Author: David George, a16z Partner

Translation: Yuliya, PANews

Original Title: Only Two Paths Left for the Software Industry: Either 10% Growth with AI-Native Products or 40% Real Profitability

PANews Editor's Note: a16z partner David George published a new article stating that there is no more "middle ground" in the software industry. Companies must choose one of two paths within 12-18 months: achieve over 10% revenue growth through AI-native products or increase real profit margins to 40%-50%. He calls for companies to undergo thorough restructuring, clarify their development direction, and reshape their teams and architecture to adapt to the new AI-driven competitive environment. Otherwise, they will face valuation compression and market pressure.

Below is the full translation:

To CEOs, founders, board members, and investors of software companies: The comfortable middle ground is over.

The public market has repriced the industry, and for good reason. The market is telling us that the terminal value of software is not what it used to be. I don't know what will drive each stock's fluctuations next quarter, but in the medium to long term, I believe there are only two reliable paths to create lasting equity value.

-

Path One: Achieve year-over-year revenue acceleration of more than 10 percentage points through truly new AI-native products within the next 12 to 18 months.

-

Path Two: Restructure the company to achieve real operating profit margins of over 40% (ideally 50%), including stock-based compensation (SBC).

Strictly speaking, these moves are not mutually exclusive. But I believe this 12 to 18-month plan must be an either/or choice. By the end of next year, any state between these two paths of high growth and high profitability will become a no-man's land: facing growth pressure, continuous equity dilution, and compressed valuation multiples. Today's CEOs need clear moves to advance one of these paths as the ultimate goal.

