TL;DR

U.S. stock investors now face a problem that goes beyond simple bullishness or bearishness.

On one side is Bank of America's US Equity & Quant Strategy team. Led by Savita Subramanian, the team released a client report on June 5th titled 'Too many red flags. Take profits.' According to a June 9th report by Axios, the report argues there are too many risk signals in U.S. stocks and offers a more direct position suggestion: take profits.

On the other side, there are still strong AI fundamentals. Microsoft, Google, Amazon, and Meta are still increasing AI and data center capital expenditures, and Nvidia's data center demand remains the core anchor of the semiconductor cycle. Unlike the 2000 dot-com bubble, the leaders of this rally have been replaced by giants with cash flow, profits, cloud revenue, and chip orders.

So the real question has shifted from 'Is AI a bubble?' or 'Is BofA calling a top?' to another, harder-to-answer question: when historical top signals and real AI growth coexist, how should investors understand the current risks in U.S. stocks?

The answer may be more uncomfortable than simply being bearish: the AI bull market may not be over, but it has moved from the 'buying growth' phase to the phase of 'testing the speed of growth realization.'

BofA Warns of Worsening Odds

The value of BofA's report lies in placing the current market within a historical risk structure, not in giving a precise top timing.

According to numerous financial media outlets citing the BofA report, about 70% of its tracked 10 bear market warning signs have been triggered. This ratio is close to the average level before multiple S&P 500 tops since 1990. The BofA framework also shows that the S&P 500 is statistically overvalued in 17 out of 20 valuation metrics, with 8 higher than the peak of the 2000 internet bubble. The CAPE (Cyclically Adjusted P/E Ratio) or P/E10 is around 40, residing in a historically extreme range.

Each of these numbers can be refuted individually. High valuation doesn't mean a decline tomorrow. Effective historical signals don't mean they're right every time. Stronger profits from AI companies do indeed make today different from 2000. But when valuation, market breadth, style divergence, and momentum simultaneously show extreme readings, BofA's main point is closer to: the market can still be held, but the odds have worsened.

Market breadth is key here. The indices are still high, but the rally relies increasingly on a handful of AI and tech leaders. The current U.S. market shows narrow leadership characteristics similar to historical top phases: a few stocks contribute the majority of index gains, the proportion of S&P components above key moving averages is receding, and many individual stocks are not near their own highs. Strength at the index level masks declining internal participation.

Style divergence reinforces the same signal. BofA noted that the median return differential between the top quintile and bottom quintile of tech stocks is about 120 percentage points, the highest since February 2000, approaching the 130 percentage points just before the March 2000 peak. This looks more like a concentrated bet by capital on a few certain narratives, rather than the broad dispersion typical of a normal bull market.

For investors holding SPY, QQQ, NVDA, or SOXX, the most dangerous aspect of this structure is reduced margin for error. The indices could certainly continue to rise, but as gains depend more on fewer stocks, any deviation in a leading company's earnings, guidance, capex returns, or valuation assumptions could be amplified into a pullback for the entire portfolio.

This AI Rally Can't Simply Mirror 2000

Looking only at BofA's valuation and breadth signals, it's easy to directly compare the current rally to 2000. But that comparison is only half right.

The typical feature of the 2000 internet bubble was that many companies lacked mature business models, and investors mainly traded on the imagination of 'the internet changing the world.' Today's AI leaders are different. The cloud and AI businesses of Microsoft, Google, Amazon, and Meta are already reflected in real revenue, capex plans, and data center demand. Nvidia is not just a narrative center but also a chip supplier with highly concentrated profits and cash flow.

