Authored by: Matt Hougan, Chief Investment Officer, Bitwise

Compiled by: Chopper, Foresight News

Over the past two weeks, three cryptocurrency research firms I have long followed—other than Bitwise—have published in-depth reports addressing the same issue: Has the cryptocurrency market reached its bottom?

- Galaxy Digital: Bitcoin has not bottomed yet; data points to a potential bottoming zone.

- NYDIG: What factors are currently suppressing Bitcoin's price performance?

- Standard Chartered: The market bottom has already occurred.

The three reports are detailed, containing a wealth of data and complete logical reasoning, and are worth reading in full. However, if you're looking for a simple, unified answer, you might be disappointed: the judgments given by these three authoritative institutions are completely different.

Has the Market Bottomed?

- Galaxy Digital: No

- NYDIG: Possibly, but not very likely

- Standard Chartered: Yes

Below, we break down the core logic of each institution one by one.

Three Institutions, Three Views

Galaxy Digital

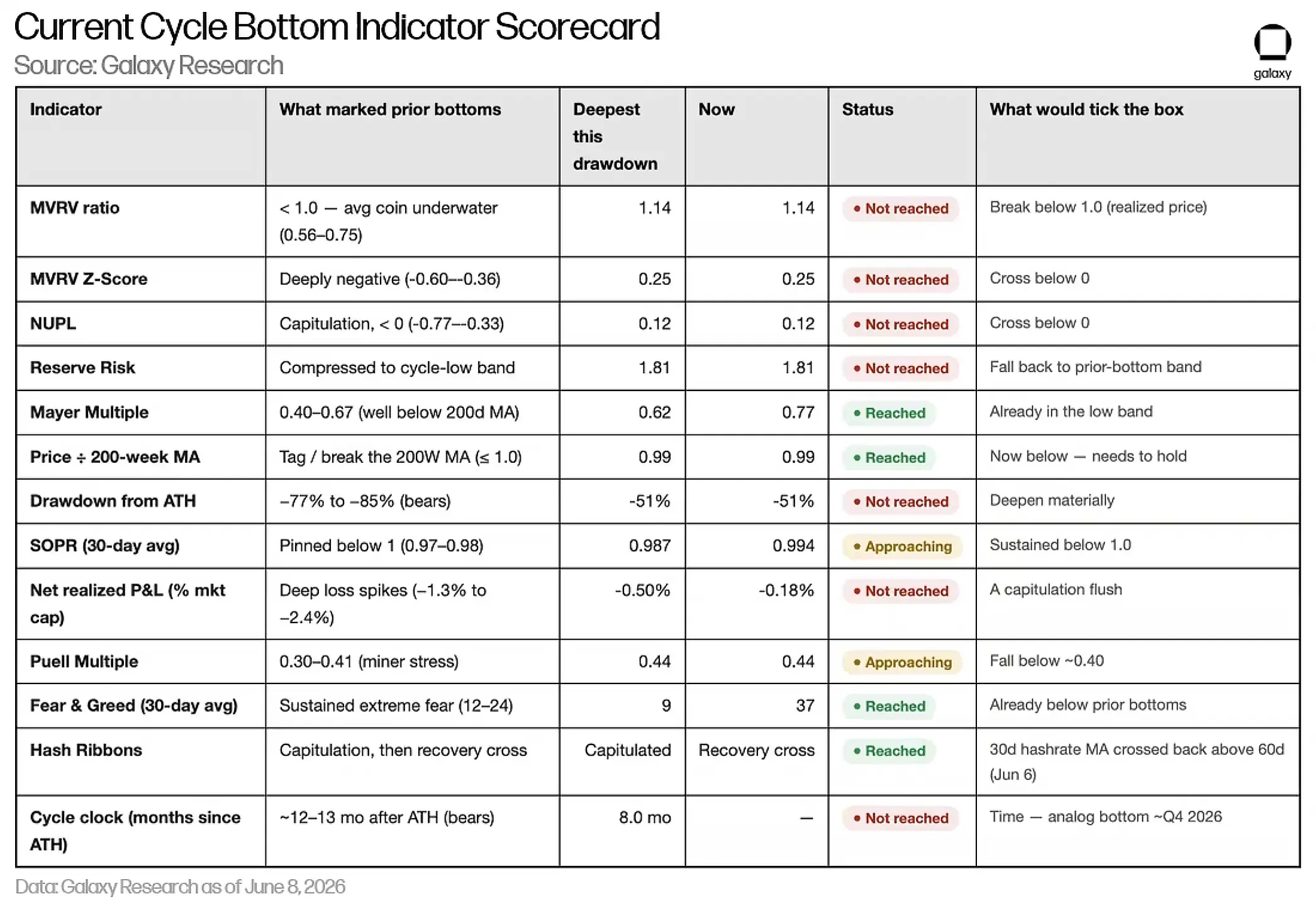

Galaxy Digital reviewed Bitcoin's full 17-year price history and summarized 13 indicators that typically appear simultaneously when the market truly bottoms out. These cover six dimensions: valuation, profit-taking, miner pressure, price trends, bull/bear cycles, and market sentiment. Long-term Bitcoin investors are familiar with these indicators, including the 200-week moving average, Fear & Greed Index, Mayer Multiple, etc.

Galaxy found that currently only 4 indicators fully meet the criteria, 2 are partially met, and the remaining 7 have not triggered a bottom signal. The report concludes that the bottom range for this Bitcoin cycle is between $30,000 and $54,000, with a neutral baseline bottom of $40,000 to $46,000.

NYDIG

NYDIG also adopts a multi-indicator comprehensive analysis framework, comparing the current market with historical cycles, assessing the market status from dimensions such as the duration of maximum drawdown and holder profit/loss (what Bitcoin users call 'MVRV,' or the market value to realized value ratio).

NYDIG believes that current indicators are very close to the extreme ranges of historical major bottoms, but the hallmark widespread panic selling seen in past major bear markets has not yet occurred. However, the report introduces a variable: the entry of institutional funds has fundamentally changed Bitcoin's cycle logic. The magnitude of this correction might be smaller than in historical bear markets. From this perspective, the bottom might also have already appeared.

Standard Chartered

Standard Chartered is not unwaveringly bullish on Bitcoin. Back in February when Bitcoin was at $67,000, the bank lowered its full-year price forecast, warning that the price could fall to $50,000, citing a weaker macroeconomic environment and sustained selling pressure from Bitcoin ETFs.

