Многие участники криптосообщества продолжают ждать наступления альтсезона, однако рынок по-прежнему не демонстрирует признаков перехода к фазе активного роста. Инвесторы следят за макроэкономикой, динамикой биткоина и состоянием ликвидности, но заметных изменений нет.

Редакция BeInCrypto выяснила, что происходит с альткоинами и есть ли основания ожидать альтсезон.

Что такое альтсезон и как к нему подготовиться

Что не так с альткоинами

ISM против альтов

Индекс ISM Manufacturing PMI отражает состояние промышленности США. Он формируется на основе опроса более 400 компаний, которые оценивают заказы, производство, занятость, поставки и складские запасы. Показатели выше 50 указывают на рост, ниже — на спад.

Последний показатель составил 48,2, что означает продолжающееся снижение промышленной активности.

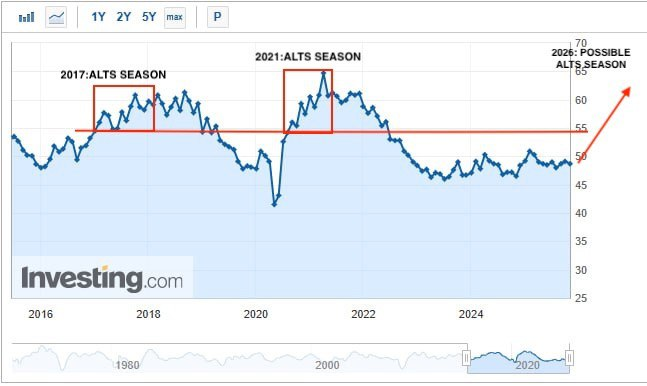

Исторически альтсезоны возникали только тогда, когда экономика находилась в фазе расширения, а ISM поднимался выше 55. Так происходило в 2017 и 2021 годах. Сейчас экономика далека от таких уровней, и это удерживает спрос на рисковые активы, включая альткоины.

Ликвидность сжимается

Сегмент альткоинов испытывает давление из-за снижающейся ликвидности. Ликвидность — это объем капитала, который может входить в активы или выходить из них без резких ценовых колебаний. Когда ликвидность уменьшается, рост становится сложнее, а импульсы быстро затухают.

CEO CryptoQuant Ки Ён Чжу отмечает, что ликвидность альткоинов падает. По его словам, проекты, которые развивают каналы притока капитала — например, через инфраструктуры уровня DAT или участие в продуктах, связанных с ETF, — повышают свои шансы на долгосрочное выживание. Проекты, которые этим не занимаются, сталкиваются с повышенными рисками.

Цикл биткоина не определен

Ожидания по альткоинам напрямую связаны с тем, на какой стадии находится биткоин. Типичный альтсезон начинается после того, как биткоин завершает пик цикла и переходит в более спокойную фазу.

