1.简介

“”

“L1战争”是2020-2021年周期中被高度宣传的故事,主要的替代性第1层区块链与以太坊一起捕获了大量的价值和开发者人才。Solana、Cosmos、Avalanche、BSC和其他近十家L1区块链在市场高峰期持有的市值超过3000亿美元。虽然这种说法已经降温,而且由于熊市,人们都缩手缩脚,但围绕网络规模的可扩展性、安全性和围绕技术设计持续创新的讨论再次被提到了风口浪尖。这些对话是由两个新的L1独角兽公司Aptos和Sui的巨额融资所推动的,它们的团队和架构都来自Meta现已不存在的Diem和Novi项目。

“”

> Diem & Novi

“”

Novi Financial是Meta的全资子公司,也是Diem Association的成员,是Meta的数字资产团队为Diem构建的主要项目。这是一款加密支付钱包,使用的技术与Facebook在2019年6月宣布的其前身Calibra相同。面对持续的监管审查和缺乏对采用与web3和去中心化的主流风气相矛盾的产品的热情,Diem Association开始逐步退出,Novi试点也面临了类似的命运。

“”

虽然Meta支持的项目在1 Hacker Way淘汰,但该技术背后的团队有很大的野心,希望以完全不同的方式将其带回。最值得注意的是,Diem的目标是成为一个许可网络,而Aptos和Sui是去中心化的、无许可的,允许任何人作为验证者加入他们。

“”

Diem最初被称为Libra,是Facebook (Meta)提出的一个基于区块链的稳定币支付系统,由Diem Association独立和加密的方式委托给Diem Association,该协会由支付、技术、电信到风险投资和非营利组织组成,包括了Visa、Mastercard、eBay、Shopify、Anchorage、Coinbase、Ribbit capital、a16z、Union Square Ventures、Mercy Corp、Uber、Lyft和许多其他公司。

“”

>Move

“”

Move是一种基于Rust的开源编程语言,由Diem Association团队开发,用于创建可定制的交易逻辑和智能合约。它是一种新颖的语言,与项目中推出的MoveVM一起使用。该机制旨在最大限度地提高安全性,而不增加交易的编译成本,与其他PoS链(如以太坊)相比,很大限度地减少了gas费用。它被吹捧为一种安全和高效的语言,可以帮助开发人员避免可能导致漏洞的错误。

“”

根据白皮书,Move的可执行格式是“比汇编语言级别高,但比源语言级别低的字节码。字节码验证器在链上检查字节码的资源、类型和内存安全,然后由字节码解释器直接执行。”将Move与其他编程语言区别开来并使Move享有高水平安全性和表达性的主要因素是它对资源的使用,这是从线性逻辑的数学思想中提取出来的。

“”

虽然两个协议都利用了Move编程语言,但Aptos和Sui采用的模式略有不同。Aptos利用Diem团队创建的原始MOVE语言,而Sui则利用他们自己的替代版本“Sui MOVE”。

“”

2.融资概述

“”

