Written by: David Christopher

Compiled by: Saoirse, Foresight News

BlackRock's iShares Staking Ethereum Trust ETF (ETHB) officially began trading on the Nasdaq exchange on March 12th. This is BlackRock's first Ethereum staking fund, and it quietly addresses the core issue that has been hanging over the narrative of Ethereum's institutional development since the launch of the spot Ethereum ETF.

This means that Wall Street can, for the first time, access Ethereum in its proclaimed true form — viewing it as a productive asset capable of generating stable yields.

Core Product Launch: Filling the Institutional Investment Gap

The highly anticipated staking Ethereum ETF is officially launched. This fund deeply integrates spot Ethereum exposure with staking rewards, providing institutional investors with an unprecedented compliant channel.

Since its inception, the spot Ethereum ETF has suffered from a fatal product mismatch.

For a long time, Ethereum has been promoted to institutions as a "native internet bond" — possessing scarcity (annual issuance capped at just 1.5%), yield-generating properties (annual compound yield of approximately 3%-5%), and being deeply embedded in the settlement layer of a new financial system composed of stablecoins and tokenized assets.

Even if this concept is slightly "avant-garde," it has gained market acceptance. However, the actual product delivered failed to match this vision.

After the spot ETF launched, it was uniquely missing the core element of "yield." Investors could only gain exposure to price fluctuations but were completely unable to access Ethereum's economic engine. We sold institutions on a yield-bearing asset but delivered a hollow shell without returns.

Bitcoin does not have this problem. The core of its value proposition is "store of value," a logic that is simple and direct; holding the spot asset captures its full value. But Ethereum's logic is截然不同 (completely different). Staking is an inseparable part of its asset属性 (attributes), the fundamental way for holders to benefit from the network's economy and obtain compound returns. The spot ETF could not provide this function.

This is not the only reason, but it is undoubtedly a key factor leading to the severe lag in institutional inflows for Ethereum. BlackRock's Bitcoin spot ETF (IBIT) currently has assets under management (AUM) exceeding $55 billion, while the Ethereum spot ETF (ETHA) has an AUM of only about $6.5 billion. Admittedly, Bitcoin's first-mover advantage and simpler narrative are partial reasons, but the defect of the product itself is the core issue. Institutions got the upside narrative of Ethereum but received a castrated asset.

Wall Street Has Already Entered, Infrastructure Value Recognized

Poor performance on the asset side has masked the rapid development of Ethereum's institutional adoption since the spot ETF launched in July 2024.