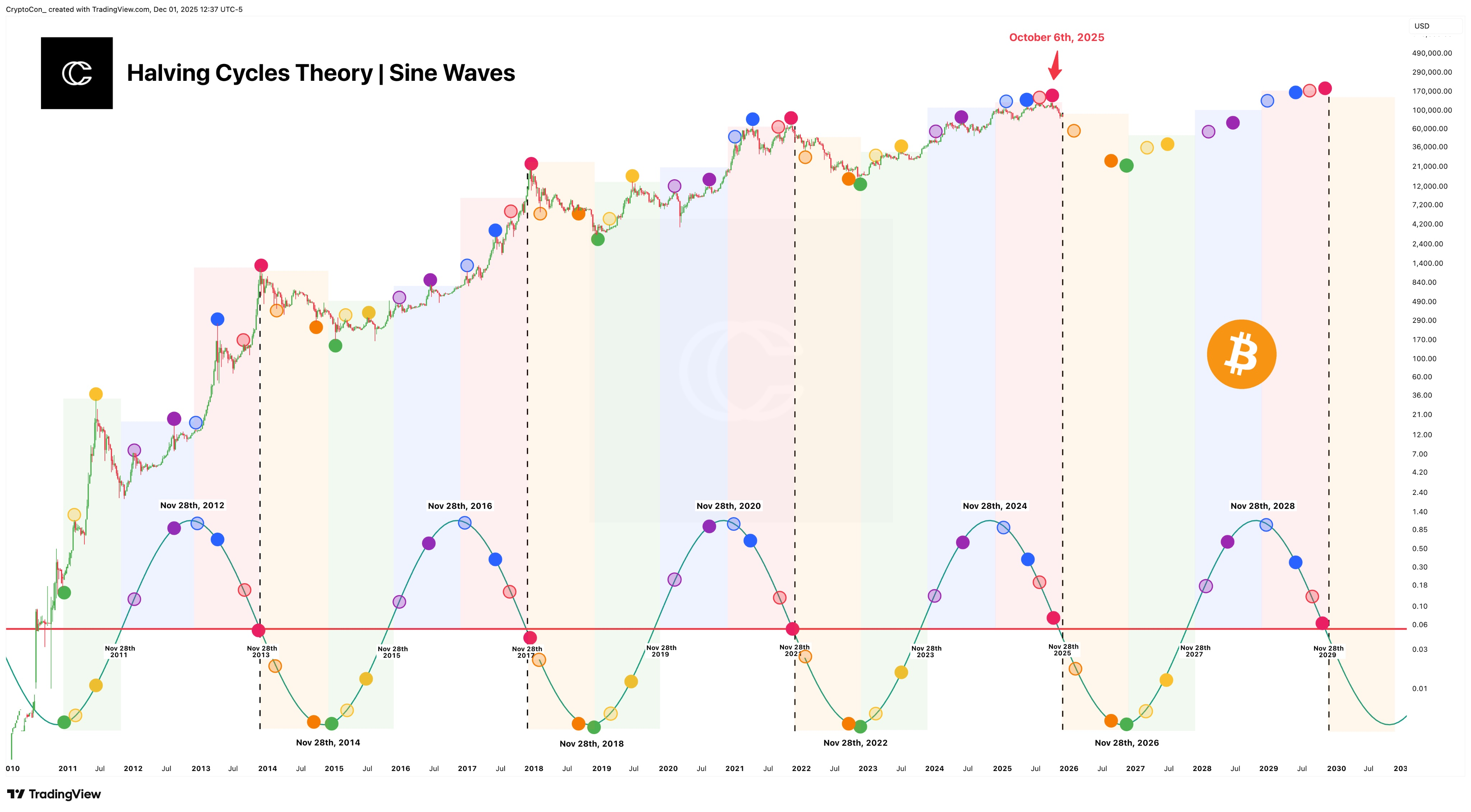

Аналитик CryptoCon придерживается четырехлетней модели. По его мнению, пик цикла пришелся на 6 октября 2025 года. Он считает, что год, соответствующий бычьей фазе, завершился 28 ноября 2025 года, а далее начинается период медвежьей динамики, который может продлиться до 28 ноября 2026 года. Он сообщил, что вышел из всех криптовалютных позиций.

Аналитическое подразделение Grayscale предлагает иную трактовку. По их наблюдениям, текущий цикл развивался без характерного розничного всплеска и формировался за счет институциональных потоков. Они допускают, что возможное снижение процентных ставок в 2026 году и прогресс в регулировании крипторынка могут привести к новым историческим максимумам биткоина именно в 2026 году, даже если это не совпадает с традиционной четырехлетней моделью.

К неопределенности добавляется и то, что траектория M2 окончательно разошлась с движением биткоина. Ранее многие ожидали, что биткоин будет следовать за M2. Сейчас M2 растет, а биткоин — нет. Это ставит под вопрос прежние подходы к анализу циклов.

Потенциал для будущего альтсезона

Несмотря на слабые текущие сигналы, предпосылки для будущего восстановления существуют. В 2026 году могут появиться факторы поддержки — снижение процентных ставок, улучшение финансовых условий и рост институционального интереса. Некоторые проекты уже укрепляют ликвидность и развивают инфраструктуру, подготавливаясь к возможному новому циклу.

В прошлых циклах альтсезон возникал при сочетании трех условий: роста экономики, достаточной ликвидности и улучшения ожиданий инвесторов. Сейчас эти условия отсутствуют, однако отдельные элементы могут начать формироваться в ближайшие кварталы.

Что в сухом остатке

Рынок находится в переходной фазе. Промышленность США не демонстрирует признаков устойчивого роста, ликвидность альткоинов снижается, аналитики расходятся во мнениях о текущем цикле биткоина, а прежние макрокорреляции перестали работать.

Альтсезон остается возможным сценарием, но условия для его появления пока не сформировались. Рынок продолжает ждать улучшения макроэкономических показателей и восстановления ликвидности. Без этого мощное движение в альткоинах маловероятно.