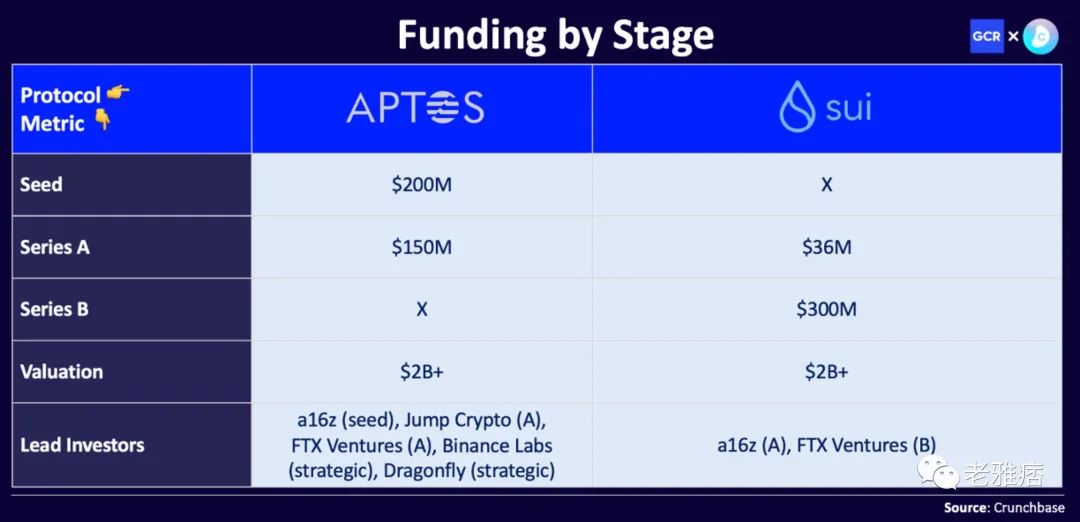

在几轮令人瞠目的融资后,Aptos和Sui的知名度迅速上升。Aptos Labs在2022年3月获得了a16z领投的2亿美元战略投资,随后在7月获得了FTX Ventures领投的1.5亿美元a轮投资,夹在2021年12月Mysten Labs的3600万美元a轮投资和最近9月同样由FTX Ventures牵头的3亿美元B轮融资之间。Binance Labs和Dragonfly也加入了这一行列,在Mysten宣布最新一轮融资后,它们都在9月底对Aptos进行了战略投资。

“”

构建新的L1是一项浩大的工程。它是资本密集、人才密集的,需要数年的时间来建设、扩展、营销并逐步走向去中心化。最近的几轮融资就像是一场资本军备竞赛,看谁能建立起最大的熊市战仓,在下一个扩张周期产生有意义的创新。尽管如此,社区和投资者也发出了一些响亮的批评,认为在深度熊市中,由于缺乏活跃的生态系统、治理框架或用户来支持其两倍独角兽的地位,这样的估值太高了。

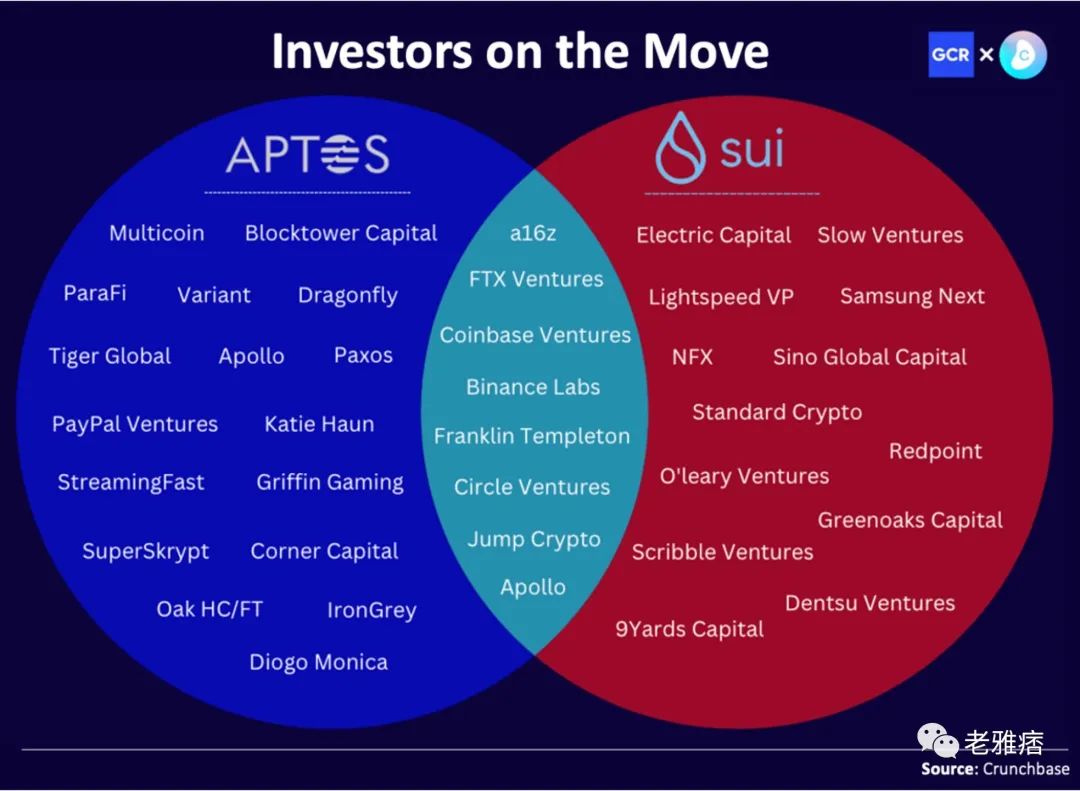

最近的融资活动讲述了另一个有趣的故事。交易所资金纷纷涌入这两个项目,FTX、Coinbase和币安都为这两个协议的最近几轮融资提供了资金。他们的母公司交易所将上市这些代币,并从交易者轮流进入另一个L1叙事中获得大量费用,同时也以早期折扣获得代币分配。除了交易所基金,值得注意的是支持这些协议的基金的水平——我们最近的VC排名中有15家顶级基金填补了cap表。Solana的一些投资者也发现,他们也在为这些同样希望最大化网络容量的协议提供资金,其中包括Multicoin、Blocktower、Sino、ParaFi、a16z和Jump。尽管人们仍对过高的估值持怀疑态度,但早期投资者希望通过未来的代币认股权证获得超额回报。

