1、BTC有望加速回升

日K线图显示,BTC价格微幅调整以后,反弹走势即将再次开启。随着成交量继续维持高位运行,BTC价格在2万美元的支撑变动异常有效。 压力位方面,22500美元、25000美元都是BTC需要确认的突破点位。

2、BTC抛压下降

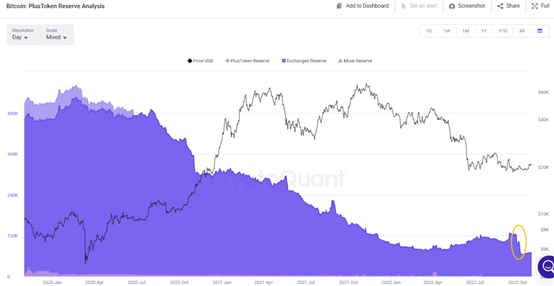

BTC维持强势基础,是抛售压力相应降低以及多头实力持续增长。从抛压减少的迹象来看,Plustoken账户的混币和出售在近期已经显著增加,使得相应的被盗BTC数量大幅度减少。从124649枚BTC下降到了63434枚BTC,减少的BTC数量达到了5万枚BTC以上。因此,对应的BTC的交易抛压相应的降低以后,推动了BTC价格筑底回升。值得关注的是,近期Plustoken账户的交易用BTC数量大幅度下降,并且存量BTC下降到历史低位,提升价格上涨压力降低,关注上涨预期。

3、ETH准备拉升

日K线图显示,ETH价格以及处在二次回升的姿态,价格随时可能出现拉升表现。目前ETH短线回撤空间有限,价格仅在2个交易日中回撤4%,就已经开始出现止跌迹象。从ETH目前的运行区间判断,短线上涨的重要压力位在1910美元。斐波那契61.8%对应的1910美元的抛压已经在8月13日ETH开始回撤得到体现。因此,等待ETH价格涨幅得到20%以上再关注重要的抛压变化。

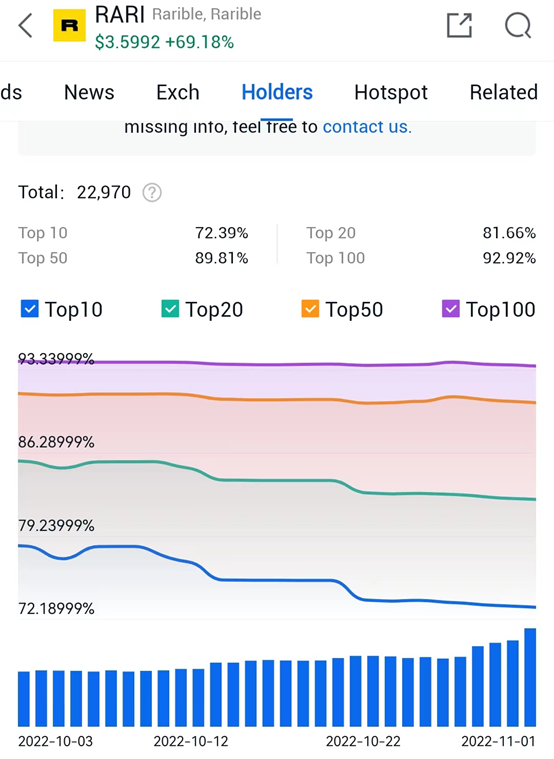

4、RARI主力减仓趋势确认

随着RARI在低位飙升达到了70%,最大2日内振幅高达100%,RARI在涨幅上已经排名靠前。同时,关注到RARI的交易量放大空间较多,同时又是再次脉冲放量,不排除RARI短线大涨以后出现交易量不足的情况。实际上,30分钟K线已经提升了抛压增长信号,关注价格回调表现。

5、RARI主力减仓

从持币数量上看,RARI的持币前10位的主力减仓 趋势明确。从10月3日的77.49%下降到了11月1日的72.19%,降幅达到了5.3个百分点。因此,对RARI价格上涨的基本判断,或许首先应该关注抛压变化,然后才是低吸机会。