The Adjustment Trick is Over

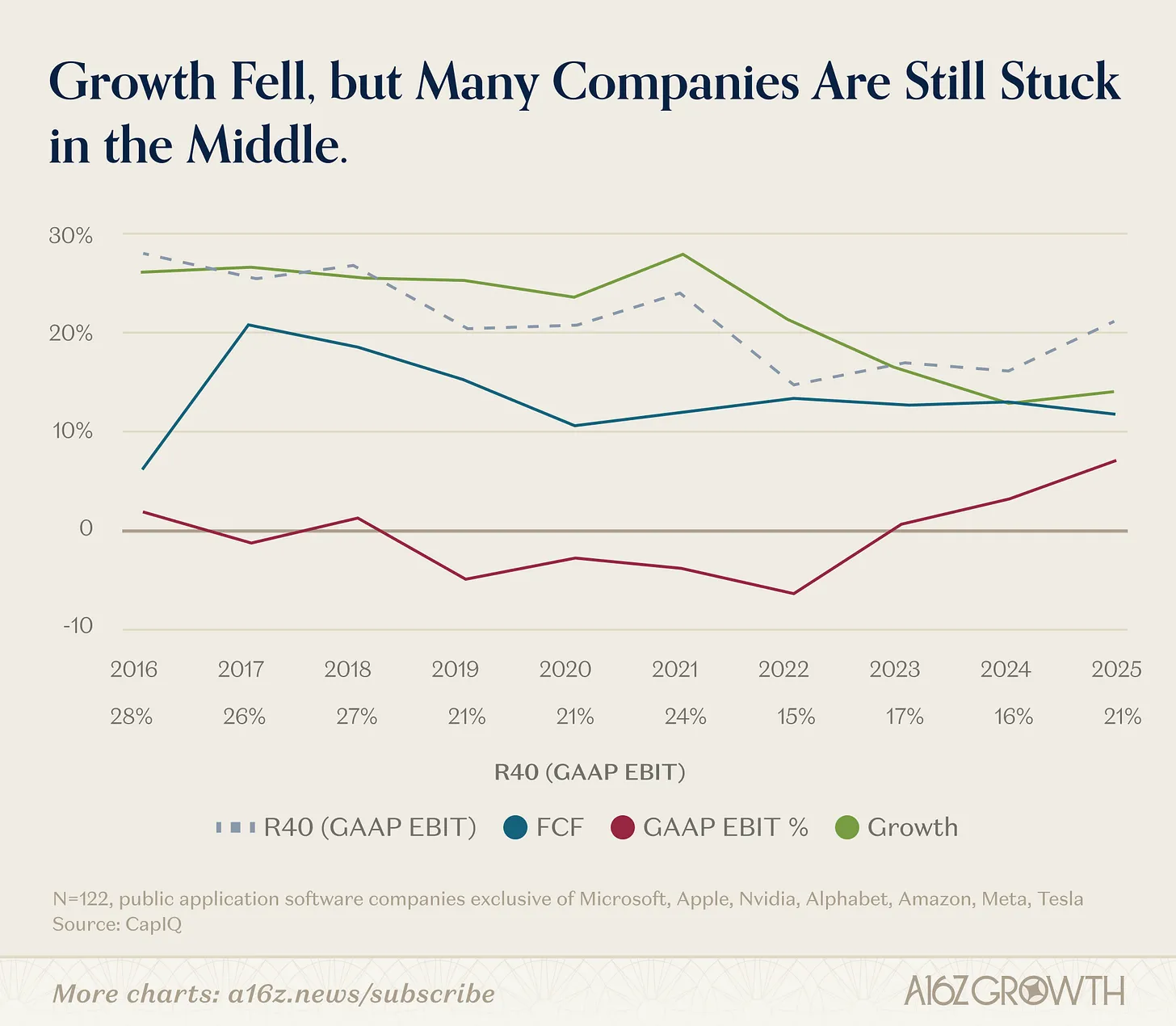

Public software companies have already gone through the first half of the transformation. Growth has slowed, and valuations have compressed. But in most cases, real profitability has not yet arrived.

Yes, free cash flow has improved; GAAP margins have also increased. However, once you treat stock compensation as a real expense, not a permanent exemption, most companies in the industry are still in a difficult middle ground: growth is too slow to deserve the valuation premium of high growth; equity is too diluted to deserve stable valuation multiples.

If revenue growth is slowing, we should see more operating leverage, but again, while we've seen some, it's far from enough.

The reality is, it's time for management to take bold action. And those headlines about "laying off 8% or 10%" are no longer effective. That's just weakness. Weak approaches only trim the edges of the organization without addressing the core issues. In contrast, a stronger approach is to redesign and realign the entire organizational structure and operating model.

In the next 12 months, I expect we will see more strong approaches. You have two choices on how to do this, depending on how you want to restructure your company.

Path One: Accelerate Growth with New AI Products

Accelerating growth with new AI products does not mean attaching a chatbot or Copilot interface to the old SKU list.

It means launching new products within 12 months that can increase the company's total growth rate by 10 percentage points. Equally important, it means you need to restructure your company at the fastest speed, including your executive team, to ensure that after finding product-market fit (PMF), you can quickly seize market opportunities and achieve growth targets.

The first thing you need to do is identify who will be the leaders to help you accomplish this task. This will be a 12-month hard trek, and you need to find out who is willing to go through thick and thin with you. But there is good news: in your organization, there are probably five people who will bring you 100 times more value than you imagine. But your top priority is to find out who these five people are (regardless of their resumes), explain the urgency of the situation to them, and give them a once-in-a-lifetime career opportunity to restructure the company with you.

How should you arrange these people?

First, put them in charge of those unglamorous but crucial information gathering projects:

-

Conduct process capture sprints around each high-value workflow;

-

Collect SOPs, work orders, conversation records, requirement documents, policies, CRM notes, support logs, event data, and approval paths.

Create a dynamic context layer, not a pile of static PDFs. Treat documents as product infrastructure. Establish evaluation mechanisms around accuracy, exception handling, latency, and cost. Immediately put these five people on this task, each with their own area of responsibility.

Over the next month, closely watch your VPs to see who is on the same boat as that team and who is not.

This will tell you everything you need to know: which executives should stay and which need to part ways in the upcoming company restructuring.

At the end of the month, have conversations with the VPs and directors who need to leave. Replace them with the elite team that just completed the information gathering sprint and other AI-native rising stars within the company who have already proven themselves.

Now, you have a refreshed, dynamic executive team ready for battle.

Meanwhile, you need to allocate 50% of R&D resources to brand-new AI products.

Adopt a four-person squad model; merge design, product, and engineering into one working unit, start writing code from day one, limit the number of people, not computing power. Reduce communication costs to as close to zero as possible.

Ensure all your best product managers are as customer-facing as possible. They can't waste a minute. Their job is pure product exploration; ensure they are not hindered by any legacy issues.

Meanwhile, your best engineers will remain in the central engineering organization, reporting directly to the CTO. Their job is to ensure the company's core engineering architecture can evolve as fast as the pace of the pioneering product managers.

It may vary from company to company, but my advice is not to put all your best engineering talent on the edge. It's tempting, but this will fragment your tech stack and create years of technical and organizational debt that will kill any early promising progress.