3.创始人-市场契合度

“”

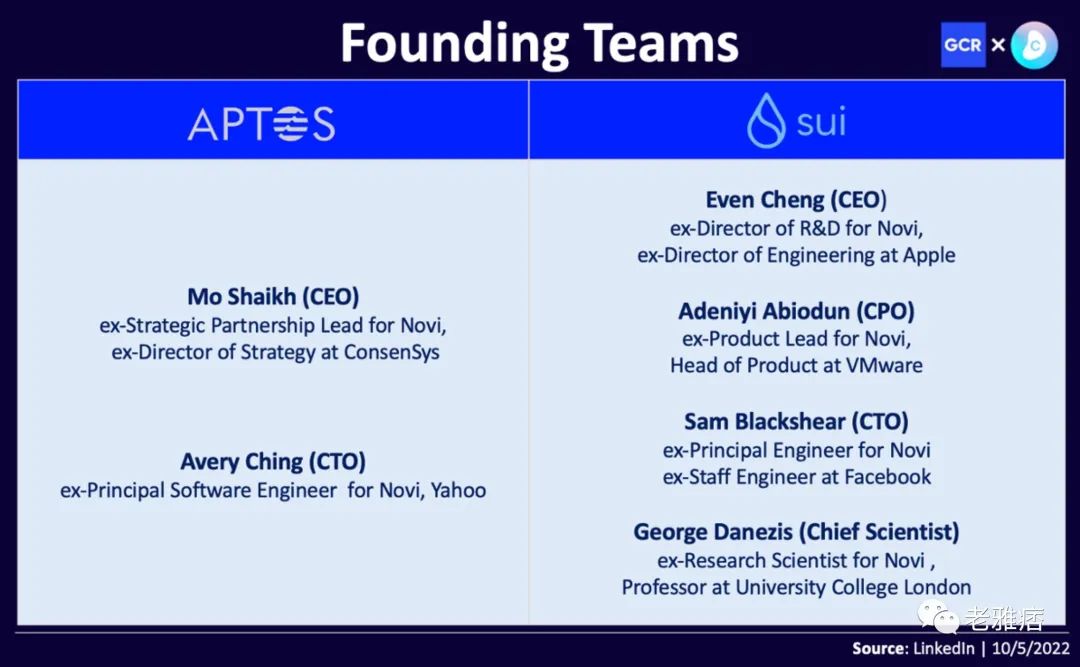

Aptos和Sui的创始团队都深深扎根于Diem和Novi项目。不可否认的是,这两个项目都具有技术智慧,可以执行这些已经积累了超过40亿美元估值的愿景。毫无疑问,这两支团队都有很强的创始人-市场契合度。Mysten Labs团队包括MOVE编程语言白皮书的两位共同作者,以及来自Novi/Diem团队的更多研发力量。作为Aptos Labs的首席执行官,Mo Shaikh带来了业务发展和合作伙伴关系——对于任何希望在不断增长的L1市场中获得牵引力的新协议来说,这是一个重要的方面。这一重点是Solana和Polygon在上个周期与NEAR和Algorand等技术性较强的协议的明显区别。Aptos还引入了包括Solana前营销主管的几位Solana校友,他们拥有扩展替代L1的第一手经验,以推动Aptos的生态系统。

4.架构与共识

“”

Aptos和Sui都是基于PoS 的区块链,两种协议都利用了一种称为BFT的共识机制,其运作理念是三分之一的验证者可以离线或有恶意,而网络仍然可以正常运行。从这里开始,两种设计开始出现分歧。

“”

> HotStuff

“”

Aptos依赖于改良的BFT共识HotStuff。在HotStuff中,每一轮投票都会发生变化的领导者会建议一个新的区块,验证者对其进行投票。由于所有验证者都与单个leader通信,所以发出的信息总数要比验证者彼此的通信低得多。一旦区块被认为是有效的,它将在Aptos声称的不到1秒内达到最终结果。这是Aptos相对于其竞争对手Solana的关键优势,后者的最终确定可能需要2-6秒。

