作者:Tuuxx

编译:Odaily 星球日报、Azuma

原标题:地狱行情下,如何使用DLMM实现1000%年化收益?

编者按:加密货币世界向来不缺高手,即便是在过去一个月的地狱行情期间,仍有人能够通过“非常规”的策略实现可观的收益。

11 月 19 日晚间,聚焦 DeFi 市场的海外 KOL Tuuxx 披露了自己近一个在 Meteora DLMM 上的做市策略及实操细节,Tuuxx 透露这期间自己盈利了 675 SOL,胜率 100%,对应年化收益率接近 1000%。

以下为 Tuuxx 全文内容,由 Odaily 星球日报编译。

近几周市场环境发生了巨大变化,因此我也相应调整了我的 Meteora DLMM 策略。

我只会在真实环境中测试过后才分享策略,以下是执行了近整整一个月时间(具体为 27 天)后的战绩成果:

-

100% 胜率;

-

盈利 675 枚 SOL;

-

期间回报率 19.35%;

-

若保持此节奏,理论年化收益率接近 1000%;

先叠个甲,这仍是我基于真实结果的个人分享 —— 不构成财务建议 —— 但希望能助你完善自己的策略。

底层资产选择

我的核心观点不变,我坚定看好 Solana 生态,目标是长期积累尽可能多的 SOL。因此我只向 SOL 交易对提供流动性,而非稳定币。

如果你需更多理由的话:

-

大多数代币都会与 SOL 组建交易对,而非稳定币,使用 SOL交易对能够自然增加手续费机会;

-

在市场急跌时,SOL 交易对通常比稳定币交易对风险更低 —— 若市场崩盘,各种代币与 SOL 可能同步下跌,从而降低完全跌破流动性区间的概率 —— 而与稳定币配对则可能让你暴露于更剧烈的不对称波动中;

-

以当前的收益率来看,即便在熊市期间,我的 DLMM 做市头寸的美元价值也会持续增长 —— 如果 SOL 重回历史高点,这种增值潜力将更加显著。

流动性曲线

我会选择相对较宽范围的买卖区间,而非窄区间或类似现货持仓式的布局。这样的方式能带来:

-

更强的资本保护;

-

更少的无常损失;

-

在波动中保持长期韧性;

这看起来可能不刺激,但我更喜欢稳定累积,而不是把流动性策略当成赌博。

做市代币选择

鉴于当前的市场环境,我的筛选标准已变得更为严苛,当前仅聚焦符合以下全部条件的代币:

能产生收入的协议(非炒作型的 Meme 代币);

-

强大活跃的社区;

-

市值高于5000万美元;

-

强劲的日交易量(超 500 万美元);

-

足够吸引人的“费用/TVL”比例;