Furthermore, in AI, you don't need the best engineers for new product exploration; you just need people who can deliver and learn quickly. The best engineers should keep an eye on the overall technical architecture of the company but ruthlessly prioritize new things.

As part of this sprint, your company needs to be very good at escalating contentious decisions to remove obstacles to progress. If you can't make tough choices every week, you won't be able to complete this transformation in 12 months and successfully build a new AI-native business. So, master this process and ensure your newly formed executive team dedicates a significant amount of time (at least a full day per week) specifically to removing obstacles for designers, product managers, and engineers, as if the company's survival depends on it.

In the process of removing obstacles for the team, you will figure out exactly what your new business model is. It needs to make money through tokens/per-use, not the old per-user model. You do have some time: the per-user model won't disappear overnight. But you need to take this challenge seriously: you can't be perfunctory about new pricing models and product interfaces. If an Agent cannot autonomously use and pay for your product, then you probably haven't hit the target yet.

Budget for new spending exists. You can do this.

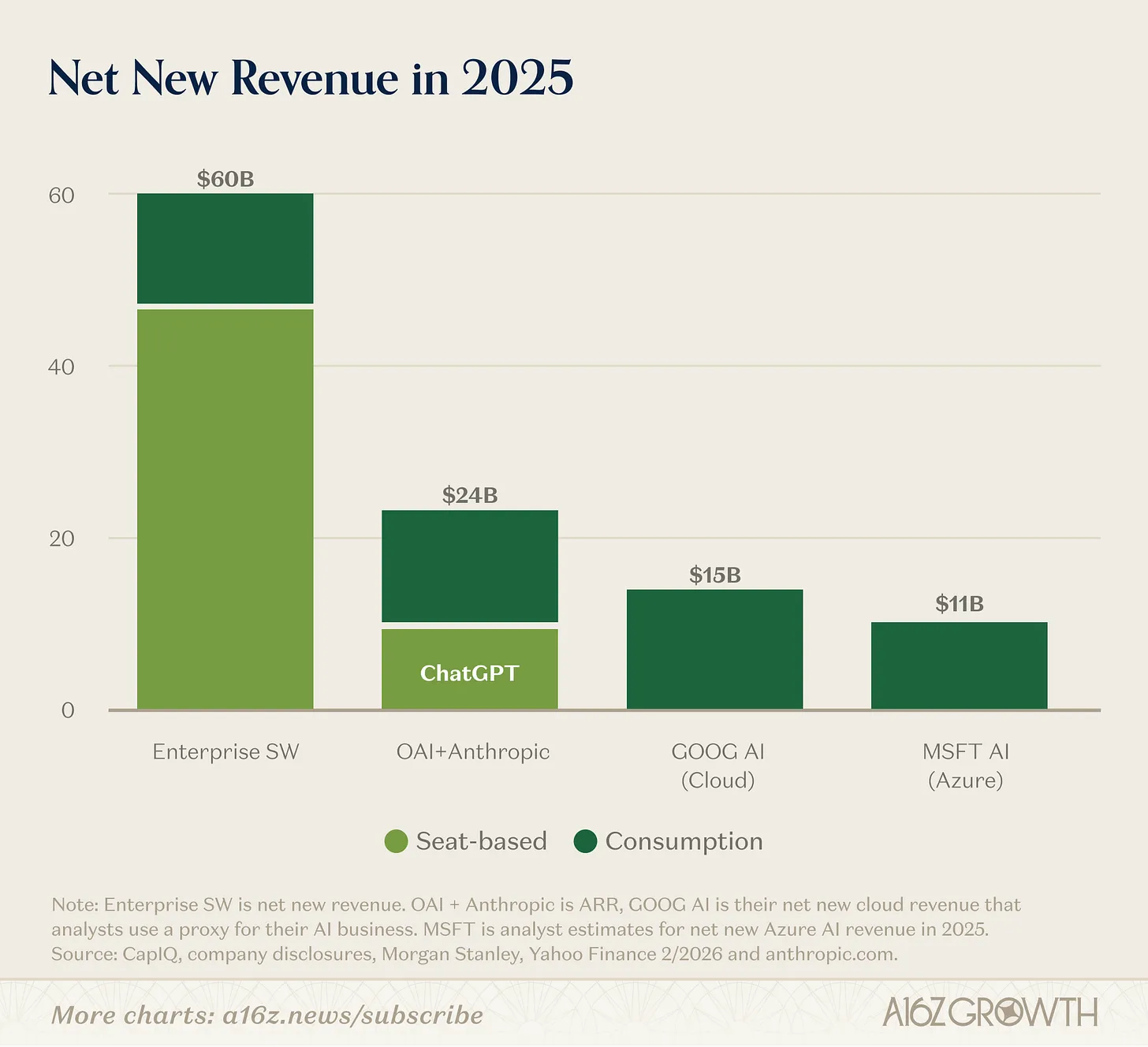

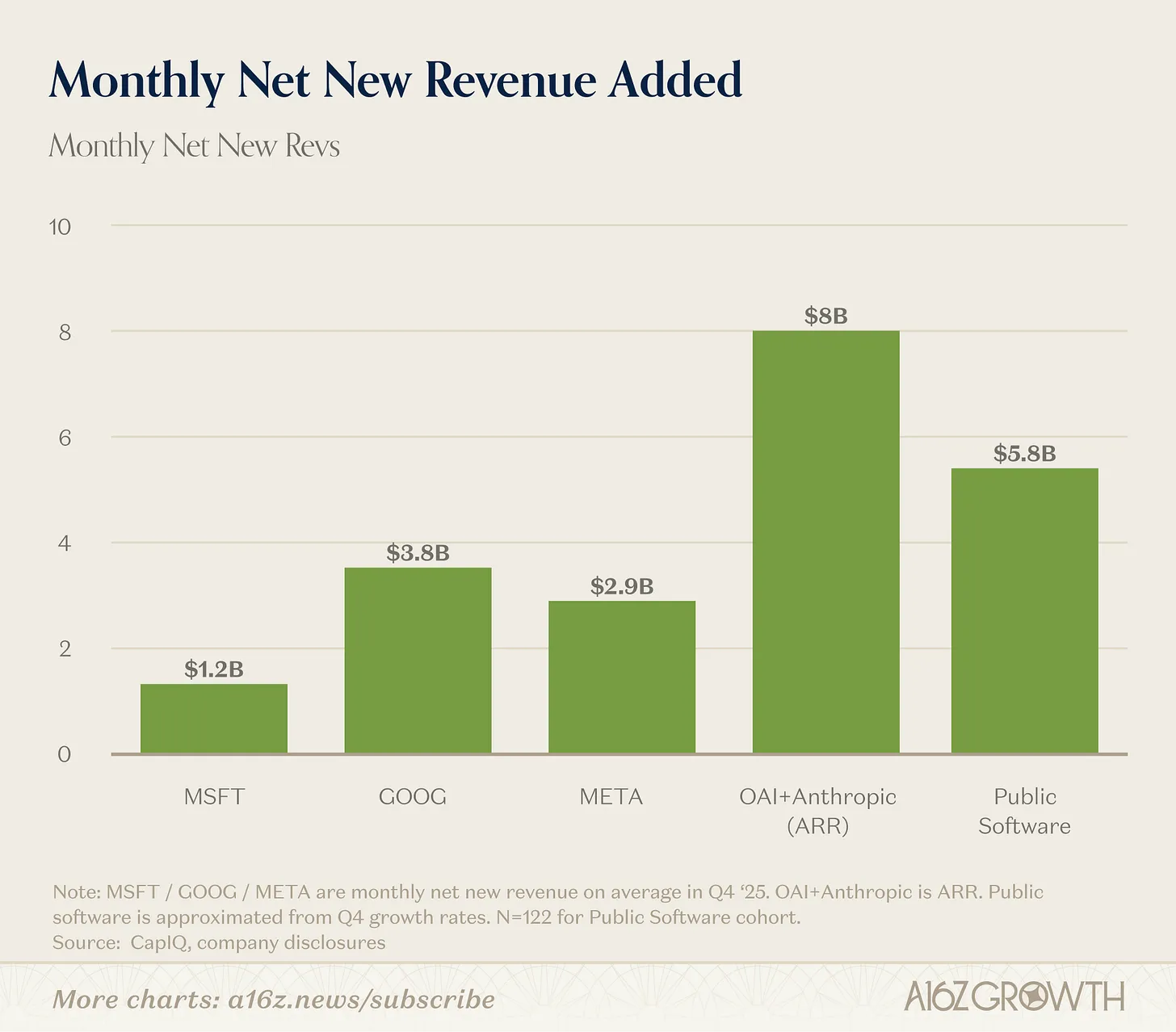

But remember, your customers' first and most obvious source of AI savings is labor efficiency, which means seats will be where they seek to cut costs. In contrast, new growth will increasingly be reflected in tokens, consumption, automation, outcomes, and machine-driven workflows.