“”

与包括以太坊在内的大多数L1类似,Aptos利用基于账户的模式,将交易依次打包成区块并形成区块链。然而,通过设计Block-STM(内存中并行执行的引擎),Aptos声称“通过利用预先设置的交易顺序,并将软件交易内存技术与新颖的协作调度相结合”,它每秒能够执行超过16万个非琐碎的移动交易。

“”

> Narwhal & Tusk

“”

Sui利用Narwhal & Tusk共识算法在执行层进行并行化。Narwhal是mempool模块——它确保交易数据是可用的。它也可以单独(不需要Tusk)与其他共识引擎一起使用,如HotStuff或Cosmos的Ignite。Tusk是一个共识模块,对提交的复杂交易进行排序以达成共识

“”

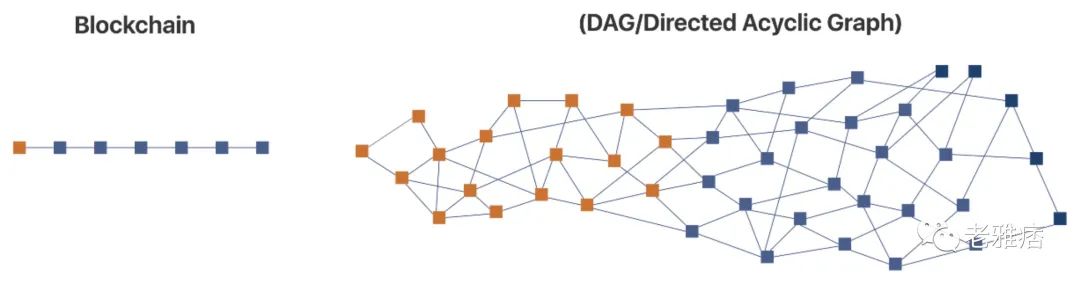

鉴于这种基于DAG或以对象为中心的数据模型,有些人可能会认为Sui是分布式账本,而不是区块链。在这种设计下,交易不会被按顺序打包到区块链中相反,它的许多元素被连接在一起,成为一个网络图而不是一个链。可以想象,DAG模型可以通过拆分对象和利用其内置属性来增强可扩展性。这种设计也是异步的,这意味着它可以抵御DoS攻击,并帮助Sui作为一个以安全为中心的协议走向市场。

通过这种设计,Sui采用了一种动态的新方法,完全消除了许多交易的共识——其所有者将简单的代币转移到不同的地址,而不依赖于他们的任何其他交易,几乎可以立即得到确认。发送者广播交易,收集验证者的投票,并收到所谓的有效性证书。对于与智能合约交互等涉及“共享对象”的更复杂的交易,Sui利用了上面概述的更传统的BFT共识。这种方法可以使Sui成为特定用例的理想L1,在这些用例中,dApp会产生大量的简单交易,并需要它们以低延迟的方式得到确认,且不太关心去中心化——例如游戏或空投。

“”

>可扩展性

“”

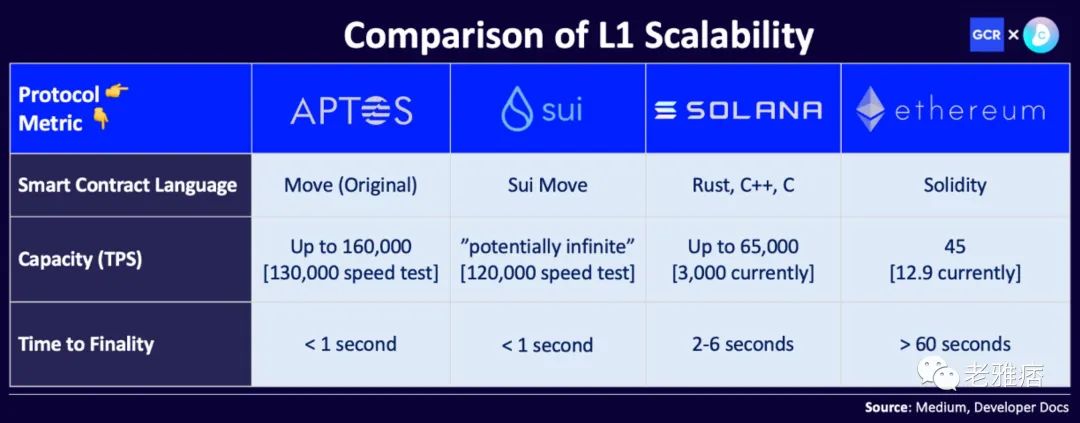

在深入研究了这些新颖的协议设计之后,很明显,可扩展性是这些项目希望为生态系统增加的主要价值。随着围绕区块链中网络规模可扩展性所进行的主要讨论,Aptos和Sui都旨在通过最大化网络容量成为这场竞赛的领导者。下面的图表强调了早期速度测试与既定的L1竞争的匹配情况。时间将证明这些团队是否能够兑现他们早期的承诺。