But last Friday, Standard Chartered updated its view, identifying $59,000 as the bottom of this cycle. The two main logics supporting this view are: a potential diplomatic agreement between the US and Iran, and the highly anticipated upcoming SpaceX IPO. Standard Chartered believes that the substantial selling by ETF holders was to raise funds for participating in the SpaceX listing, and this selling pressure will gradually subside. Standard Chartered's latest forecast is that Bitcoin will challenge $100,000 within the year.

Consensus Far Outweighs Differences in the Three Reports

You might wonder, what useful information can be extracted from three reports with seemingly opposing views? In fact, the underlying consensus in these three reports far outweighs the surface differences. For long-term investors, the conclusions they agree on are far more valuable than their disagreements:

- All three judge that the market bottom for this cycle will occur within this year.

- All three believe the current price is closer to the bottom than to the previous high.

- All three unanimously remain bullish, expecting Bitcoin to usher in a new bull market in the future.

At the time of writing this article, Bitcoin is trading around $67,000. One report claims the bottom at $59,000 has already occurred, one sees a potential drop to $50,000, and another a neutral baseline bottom of $43,000. But the core conclusion is highly unified: a bottom will definitely be reached within the year.

This is the key point long-term investors should focus on. Whether the bottom is at $40,000, $50,000, or $60,000, the difference is actually limited. What truly matters is whether Bitcoin can subsequently surge to $100,000, $200,000, or even $1 million. As long as it reaches those levels, entering and holding long-term at the current price offers considerable upside potential.

A rather ironic phenomenon in the current market is that everyone is obsessing over whether the market has bottomed, while overlooking a more important question—has the top already appeared? In my view, as long as the peak has not arrived, Bitcoin retains its long-term allocation value.

The core logic supporting Bitcoin's long-term value has not only persisted but continues to strengthen: government debt continues to accumulate worldwide with no effective resolution in sight; inflation constantly erodes the real purchasing power of wealth; public trust in centralized institutions like governments and banks continues to decline; the global digitalization process keeps accelerating; Bitcoin's trading and investment channels are constantly improving; and the early crypto-native demographic is aging, with their assets and industry influence growing simultaneously.

Of course, potential risks remain in the market, including threats from quantum computing and tightening global regulation. However, on balance, the current situation looks better than in any previous crypto winter.