If you are not on the token path, you are not standing where the budget is growing fastest.

Not all companies are in a position to do this. You might evaluate your options and see no reliable hope of winning through Path One. But if you see it, and if you survive this twelve-month sprint, you will emerge as a focused and accelerating company with a new leadership team and a "refounding moment" from which your team will draw unity and new energy for years to come.

Path Two: Restructure for 40%+ Real Profitability

Over the past decade, software companies have become very good at talking about free cash flow margins. But if we are serious about this, we should stop excluding equity incentives and pretending that equity dilution is not an expense borne by shareholders. For companies not planning to re-accelerate growth, I believe the right goal is to achieve real operating profit margins of 40% or even 50%+ (including SBC) within 12 to 24 months.

Achieving profitability of over 40% requires more than 10% or 20% layoffs. It means flattening management layers, standardizing implementation, minimizing custom services, eliminating committees, raising prices where you have workflow or switching cost advantages, moving long-tail customers to a higher floor price or letting them churn, and treating every share issued as a transfer from owners to employees.

AI should change the shape of the company. The cost structure should change accordingly.

This will require a similar level of effort as the first path. Even if your goal is different, you still need to aim to build an AI-native company in 12 months, maximizing engineer productivity and efficiency. From day one, you need to figure out what a smaller, but more motivated and productive workforce will look like in your organization twelve months from now.

Counterintuitively, the first thing you need to do is significantly increase the token spending budget allocated to each engineer. If your engineers aren't spending real money on tokens, they probably aren't pushing hard enough. A thousand dollars per engineer per month is not excessive; it's almost a basic requirement.

A useful working premise is that the upper limit of individual engineer output is increasing far faster than most company structures can utilize. Some of the best operators have described top engineers seeing order-of-magnitude productivity gains and managing 20 to 30 Agents simultaneously. Whether 20x is an extreme case or just the frontier, the organizational impact is the same: companies built for ten-person committees will lose on speed to companies built for four-person squads.

Meanwhile, you need to prepare for large-scale layoffs—you already know this.

You can't just prune the leaves at the edges of the company: if you cut a large portion of individual contributors but keep the director and VP teams, you will be worse off than when you started. To be clear, this is different from Path One; you are not trying to build a "new" business. But you are still "refounding" the company around a new set of values focused on performance and a shareholder mindset, so make sure you embark on this journey with the right leadership team.

Another very important thing is that teams should be honest about which old moats are being eroded.

Just having data is often not enough.

Integrations are becoming easier to replicate.

Workflow and UI advantages become less important as Agents move more easily across systems. Migration is becoming easier.

Competitors will increasingly attack each other's core modules, not just the edges. This means price pressure on the core business is coming, so prioritize the advantages that help you maintain pricing power and customer retention.

It Can Be Done: Lessons from Broadcom

Even before AI, the public market had a case study of a strong approach: Avago/Broadcom under Hock Tan (*Note: In 2013, Avago acquired LSI Corporation for $6.6 billion, further entering the enterprise storage market. In 2016, Avago acquired Broadcom and changed its name to Broadcom Inc.). It's a harsh model. It's not every founder's cultural blueprint. But it reminds us that radical cost control, product simplification, and price realization are possible. The strong approach exists.

The second path may sound pessimistic, but not every software company has the right to choose the first path. If the company does not have that right, then the second path is the only way to create value.

Key Questions

Founders should write one question on the first page of every board presentation: Which path are we on?

Is it over 10 percentage points of revenue growth through new AI products? Or is it 40%+ real operating profitability including SBC?

Investors should ask the same question more forcefully than they do now.

Where is the AI product engine that can change the curve? Where is the R&D architecture restructuring around small, token-rich, customer-close teams? Where is the plan for building human/Agent dual interaction layers? Where is the clear roadmap to 40-50%+ real profitability? Where is the plan to reduce equity dilution as a percentage of revenue?

If the answer is some version of "a bit of both" or "we are evaluating options," I expect the market will continue to apply pressure.

Founders: You need to choose a path, and you need to decide quickly who on your team you want to go with. You have the opportunity to create a new startup moment for your company, your new team, and your investors. Either grow 10% or earn 40%. Either build the next generation of products or build a cash cow. There is no middle road. Good luck.

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Discussion Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush