Original Author: Andjela Radmilac

Original Compilation: Luffy, Foresight News

Cathie Wood's ARK Invest accumulated $77 million worth of publicly listed crypto company stocks in June. According to ARK's daily trading disclosures, during Bitcoin's worst monthly performance in four years, the fund increased its positions by $44 million in Coinbase, $25.25 million in Circle, and $8.2 million in Bullish.

Wood and several institutions have adhered to the same investment thesis for years: publicly listed crypto companies provide investors with a compliant channel to share in the cyclical gains of the crypto industry without directly holding Bitcoin. However, CryptoSlate's analysis of market data as of July 2nd reveals the hidden significant cost of this stock investment path.

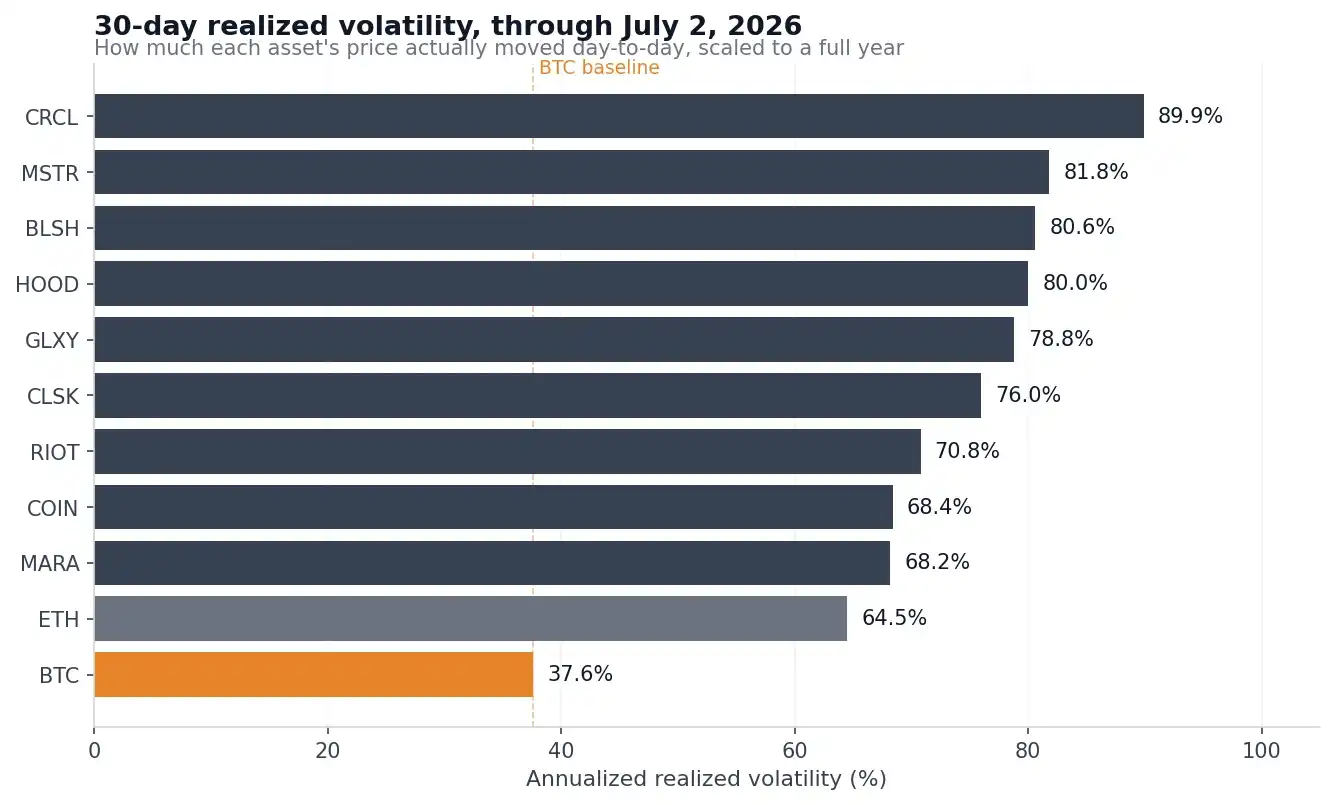

The 30-day annualized realized volatility of nine US-listed crypto companies ranges from 68% to 90%, almost double Bitcoin's 37.6% volatility. Extending to a 90-day period, Circle's volatility reaches 103.6%, while Bitcoin's is only 37.8%. The gap in price drawdowns is also significant: Circle has retreated 51.4% from its high, MSTR 48.6%, Bullish 43.6%; whereas Bitcoin has declined 36.4% from its near $97,000 high in January, with all drawdowns smaller than those of the aforementioned stocks.

30-day annualized realized volatility of BTC, ETH, and nine US-listed crypto company stocks from January 1, 2026, to July 2, 2026

Judging by volatility alone, crypto stocks appear to be leveraged Bitcoin. However, correlation data reveals a completely different truth. Over the past 90 trading days, the correlation coefficients between Circle, Robinhood, Bullish, and Bitcoin were only 0.55–0.58 (correlation range is 0 to 1, where 1 represents perfectly synchronized movements, and 0 represents no association). This means Bitcoin's price movements explain only about one-third of the stock volatility of these crypto companies. The remaining volatility stems entirely from company-specific risks: quarterly earnings reports, industry competition, financing activities, equity dilution from share issuance, etc. Investors aiming to gain crypto industry exposure via stocks ended up with only partial Bitcoin price exposure while additionally bearing a whole set of operational risks unique to the stock market.

Only One Stock Truly Tracks Bitcoin

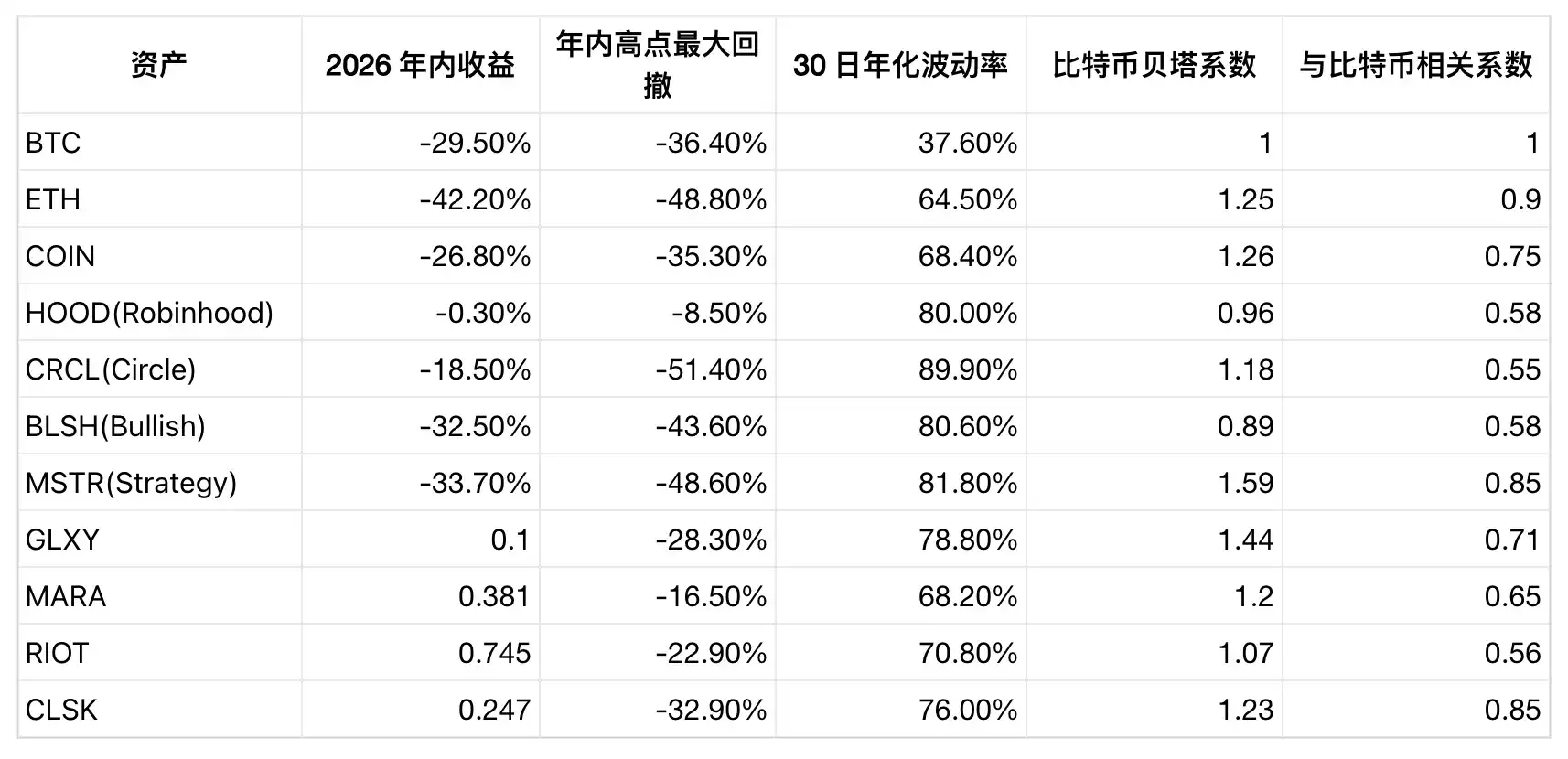

The table below summarizes the correlation of crypto company stocks with Bitcoin from late 2025 to the present. The Beta coefficient represents the percentage change in the individual stock for every 1% movement in Bitcoin.