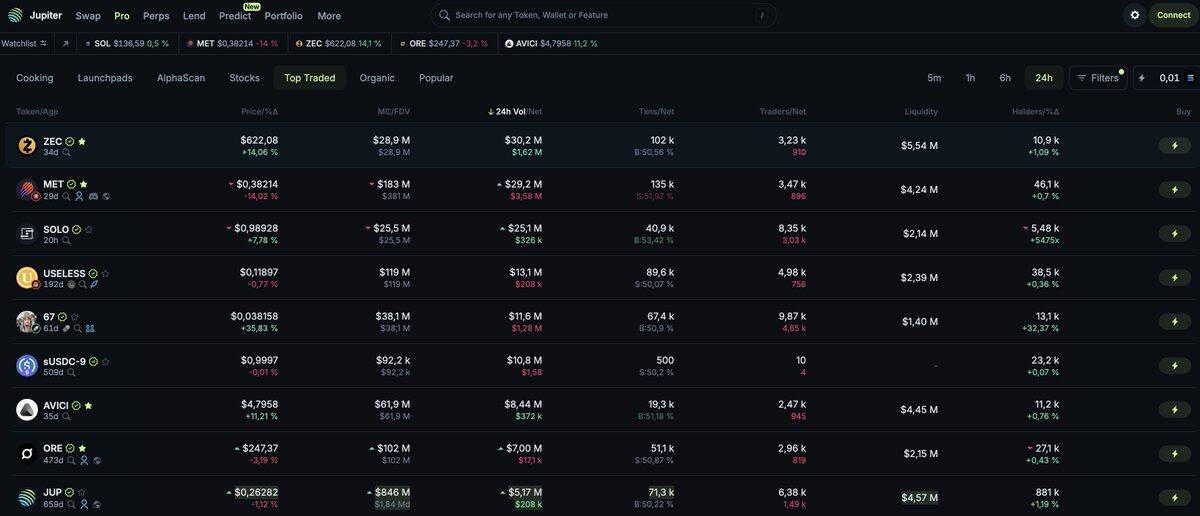

你可使用 Jupiter 与 Tokeo 追踪以上指标:https://jup.ag/pro?tab=toptraded

符合所有要求的代币极少,这反而有助于避免频繁调仓。过去数周我专注于以下四组交易对:MET/SOL、ZEC/SOL、ORE/SOL 与 AVICI/SOL。

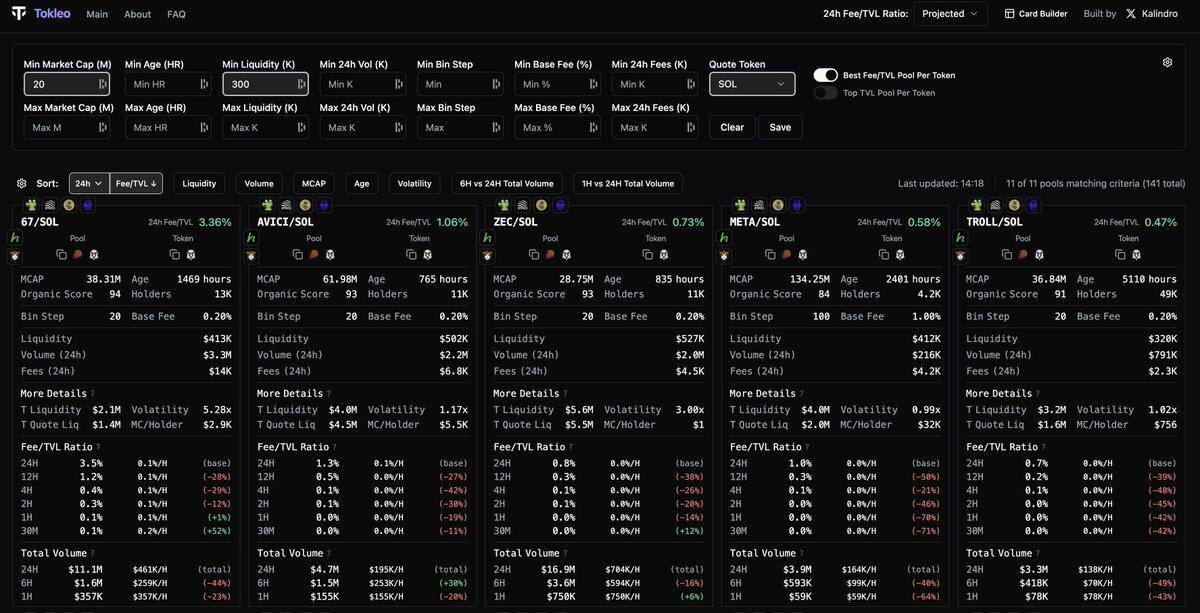

资金池选择

我会使用 Tokeo(https://tokleo.com/)来发掘表现最佳的资金池,通常会选择 Bin Step(用于定义每个价格区间的宽度)为 20,Base Fee(即基础手续费率)为 0.2% 的池子。

资金分配

我不会严格遵循某种公式,仅会按投资信念来分配资金比例 —— 且偏爱取整数。当前的分配状况如下:

-

MET/SOL:36%;

-

ZEC/SOL:24%;

-

ORE/SOL:24%;

-

AVICI/SOL:16%;