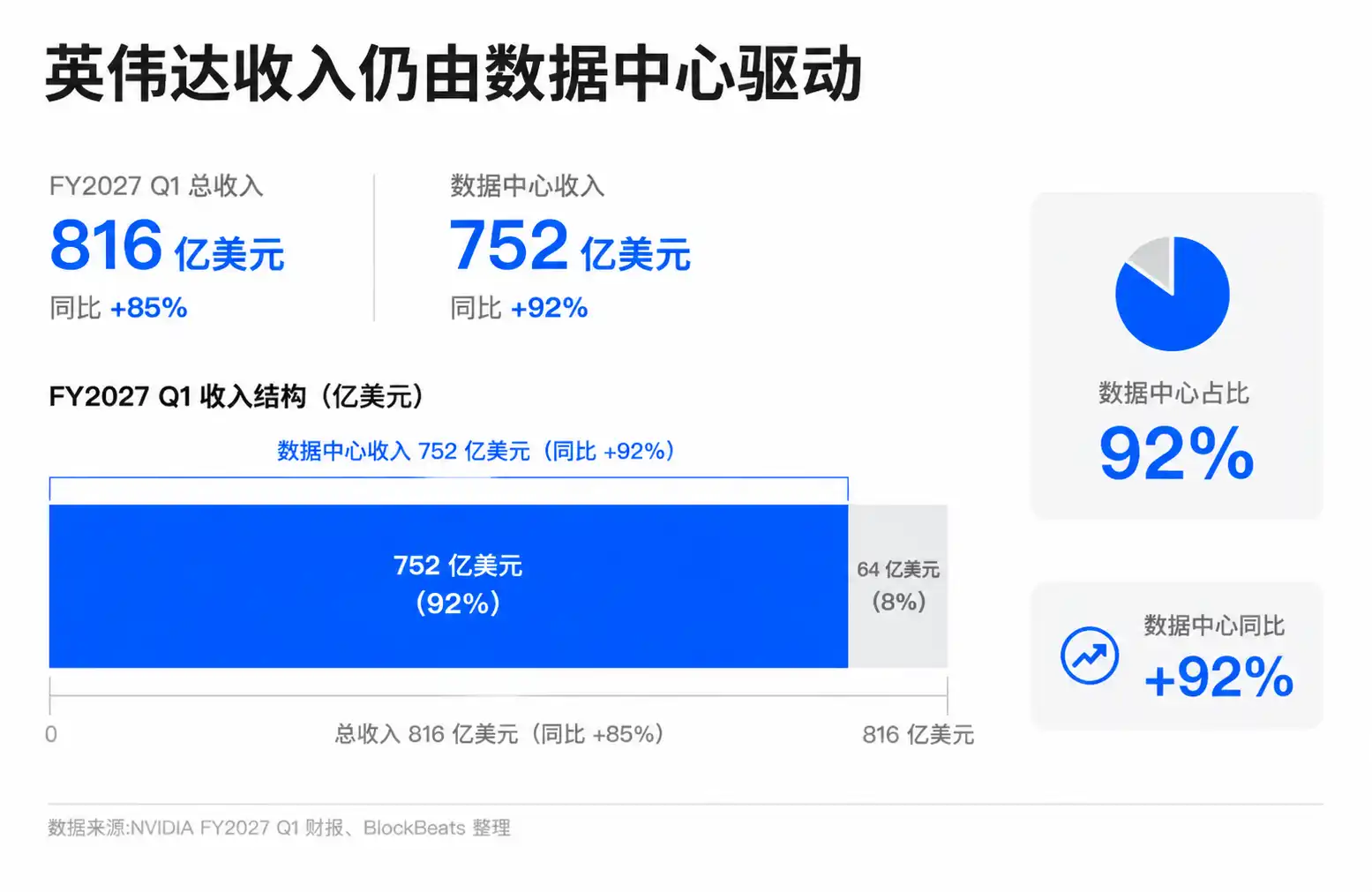

Nvidia's latest earnings report gave bulls their strongest support. The company's FY2027 Q1 report released in May 2026 showed quarterly revenue of $81.6 billion and data center revenue of $75.2 billion, a 92% year-over-year increase. In the face of these numbers, simply calling the AI rally a 'bubble without fundamentals' is not very convincing.

AI optimists, including large tech company management and growth investors, refute the bubble argument precisely based on this. They believe this rally is more like an infrastructure cycle: training and inference demand drives GPU, networking, storage, power, and data center construction; cloud vendors use higher capital expenditures to secure future AI service revenue; and enterprises then integrate AI into software, advertising, search, office, and development processes.

This framework has a factual basis. Over the past few earnings seasons, large cloud vendors have consistently emphasized strong AI demand, with cloud business maintaining growth. Nvidia's data center revenue has become a key pillar of the U.S. earnings growth narrative. Broadcom, AMD, and data center and power infrastructure companies are also incorporated into the same investment chain. The market's willingness to give these companies higher valuations is not just because the story sounds good; orders, revenue, and profits are also being delivered.