Only MSTR in the entire market qualifies as a Bitcoin alternative. With a Beta of 1.59 and a correlation of 0.85, it is essentially an equity instrument for holding leveraged Bitcoin. In the current downturn, its year-to-date decline and drawdown from highs far exceed Bitcoin's.

Coinbase is a relatively balanced choice, with a year-to-date decline of -26.8%, slightly less than BTC's. Its Beta coefficient is 1.26 and correlation is 0.75, making it the second strongest correlated with Bitcoin within the sector. However, its volatility is still nearly double that of Bitcoin. The stock is down 60.6% from its historical high of $419.78 in July 2025, meaning losses for investors who bought at that peak are much greater than for those who entered at Bitcoin's historical high in October 2025.

Circle perfectly illustrates "company-specific risks beneath a crypto facade." It has the lowest correlation with Bitcoin in the sector and the highest 90-day volatility. The trigger occurred on June 30th: the Open USD stablecoin, backed by over 140 companies including Coinbase, Stripe, Visa, Mastercard, and BlackRock, officially launched. CRCL plummeted 17.5% that day. This sharp drop was almost entirely unrelated to Bitcoin's performance, purely a company-specific negative stemming from competition for market share in the stablecoin race.

Robinhood serves as a counter-example, similarly confirming that individual stock performance operates independently of crypto trends. The stock has declined only 0.3% year-to-date, with a maximum intra-year drawdown of just 8.5%. Crypto is only a small part of its overall brokerage business encompassing stocks, options, and derivatives; diversified operations cushion the downturn. Conversely, during crypto bull markets, it is unlikely to provide investors with substantial gains from crypto price appreciation.