做市价格区间

我的目标是保护本金,我不是来追逐短期炒作的,耐心是本策略生效关键。

因此我会设定较宽的价格区间,且会通过 K 线走势的支撑区间来辅助判断,接受区间内最多70% 的下跌空间。

当前我在各交易对中使用的价格区间如下(以现价为准):

-

MET/SOL:下限约 –25%;

-

ZEC/SOL:下限约 –63%;

-

ORE/SOL:下限约 –69%;

-

AVICI/SOL:下限约 –70%;

宽区间或许需更长的时间才能产生可观收益,但却能提供稳定性保障,是承受重大市场冲击时唯一可靠的无压力方式。

仓位管理

这是变动最大的部分。

在做市代币与 SOL 之间发生明显价格波动后,我会:

-

提取所有流动性(SOL + 做市代币),但不会关闭做市仓位

-

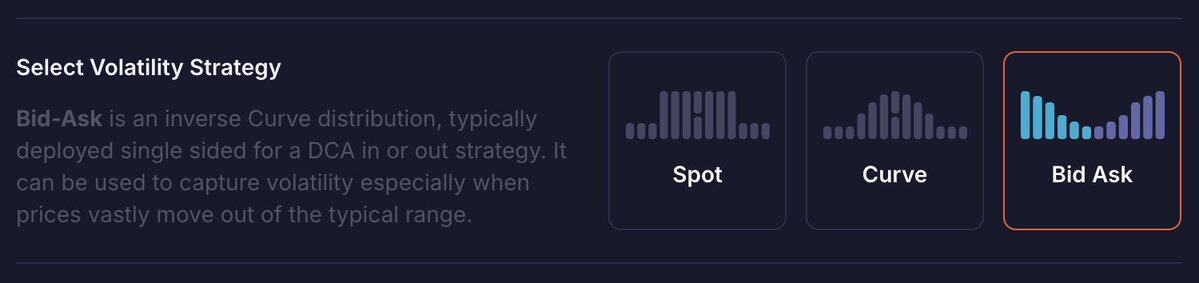

在相同区间重新部署:

-

100% 的 SOL 放回买卖(Bid-Ask)区间;

-

50% 的做市代币放回(Bid-Ask)买卖区间;

-

剩余 50% 代币放回现货(Spot)流动性曲线;

经过一段时间,你的仓位会出现类似这样的情况:

-

高位卖出、低位买入;

-

通过波动赚更多手续费;

-

逐步积累越来越多的 SOL;

这套复利机制是长期增值的关键,即便起始时采用宽区间也亦然。我通常会在收益达到 10–20% 左右时关闭一个做市头寸。

实践反馈

在实测该策略的 27 天中:

• 我从未因亏损平仓;

• 也从未看到跌传价格区间的情况发生;

我每日仅会查看资金池 2–3 次,仅在显著价格波动(涨或跌)后重新平衡 —— 不会过度交易,没什么压力。

无论你是操作 10 枚 SOL 还是 10000 枚SOL,持续性与复利效应远比起始规模重要。

再次声明,这并非财务建议,只是分享一个契合我增值目标与风险偏好的方法。

关于策略复制及地址追踪

目前此策略无法实现自动化及复制 —— 我得提前告诉你,以免你浪费时间或资金。

甚至投资组合追踪工具也无法准确读取仓位变化情况。例如,LP Agent 会显示我某些天出现了亏损 —— 但那只是因为当前的工具无法识别此类再平衡操作。

策略指导

我很乐于在评论区(原帖:https://x.com/Tuuxxdotsol/status/1991158752452489477)直接回应反馈与解答问题。分享此类策略最有价值之处在于,与同在真实市场中测试、优化与学习的同行交流。

此外,因近期多位成员咨询如何以定制化方式部署大型 DLMM 组合——我将通过 LP Army(@met_lparmy:https://www.lparmy.com/coaching)提供一对一指导。

此服务面向那些希望以专业的方式构建策略的人士 —— 并非提供信号或捷径,而是基于真实执行的清晰框架。

希望你的收益愈发稳健,晚安。

Twitter:https://twitter.com/BitpushNewsCN

比推 TG 交流群:https://t.me/BitPushCommunity

比推 TG 订阅: https://t.me/bitpush