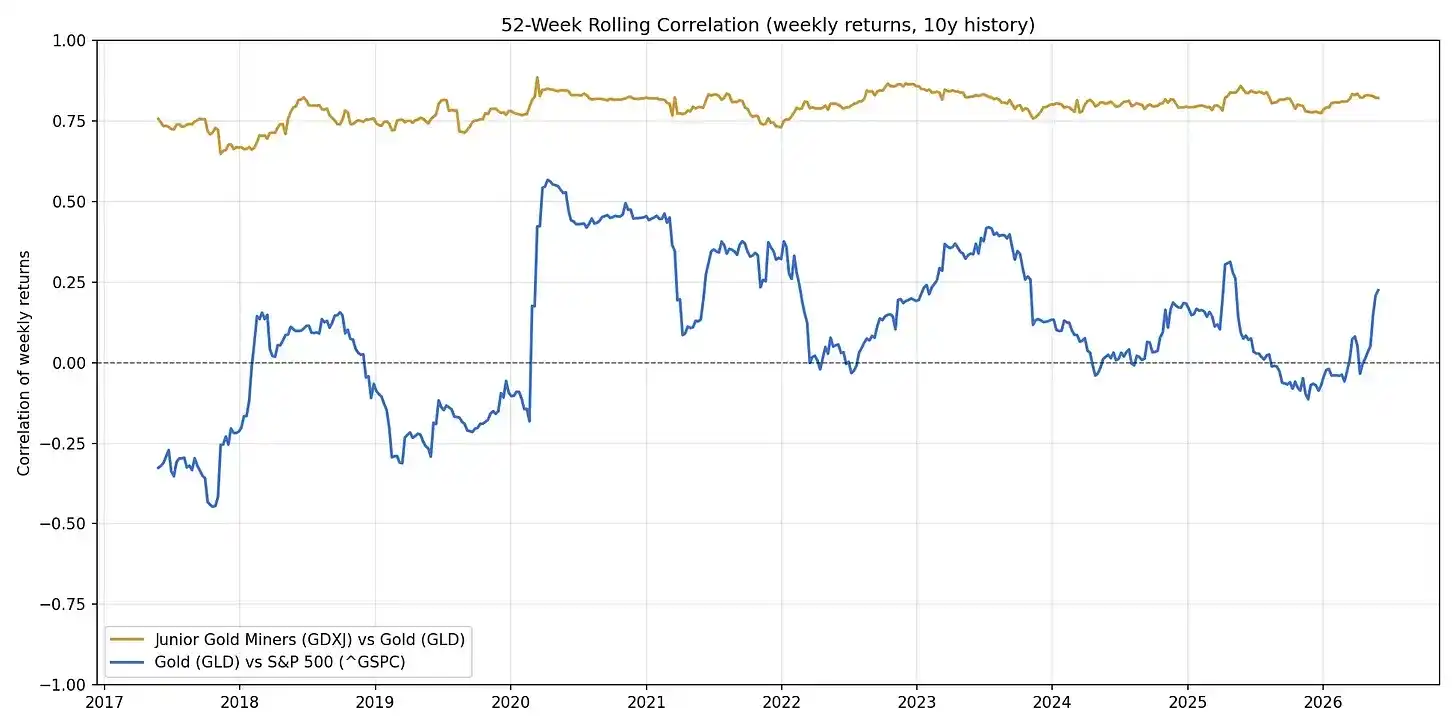

This is not a bearish prediction for the endogenous asset class. Just as gold, and even small gold mining companies, have their place in an investment portfolio, Bitcoin and endogenous asset classes have their value and timing. But fundamentally, different drivers may continue to affect their performance and correlation. You can see these two relationships in the data:

This metaphor can be visualized: small gold miners have a correlation with gold that rarely strays beyond the 0.75 range. Cryptocurrency now trades much the same way: small miners correlate with Bitcoin like gold, while leveraged trades bet on the same underlying asset. The blue line represents another relationship. Gold and the S&P 500 have some macroeconomic correlation, but they trade based on their own distinct drivers. This is the ultimate destination for exogenous asset classes. Over time, these assets should shift from the gold-related line toward the blue line, transitioning from leveraged proxy assets to independent assets occasionally correlated with economic conditions.

These exogenous names are examples, illustrating the point and also serving as exceptions to it.

Many "endogenous" assets still move closely with Bitcoin. Some exogenous assets have declined, but the time window is too short to mean anything yet. Fundamentals change first; correlation changes later.

This changes the analytical approach. The exogenous category needs underwriting like any ordinary business: who pays for the product, how unit economics work, and where the moat is. Bitcoin price is no longer the most important variable; your analysis sounds like that of a fintech investor with strange custody arrangements.

Some exciting "exogenous" categories, in no particular order, with various notes:

- On-chain exchanges and brokers

- Credit / redemption solutions for long-tail tokenization (Grove Basin looks interesting in this regard)

- Real crypto x AI (private inference, distributed open-source model training, similar to Nous Research's Psyche)

- Neobanks (I prefer more privacy-focused platforms like Payy and Raycash, and the programmable privacy infrastructure supporting them, like Aztec and Zama, is also interesting).

- Lending (Morpho is becoming the institutional standard akin to the repo market, while smaller companies like Valinor and 3jane target interesting niches in private credit)

- Stablecoin and real-world asset / tokenization issuers

- Payment channels (In broad payment channels, Stripe and Tempo are currently the ones to beat; in proxy payments, it's currently Coinbase).

- Non-financial consumer crypto (e.g., products like Venice and Collector Crypt, these special cases show that assigning value from non-crypto businesses to tokens can enhance market value and adoption).

- Agent economy (The key lies in the coordination between access-layer agents and suppliers/creators, which is less fungible than the rails. Cloudflare is well-positioned, but whether it taxes traffic or merely sells switches remains to be seen).

Currently, the most enduring way to invest in this theme is equity, not tokens. Quality tokens are the exception; they can play a larger role only if the tokens themselves improve, which requires joint efforts from regulators and the industry. There's been some progress on both regulatory and transparency fronts: the CLARITY Act on the regulatory side, and efforts by companies like Blockworks to improve transparency. Tokens have a long way to go.

None of this changes the key point. The drivers are shifting from a single factor to multiple factors; the work is no longer interpreting Bitcoin charts but funding businesses. Don't be confused in the next decade about why "cryptocurrency" no longer moves in unison as it once did.