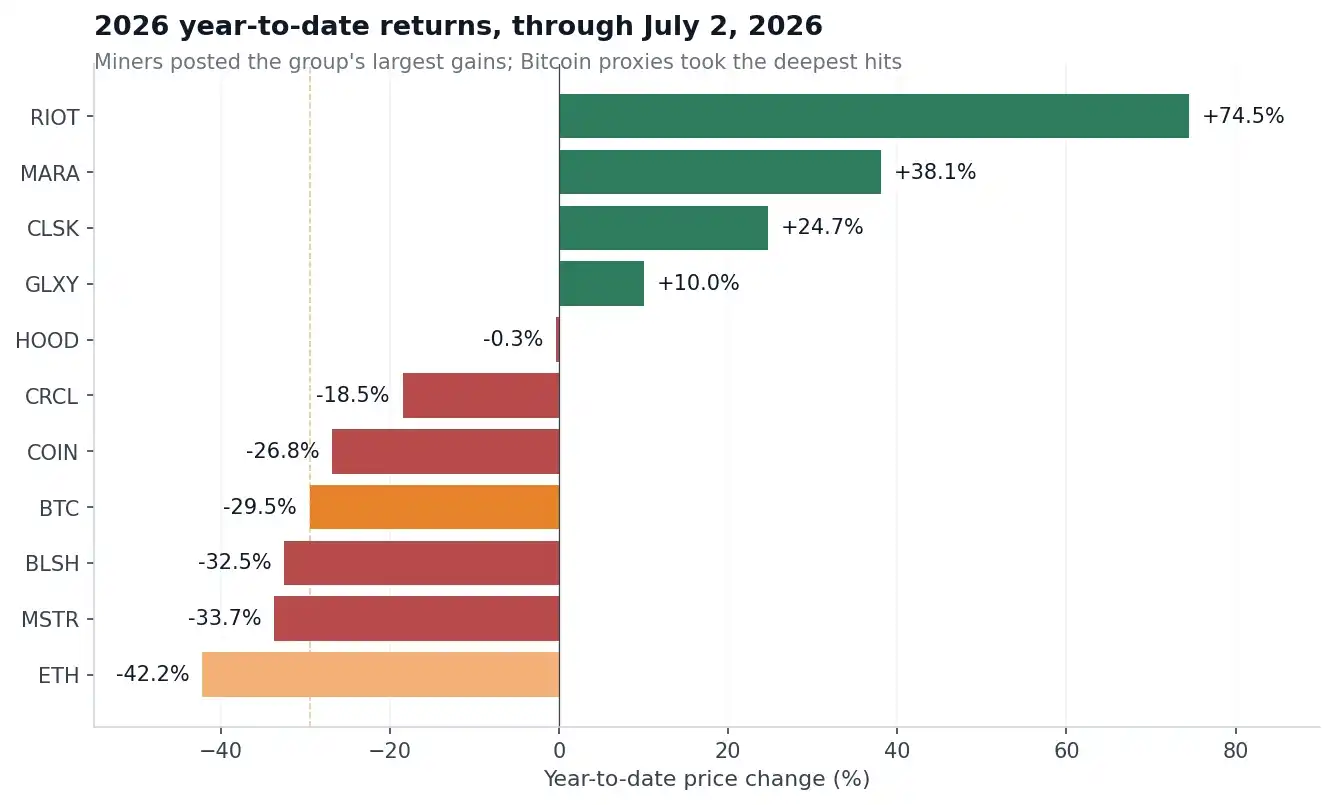

Mining company movements are most anomalous. While Bitcoin fell 29.5% year-to-date, RIOT surged 74.5%, MARA rose 38.1%, and CleanSpark gained 24.7%. The core logic is their pivot to becoming AI high-performance computing service providers, securing tens of billions in computing power leasing contracts while consistently reducing their Bitcoin holdings. Although their daily movements still follow Bitcoin (Beta coefficients all greater than 1), their full-year returns are entirely driven by AI hosting services, decoupled from coin prices.

Year-to-date price changes of BTC, ETH, and nine US-listed cryptocurrency stocks

Bitcoin itself is not low in volatility. Volmex's Bitcoin 30-day Volatility Index dropped to a low of 24.5 in late May, peaked at 68.7 in early February, and rebounded to 41.6 in early July. Despite this, the volatility of most crypto stocks remains approximately double.

Strategy Case: Equity Structure Brings Additional Risks

Holding Bitcoin only entails the risk of price fluctuations; buying publicly listed crypto company stocks adds layers of corporate operational risks, equity dilution, disappearance of valuation premiums, financing pressures, changes in capital structure, and other variables.

Strategy recently exposed all these vulnerabilities within a single month. In late June, its price-to-net-asset-value (mNAV) ratio fell below 1 for the first time. This metric measures the company's total valuation against its net assets. A ratio below 1 means the market values the entire company less than the cash and Bitcoin it holds. According to disclosures as of June 22nd, Strategy held 847,363 Bitcoin. On the day mNAV fell below 1, this Bitcoin was worth approximately $50 billion.

An mNAV greater than 1 is the foundation of Strategy's entire growth flywheel. Previously, the company could issue common and preferred shares at a premium, use the raised funds to acquire more Bitcoin, thereby increasing Bitcoin holdings per share. Once mNAV falls below 1, this cycle can erode shareholder value in reverse—issuing new shares to raise funds for buying Bitcoin equates to selling existing Bitcoin assets at a discount.

CryptoSlate reported as early as January that Bitcoin-holding companies are divided into valuation premium and discount types. By late June, Strategy's total market cap was $29.54 billion, less than half of its peak exceeding $71 billion in 2024, with all four classes of preferred stock at historical lows.

Strategy announced a response plan. On June 29th, it revealed a stock repurchase program of up to $1.25 billion while authorizing Bitcoin sales to supplement liquidity, covering preferred stock dividends and debt interest. In the preceding weeks, on June 1st, the company conducted its first Bitcoin sale since 2022, selling only 32 Bitcoin. Following the news, the stock surged 12.6% in a single day, ending an eight-day losing streak. The world's largest Bitcoin-holding company needing to sell its holdings in a bear market to secure cash flow is a constraint not encountered when directly holding Bitcoin and a risk unique to stocks.

This is precisely the backdrop against which ARK increased its positions against the trend. On June 25th, as crypto stocks collectively plummeted, Wood's funds bought $3.27 million worth of Robinhood in a single day, simultaneously adding to positions in Coinbase, Circle, and Bullish. Wood believes Bitcoin's long-term target price is in the millions of dollars and is currently positioning at a significant discount in crypto companies that have deeply corrected from their 2025 highs.

The data reveals the true nature of these companies.

- Strategy = Leveraged Bitcoin + Equity Dilution Risk;

- Circle = Payment company in the stablecoin track, deeply embroiled in market share battles;

- Robinhood = Comprehensive brokerage firm, crypto is just a side business.

Wood's bulk purchase of these company stocks is essentially a bet on a combination of different business models, with vastly differing levels of crypto exposure among them.

Each individual stock has its own independent investment thesis. Coinbase has outperformed Bitcoin year-to-date, Robinhood has maintained its January price level, and the mining sector overall has led in returns. But the core question remains: Are crypto stocks really less risky than holding coins directly?

Data from nine listed companies shows that stocks either amplify Bitcoin's volatility or layer on company-specific operational risks unrelated to coin prices.

This year's truly strong-performing crypto stocks rely on independent growth drivers like AI computing power, brokerage user traffic, and payment products, with Bitcoin being only a secondary influencing factor.