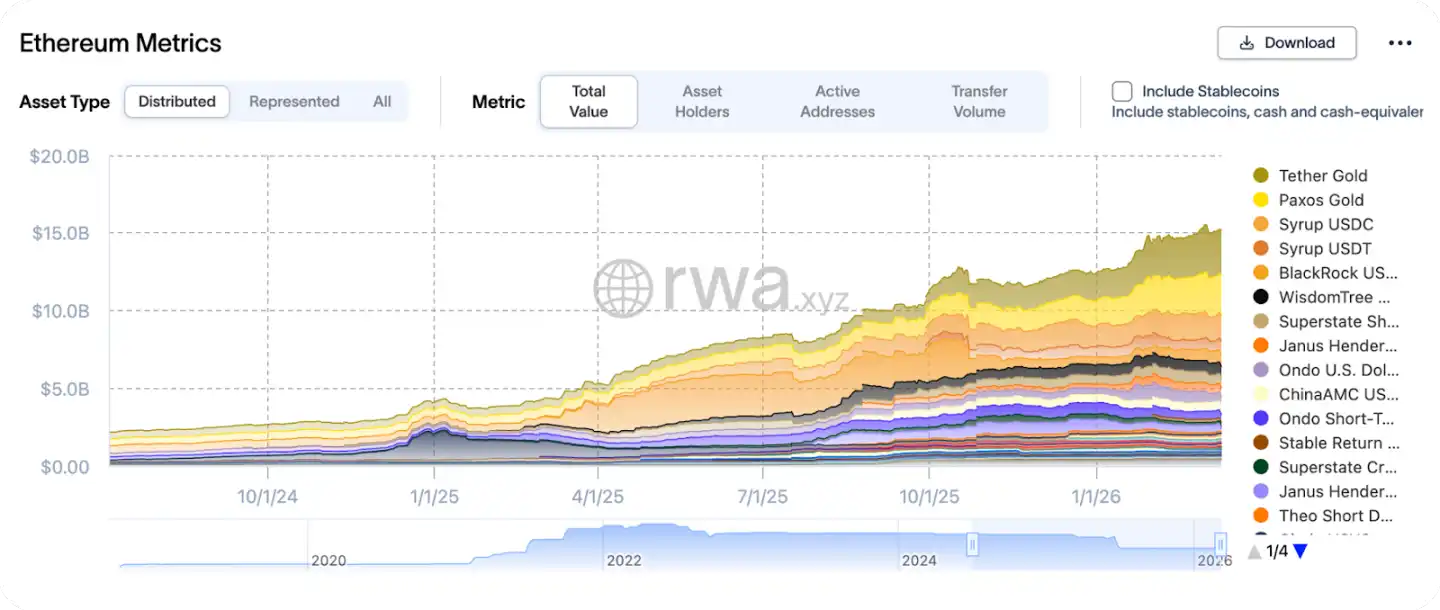

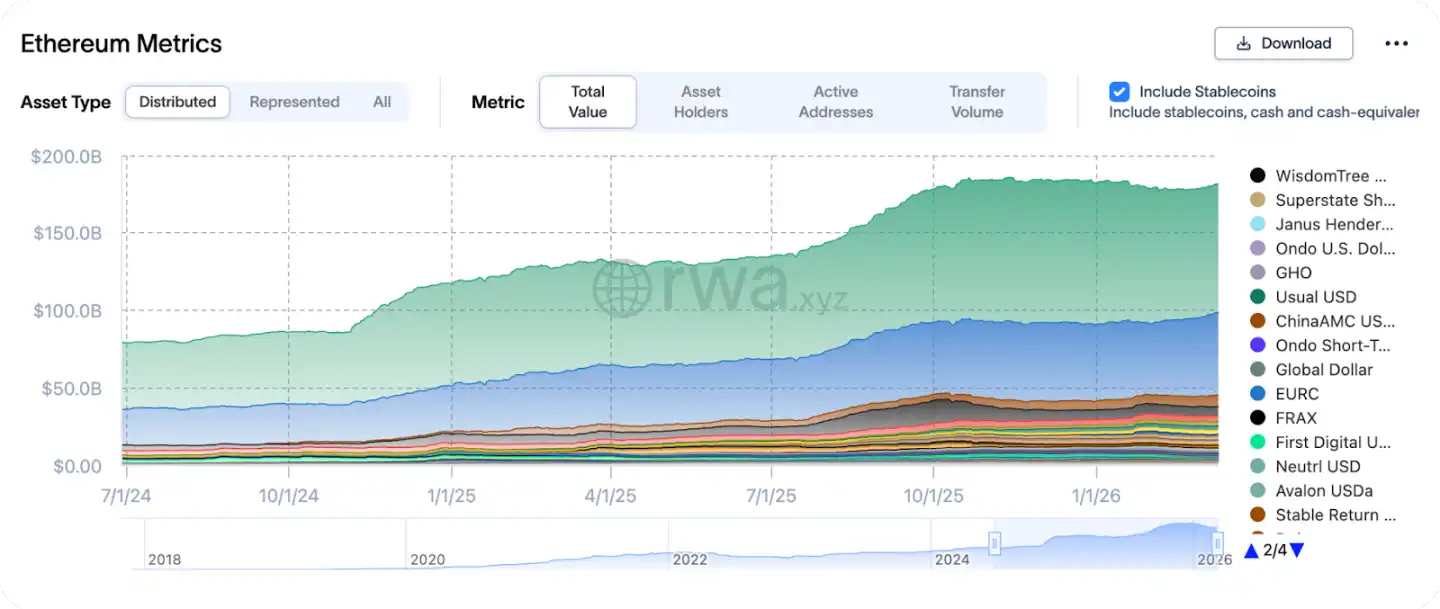

During this period, the supply of RWA (Real World Assets) on Ethereum has grown approximately 7-fold, and the stablecoin supply has doubled. Wall Street is increasingly viewing Ethereum as infrastructure — the operating轨道 (track) for stablecoins and tokenized finance, rather than just a single trading target.

Growth of RWA on Ethereum since July 2024

BlackRock's BUIDL fund, Franklin Templeton's FOBXX money market fund, and an increasing number of tokenized products are all settled on Ethereum or its Layer 2 (L2) networks. Major banks are testing on-chain settlement functions, and SWIFT is among them. Although ETF flows have been disappointing, Ethereum's institutional footprint is actually expanding continuously.

The essence of the problem is that while institutions could hold price exposure to Ethereum, they could not compliantly participate in the Ethereum network economy they increasingly rely on. The emergence of ETHB completely solves this pain point.

Growth of stablecoins on Ethereum since July 2024

Structural Impact: Reshaping Institutional Investment Logic

This impact far exceeds the ETHB product itself.

Before this, non-crypto-native institutions seeking yield-bearing Ethereum exposure could only use workaround structures like Digital Asset Trusts (DATs). These structures could participate in staking, restaking, and the DeFi ecosystem, but the fund's value was not directly linked to the underlying asset.

The existence of such structures was rooted in regulatory restrictions preventing institutions from directly participating in staking. With the landing of the staking ETF, the rationale for this intermediary path is significantly weakened. Funds that previously had to flow through intermediary channels to these workaround structures are expected to flow directly back to the native Ethereum asset itself.

Market Valuation & Fundamentals: Value in Deep Undervaluation Zone

At the time of ETHB's launch, Ethereum's current valuation is in a reasonable to deeply undervalued range based on multiple cycle indicators.

Its MVRV (Market Value to Realized Value) ratio is below 1, meaning the market is整体 (overall) at a floating loss; the percentage of supply in profit is lower than during the 2022 crash; the price in this cycle has failed to break the 2021 all-time high, remaining within the previous range, showing极佳的压缩性价比 (excellent compressed value) from a historical perspective.

Of course, the underperformance also has reasons related to Ethereum's own development. The Layer 2 (L2) roadmap prioritizes scale and user experience over Layer 1 fee capture. Blob data block technology significantly reduces the anchoring cost for Rollups (L2 scaling solutions), but also drastically reduces the scale of fee burns that once supported the deflation narrative, making its investment logic harder to model.

However, it is worth affirming that Ethereum's monetary system remains intact. Its annualized issuance is about 0.8%, basically on par with Bitcoin's inflation rate. Now, various elements are reconverging: institutional usage demand continues to accelerate, ecosystem applications like RWA, stablecoins, and tokenized funds are growing steadily on Ethereum, the staking yield channel is finally open, and the price is in a value洼地 (depression).

Future Outlook: Wall Street's Litmus Test for Value

For years, Ethereum has been selling itself to institutions as a "yield-bearing reserve asset" and the settlement layer for a tokenized economy. This story has been refined, formalized, and reiterated — placed before institutions that already recognize the network's value but were unable to participate in its economic proposition.

Now, the product design finally perfectly matches the value proposition. The market performance of ETHB will be the key litmus test for whether Wall Street truly recognizes the value of Ethereum as an asset.