5.牵引力

“”

现在判断Aptos和Sui的MOVE大战将如何发展还为时过早。然而,大量的资本流入无疑为两种协议带来了巨大的吸引力,生态系统的早期迹象已经开始显现。根据Move Market Cap,已经有181个项目正在构建或支持Move编程语言的集成。

“”

> Aptos生态系统

“”

自夏末的融资以来,Aptos已经在测试网上推出了一些特定的浏览器钱包,其中包括Pontem Wallet、Fewcha、Martian以及其他一些在Chrome和iOS上可用的钱包。上述钱包背后的Aptos产品工作室Pontem Network还推出了LiquidSwap,这是Aptos上的首款AMM。此外,一些NFT市场已经在网络上建立,其中包括BlueMove、Topaz和Souffl3(目前只支持Martian Wallet),它们都在测试网beta版本中发布。Aptos Naming Service也是由Aptos基金会建立的。除了早期的DeFi生态系统,还有一些额外的dapp吸引了人们的注意,包括Aptin Finance(一个借贷平台)、Mover(到Aptos的EVM跨链桥)、Vial(算法流动性协议)、Mobius(非托管流动性协议)和Aptos上的第一个去中心化启动平台AptosLaunch。LayerZero Labs最近也宣布在10月17日上线的主网上与Aptos整合。

“”

>Sui生态系统

“”

在核心团队于7月推出Sui Wallet之后,Sui生态系统中已经出现了许多独立的浏览器扩展钱包。其中包括了Wave、Suiet、Hydro等。MoveEx已经成为第一个建立在Sui上的DEX,Aptos的NFT市场BlueMove也整合了Sui网络。最近与Axelar Network的合作旨在帮助Sui开发者与EVM兼容的应用建立联系。一个新生的GameFi生态系统也已经开始出现,但现在甚至还无法嗅到潜在赢家的气息。

“”

>关于代币经济学

“”

Mysten Labs宣布了SUI的代币经济学。虽然他们已经提供了关于代币机制的一般信息,但他们还没有发布按组群的正式分配明细。

“”

另一方面,Aptos采取了一种更加不透明的方法,这导致了社区中早期怀疑和失望的浪潮。在主网10月17日上线之前,他们没有向公众公开发布代币经济学或分配明细。直到主网发布的第二天,也就是APT在顶级交易所上市的前不久,代币经济学才正式被公布,这导致了一些知名玩家甚至称本周发布的APT代币是对散户投资者的掠夺,据Polychain的Olaf说这是“我见过的最糟糕的设计之一,我已经看到了很多”。这种挫折归因于Aptos基金会声称51%的代币供应将分配给“社区”,而实际上必须由基金会通过另一个不透明的过程任意分配——导致许多人认为Aptos基金会和Aptos实验室实际上拥有今天的供应的>67%——没有强大的模型来合理分配和去中心化网络。同样值得关注的是,根据apscan.io,在10亿总供应量中,有8.21亿是被质押的——这意味着未分配的代币有可能会获得质押奖励。Aptos Labs联合创始人兼首席执行官Mo Shaikh在推特上承认了这次发布的坎坷。

“”

6.最后的思考

“”

>L1博弈在上个周期后已经饱和。然而,其他许多顶级L1从之前的熊市中脱颖而出,迅速进入了接下来的扩张。不要低估这种情况再次发生的可能性,因为围绕持续创新和网络规模可扩展性的新对话已经生根发芽。

>我们将看到建立在Move编程语言上的整个生态系统和行业出现——甚至可能出现替代Aptos和Sui的L1。

>随着越来越多的构建者在可扩展性上不断创新,可能会出现更多专门基于Narwhal & Tusk共识机制构建并获得资金的项目。

>另一种基于Rust的编程语言将推动更多的开发者采用其他基于Rust的区块链,进一步蚕食Solidity在该行业的市场份额。