This is why BofA's signals cannot be crudely interpreted as 'the AI bull market is already over.' If underlying fundamentals are still improving, a high-valuation regime can last longer than historical experience suggests. Especially in a market where passive funds, index weightings, and institutional allocations collectively reinforce leader status, the strong getting stronger is itself part of the capital flow mechanism.

But AI being real does not equal valuations being safe. A common misconception easily arises here: as long as the technological revolution is real, the price is not expensive. Historically, many bubbles were precisely built on real technology being priced in too early and too fully. The internet truly changed the world, but investors who bought many internet stocks in 2000 still experienced prolonged valuation compression.

The core divergence in the current AI rally is shifting from 'Is AI useful?' to 'How many years of future good news has the market already priced in?' The importance of BofA's historical signals lies precisely in reminding investors: even if fundamentals are real, when the price already reflects too much future good news, risk can still rise.

Pressure Shifts to Revenue and Cash Flow

The AI bull market is entering its hardest phase, not because demand suddenly disappears. The real change is that the market is starting to demand more proof.

Over the past two years, investors were willing to pay high valuations for AI leaders because the growth path seemed clear: cloud vendors increased capex, chip companies sold more high-end GPUs, data center and networking equipment companies received orders, and future enterprise applications would release even greater revenue. Entering 2026, the market needs to see not just continued investment, but also whether that investment can translate into sufficiently high revenue, profit margins, and free cash flow.

Capital expenditure is the focal point of this question. The direction of increased AI and data center investments by Microsoft, Google, Amazon, and Meta is generally clear, but estimates of specific scale vary widely among different institutions and media. More importantly, investors are already starting to worry about the pressure higher capex puts on free cash flow and return on investment. This cannot simply be framed as 'AI investments cannot be recouped,' but as the investment curve steepens, market demands on the return curve will also increase.

For Microsoft, Google, Amazon, and Meta, continuing to increase AI investment is strategically necessary. Whoever stops risks falling behind in cloud, search, advertising, office, models, and developer ecosystems. But from a shareholder perspective, the higher the capex, the more future earnings reports need to prove these investments can bring revenue growth, stable margins, and cash flow resilience.

For the semiconductor chain represented by Nvidia, Broadcom, AMD, and SOXX, the logic is slightly different. They are direct beneficiaries of the AI investment cycle, with orders and profits realized earlier. But precisely because the market already views them as core winners of the AI infrastructure cycle, once downstream cloud vendors slow capex, delay purchases, or start emphasizing investment discipline, semiconductor valuations will react first.

This creates a more fragile feedback loop. Cloud giants increase capex, supporting chip company revenue. High growth from chip companies supports index gains. Index gains and earnings revisions reinforce market confidence in the AI long cycle. If any link in this chain shows signs of slowing, the market may face not an 'AI end,' but more likely a need for valuations to re-match the pace of realization.

Second-Half Earnings Need to Prove Growth Can Cover Risks

BofA's 70% bear market signal won't automatically turn into a top, and strong earnings from AI leaders won't automatically eliminate valuation risks. What really needs to be verified next is whether sustained growth can cover these risk signals in valuation and market structure.

The most direct observation window is the second-half 2026 earnings season. Investors need to see AI revenue from large tech companies continue to grow, while profit margins aren't significantly eroded by capex and depreciation pressures. Cloud vendors, while continuing to invest, also need to prove customer demand is strong enough. The orders and guidance from semiconductor companies like Nvidia, Broadcom, and AMD will reflect whether downstream investment momentum is slowing.

Another variable is market breadth. If the S&P and Nasdaq continue to hit new highs but fewer stocks participate in the rally, and high-P/E stocks continue to systematically outperform low-P/E stocks, the historical top structure BofA mentions will be harder to ignore. Conversely, if earnings diffusion spreads to more sectors and indices no longer rely solely on a few AI leaders, risk signals have a chance to be digested slowly by time and performance.

For ordinary investors, now is a more suitable time to check portfolio positioning and concentration. Using a simple 'bullish on AI' or 'bearish on U.S. stocks' doesn't solve the problem. AI may still be the most important investment theme for the next few years, but with valuations, breadth, and capex pressures simultaneously rising, continuing to hold it has shifted from early trend discovery to a bet on the speed of realization.